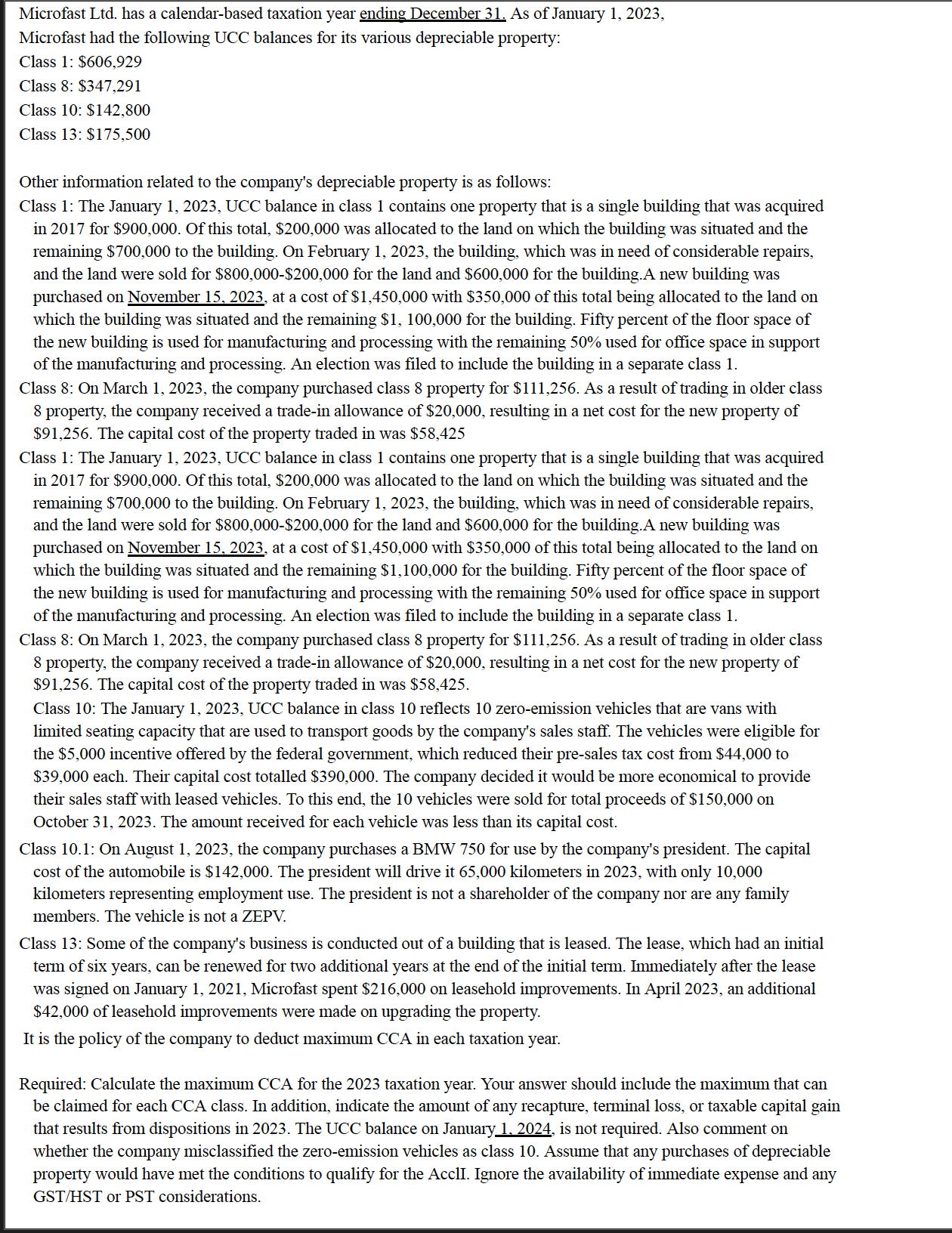

Microfast Ltd. has a calendar-based taxation year ending December 31. As of January 1, 2023, Microfast...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

To calculate the maximum Capital Cost Allowance CCA for the 2023 taxation year and determine any recapture terminal loss or taxable capital gain resul... View the full answer

Related Book For

College Algebra With Modeling And Visualization

ISBN: 9780134418049

6th Edition

Authors: Gary Rockswold

Posted Date: