The Finance Manager of Anita Mills Limited, a medium-sized mill manufacturing coarse cloth was assessing the cash

Question:

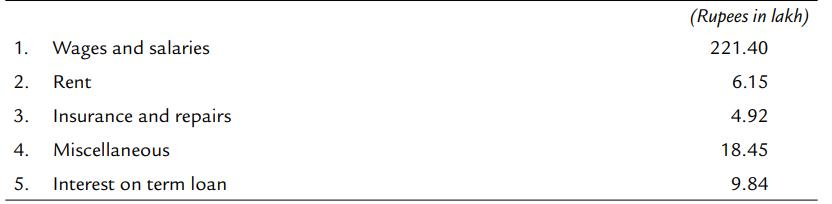

The Finance Manager of Anita Mills Limited, a medium-sized mill manufacturing coarse cloth was assessing the cash requirements for the operating year 2011 which had just started. The company had plans to increase its sales by 33 1/3 percent during 2011. In 2010 the company sold cloth valued at Rs. 708.48 lakh. The physical facilities present at the command of the company were considered adequate to sustain twice the 2010 level of production. In fact, in early January 2011 when this cash budgeting exercise was being done, revised production plans to suit the changed sales plan had just been finalized. Due to the seasonal demand of textile products, the sales during the quarters ending September and December were twice as much as those in the first two quarters of the year. Within each of these half years, however, there was near uniformity in the off-take. Efforts that Anita Mills's management were capable of could not alter the seasonal pattern of sales. The company, however, follows and would wish to continue to follow a constant level of production throughout the year because of several reasons. Sales are made on 30 days credit, and the company's experience in the collection were satisfactory. At the end of 2010 the clients owed Rs. 79.95 lakh of which Rs. 65.19 lahks pertained to December 2010 sales. The remaining sum of Rs. 14.76 lakh was being carried over from year to year, and there was no distinct possibility of its realization even during 2011-12. Major items of inputs required for the manufacture of cloth are cotton, dyes and chemicals, fuel and power, and labour. The Finance Manager knew that, for every rupee of sales, cost of cotton was 44 paise, dyes and chemicals 6 paise, fuel 4 paise and on the packaging, etc. 1 paisa. The company purchased cotton, dyes and chemicals and general maintenance stores on 60 days credit. Although it had not been strictly possible to pay the creditors in time in the past, the Finance Manager strongly wished to set things right at least during 2011. At the end of 2010, the company owed Rs. 132.84 lakh to its suppliers. The minimum stock of cotton the company would like to hold at any point of time is a fixed 1.5 months' requirements. Further, it is the company's policy to buy the requirements of cotton for any one month in the preceding month itself. At the end of 2010, cotton worth Rs. 55.35 lakh was held in inventory. Dyes and chemicals, available with insignificant lead time, were usually bought a month in advance of need. There was no stock of this item at end of 2010. The company maintains a stock of 3 months' requirement of stores and spares and replenishes consumption every month. They had, at the close of December 2010 , stores valued at Rs. 20.91 lakh of which a sum of Rs. 14.76 lakh represented obsolete stock. The company expects its annual consumption of stores and spares during 2011 to remain at the 2010 level of Rs. 49.20 lakh for the whole year. The mill had unsold finished goods worth Rs. 61.50 lakh (valued at market price) at the end of 2010 . The semi-processed material on the spindles and looms worth Rs. 6.15 lakh in 2010 is expected to remain the same during 2011. There was no clear defined policy with regard to stocking finished goods. The company would receive requisitions from buyers, well in advance, indicating the quantities they would like to lift in specified months. The company however made it a point to ensure that as far as possible the deliveries proposed in a particular month were ready by the end of the preceding one. The aggregate cash and bank balance was around Rs. 12.30 lakhs which, according to the Finance Manager, was the minimum he should hold at any time in 2011 also. Period based costs, as they were incurred in the year 2010, are given below: Expenses under 1,2 and 4 are paid every month. Insurance is paid half yearly in March and September; interest on term loan, which is expected to remain the same for 2011, is also paid half yearly but in the months of June and December.

The management expects a five percent increase in wages and salaries during 2011 on account of the revision in rates. The increased production plan for the year would increase the wage bill further by 5 percent. Other obligations which the company has to meet during 2011 are as follows:

The company estimates that its liability on the operational results for the year 2011 could be of the order of Rs. 49.20 lacks which, according to the tax laws, would have to be paid up in four equal quarterly installments, which commenced from June 2011.

1. Suggest the methodology for estimating the cash requirement of Anita Mills.

2. What assumptions have you made in estimating the requirement?

3. Provide the sketch of the partial balance sheet

4. In your opinion is the company profitable and are operations generating sufficient funds to finance requirements?

5. What is the nature of the working capital requirements of Anita Mills? Give your assumptions and their implications.

Expert Answer:

To estimate the cash requirements of Anita Mills for the operating year 2011 we can follow these steps 1 Forecast Sales Based on the 2010 sales value of Rs 70848 lakh and the expected increase of 33 1... View the full answer