Mr. Kofi Tieku who has been operating a trading business, DANCLAY MERCHANTS, for several years in...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

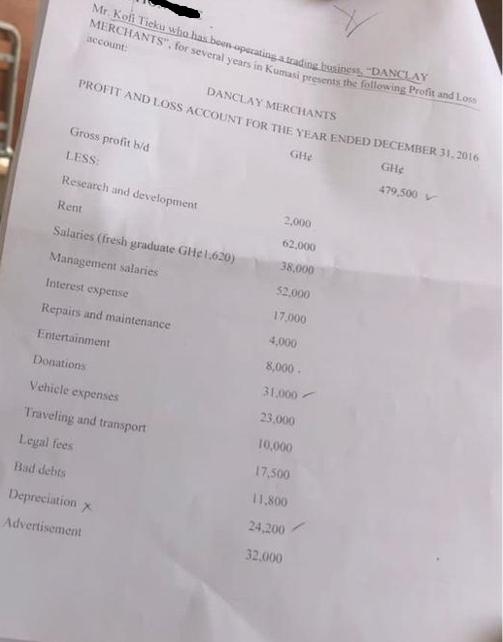

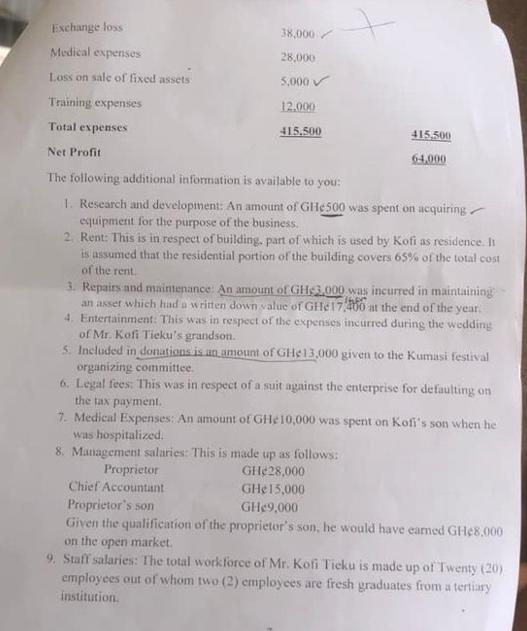

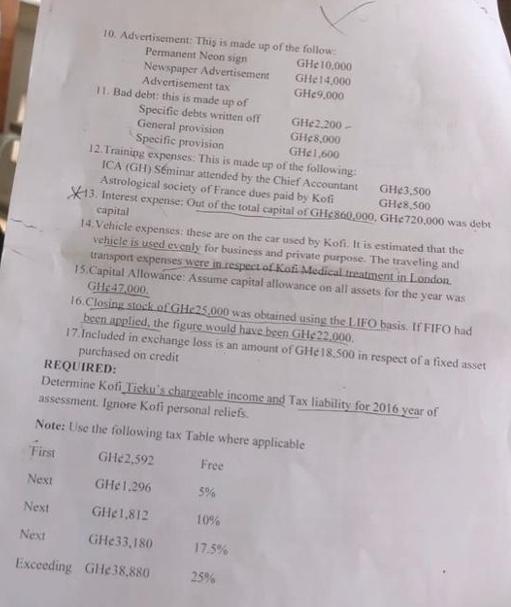

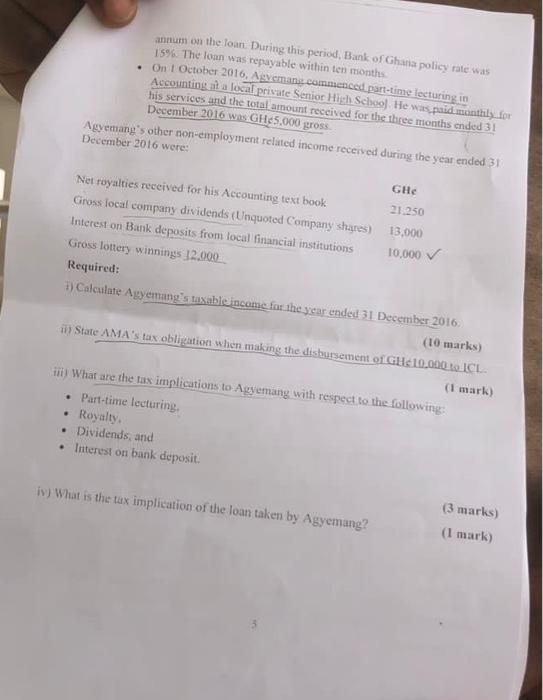

Mr. Kofi Tieku who has been operating a trading business, "DANCLAY MERCHANTS", for several years in Kumasi presents the following Profit and Loss account: DANCLAY MERCHANTS PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED DECEMBER 31, 2016 GH¢ 479,500 Gross profit b/d LESS: Research and development Rent Salaries (fresh graduate GH¢1,620) Management salaries Legal fees Bad debts Interest expense Repairs and maintenance Entertainment Donations Vehicle expenses Traveling and transport Depreciation x Advertisement GHe 2,000 62,000 38,000 $2,000 17,000 4,000 8,000. 31,000 23,000 10,000 17,500 11,800 24,200 32,000 Exchange loss Medical expenses Loss on sale of fixed assets 38,000 28,000 5,000 ✓ 12.000 415.500 Training expenses Total expenses Net Profit The following additional information is available to you: 1. Research and development: An amount of GHe 500 was spent on acquiring equipment for the purpose of the business. 2. Rent: This is in respect of building, part of which is used by Kofi as residence. It is assumed that the residential portion of the building covers 65% of the total cost of the rent 3. Repairs and maintenance: An amount of GHg3,000 was incurred in maintaining an asset which had a written down value of GHe 17.00 at the end of the year. 4. Entertainment: This was in respect of the expenses incurred during the wedding of Mr. Kofi Tieku's grandson. 5. Included in donations is an amount of GHe 13,000 given to the Kumasi festival organizing committee. 6. Legal fees: This was in respect of a suit against the enterprise for defaulting on the tax payment. 7. Medical Expenses: An amount of GHe 10,000 was spent on Kofi's son when he was hospitalized. 8. Management salaries: This is made up as follows: GH 28,000 Proprietor Chief Accountant 415.500 64,000 GH$15,000 GH¢9,000 Proprietor's son Given the qualification of the proprietor's son, he would have earned GHe8,000 on the open market. 9. Staff salaries: The total workforce of Mr. Kofi Ticku is made up of Twenty (20) employees out of whom two (2) employees are fresh graduates from a tertiary institution. 10. Advertisement: This is made up of the follow: GHe10,000 Permanent Neon sign Newspaper Advertisement GH:14,000 Advertisement tax GH¢9,000 11. Bad debt: this is made up of Specific debts written off General provision Specific provision Next Next Next GH₂2.200- GH¢8,000 GH¢1,600 12. Training expenses. This is made up of the following: ICA (GH) Seminar attended by the Chief Accountant Astrological society of France dues paid by Kofi GH¢3,500 GH¢8,500 13. Interest expense: Out of the total capital of GHc860,000, GHe720,000 was debt capital 14. Vehicle expenses: these are on the car used by Kofi. It is estimated that the vehicle is used evenly for business and private purpose. The traveling and transport expenses were in respect of Kofi Medical treatment in London. 15.Capital Allowance: Assume capital allowance on all assets for the year was GH:47,000. 16.Closing stock of GHe25,000 was obtained using the LIFO basis. If FIFO had been applied, the figure would have been GH₂22.000. 17. Included in exchange loss is an amount of GHe 18.500 in respect of a fixed asset purchased on credit REQUIRED: Determine Kofi Ticku's chargeable income and Tax liability for 2016 year of assessment. Ignore Kofi personal reliefs. Note: Use the following tax Table where applicable First GH22,592 Free GH₂1.296 5% GH1,812 10% GHe33,180 17.5% Exceeding GHe 38,880 25% annum on the loan. During this period, Bank of Ghana policy rate was 15%. The loan was repayable within ten months. . On 1 October 2016, Agyemang commenced part-time lecturing in Accounting at a local private Senior High School. He was paid monthly for his services and the total amount received for the three months ended 31 December 2016 was GHe5,000 gross. Agyemang's other non-employment related income received during the year ended 31 December 2016 were: Net royalties received for his Accounting text book Gross local company dividends (Unquoted Company shares) Interest on Bank deposits from local financial institutions Gross lottery winnings 12,000 . Required: i) Calculate Agyemang's taxable income for the year ended 31 December 2016. GH¢ 21.250 13,000 10,000 ✓ (10 marks) in State AMA's tax obligation when making the disbursement of GHe 10,000 to ICL (1 mark) iii) What are the tax implications to Agyemang with respect to the following: • Part-time lecturing. Royalty, • Dividends, and • Interest on bank deposit. iv) What is the tax implication of the loan taken by Agyemang? (3 marks) (1 mark) Mr. Kofi Tieku who has been operating a trading business, "DANCLAY MERCHANTS", for several years in Kumasi presents the following Profit and Loss account: DANCLAY MERCHANTS PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED DECEMBER 31, 2016 GH¢ 479,500 Gross profit b/d LESS: Research and development Rent Salaries (fresh graduate GH¢1,620) Management salaries Legal fees Bad debts Interest expense Repairs and maintenance Entertainment Donations Vehicle expenses Traveling and transport Depreciation x Advertisement GHe 2,000 62,000 38,000 $2,000 17,000 4,000 8,000. 31,000 23,000 10,000 17,500 11,800 24,200 32,000 Exchange loss Medical expenses Loss on sale of fixed assets 38,000 28,000 5,000 ✓ 12.000 415.500 Training expenses Total expenses Net Profit The following additional information is available to you: 1. Research and development: An amount of GHe 500 was spent on acquiring equipment for the purpose of the business. 2. Rent: This is in respect of building, part of which is used by Kofi as residence. It is assumed that the residential portion of the building covers 65% of the total cost of the rent 3. Repairs and maintenance: An amount of GHg3,000 was incurred in maintaining an asset which had a written down value of GHe 17.00 at the end of the year. 4. Entertainment: This was in respect of the expenses incurred during the wedding of Mr. Kofi Tieku's grandson. 5. Included in donations is an amount of GHe 13,000 given to the Kumasi festival organizing committee. 6. Legal fees: This was in respect of a suit against the enterprise for defaulting on the tax payment. 7. Medical Expenses: An amount of GHe 10,000 was spent on Kofi's son when he was hospitalized. 8. Management salaries: This is made up as follows: GH 28,000 Proprietor Chief Accountant 415.500 64,000 GH$15,000 GH¢9,000 Proprietor's son Given the qualification of the proprietor's son, he would have earned GHe8,000 on the open market. 9. Staff salaries: The total workforce of Mr. Kofi Ticku is made up of Twenty (20) employees out of whom two (2) employees are fresh graduates from a tertiary institution. 10. Advertisement: This is made up of the follow: GHe10,000 Permanent Neon sign Newspaper Advertisement GH:14,000 Advertisement tax GH¢9,000 11. Bad debt: this is made up of Specific debts written off General provision Specific provision Next Next Next GH₂2.200- GH¢8,000 GH¢1,600 12. Training expenses. This is made up of the following: ICA (GH) Seminar attended by the Chief Accountant Astrological society of France dues paid by Kofi GH¢3,500 GH¢8,500 13. Interest expense: Out of the total capital of GHc860,000, GHe720,000 was debt capital 14. Vehicle expenses: these are on the car used by Kofi. It is estimated that the vehicle is used evenly for business and private purpose. The traveling and transport expenses were in respect of Kofi Medical treatment in London. 15.Capital Allowance: Assume capital allowance on all assets for the year was GH:47,000. 16.Closing stock of GHe25,000 was obtained using the LIFO basis. If FIFO had been applied, the figure would have been GH₂22.000. 17. Included in exchange loss is an amount of GHe 18.500 in respect of a fixed asset purchased on credit REQUIRED: Determine Kofi Ticku's chargeable income and Tax liability for 2016 year of assessment. Ignore Kofi personal reliefs. Note: Use the following tax Table where applicable First GH22,592 Free GH₂1.296 5% GH1,812 10% GHe33,180 17.5% Exceeding GHe 38,880 25% annum on the loan. During this period, Bank of Ghana policy rate was 15%. The loan was repayable within ten months. . On 1 October 2016, Agyemang commenced part-time lecturing in Accounting at a local private Senior High School. He was paid monthly for his services and the total amount received for the three months ended 31 December 2016 was GHe5,000 gross. Agyemang's other non-employment related income received during the year ended 31 December 2016 were: Net royalties received for his Accounting text book Gross local company dividends (Unquoted Company shares) Interest on Bank deposits from local financial institutions Gross lottery winnings 12,000 . Required: i) Calculate Agyemang's taxable income for the year ended 31 December 2016. GH¢ 21.250 13,000 10,000 ✓ (10 marks) in State AMA's tax obligation when making the disbursement of GHe 10,000 to ICL (1 mark) iii) What are the tax implications to Agyemang with respect to the following: • Part-time lecturing. Royalty, • Dividends, and • Interest on bank deposit. iv) What is the tax implication of the loan taken by Agyemang? (3 marks) (1 mark)

Expert Answer:

Answer rating: 100% (QA)

Kofi Tiekus Chargeable Income and Tax Liability for 2016 Adjustments to Profit and Loss Account a Research and Development Deduct the capital expendit... View the full answer

Related Book For

Financial Accounting and Reporting

ISBN: 978-0273744443

14th Edition

Authors: Barry Elliott, Jamie Elliott

Posted Date:

Students also viewed these accounting questions

-

Bottle-Up, Inc. was organized on January 8, 2010. and made its Selection on January 24, 2010. The necessary consents to the election were filed in a timely manner. Its address is 1234 Hill Street,...

-

9. Find elecnic potential at P. (4) -49 -29 Given d= 1:5cm. P. 1+9 9=1.5MC. -49 +49 10. When an electron moves from A to B an electric along field Line, ao chown in the frg, the 394X10-19J t work....

-

The following additional information is available for the Dr. Ivan and Irene Incisor family from Chapters 1-5. Ivan's grandfather died and left a portfolio of municipal bonds. In 2012, they pay Ivan...

-

You have extracted a trial balance and drawn up accounts for the year ended 31 December 20X7. There was a shortage of 78 on the credit side of the trial balance, a suspense account being opened for...

-

Applepolscher has designed a Smith predictor with proportional control for a control loop that regulates blood glucose concentration with insulin flow. Based on simulation results for a FOPTD model,...

-

Write the "for-each" loop for the given "for" loop of 2 given arrays - int array 'marks and String array 'fruits' int marks] (100,80,70,60,50); for(int i=0; i

-

What internal accounting control principles are applicable to (a) executing and (b) recording securities transactions?

-

Installment SalesDefault and Repossession Seaver Company uses the installment-sales method in accounting for its installment sales. On January 1, 2010, Seaver Company had an installment account...

-

What struck you about the Growth Mindset video? How does it relate to yourself and what you've been thinking about your success in this course? Think about someone youknow who speaks well. What is it...

-

CableTech Bell Corporation (CTB) operates in the telecommunications industry. CTB has two divisions: the Phone Division and the Cable Service Division. The Phone Division manufactures telephones in...

-

find the reactions, as well as the shear force and bending moment diagrams. 8 5 KN force every 3 meters. om N WW 85 85 85 85 M W 85' 85% V =0-> Ay+By+cy = DookN {M = 0-> 53,550 = By+Cy 30m &5 851...

-

What is the primary purpose of admission-seeking questions?

-

What happens if you specify an invalid format string?

-

Why is it advisable to obtain a written confession from the subject of an investigation?

-

How many times can you define a function?

-

What is a compilation unit?

-

7. Prove the following using a two-column proof. Make sure to include reasons to support each of your statements. Mark congruent parts as you list them in your proof. (10pts) Given: ESGL E ZS = ZL...

-

Consider a game of poker being played with a standard 52-card deck (four suits, each of which has 13 different denominations of cards). At a certain point in the game, six cards have been exposed. Of...

-

The following is the draft trading and income statement of Parnell Ltd for the year ending 31 December 2003: You are given the following additional information, which is reflected in the above...

-

The following information is given in respect of Unambitious plc: (a) Non-current assets consist entirely of plant and machinery. The net book value of these assets as at 30 June 2010 is 100,000 in...

-

Discuss the following issues with regard to financial reporting for risk: (a) How can a company identify and priorities its key risks? (b) What actions can a company take to manage the risks...

-

LDDS continued to publicly report increasing profits and sales in the financial statements, which allowed it to acquire more companies with no limit to the growth of its stock price. True/False

-

WorldCom overstated its sales by holding its books open at the close of a reporting period. True/False

-

WorldCom overstated its earnings by improper accounting for multiple element contracts. True/False

Study smarter with the SolutionInn App