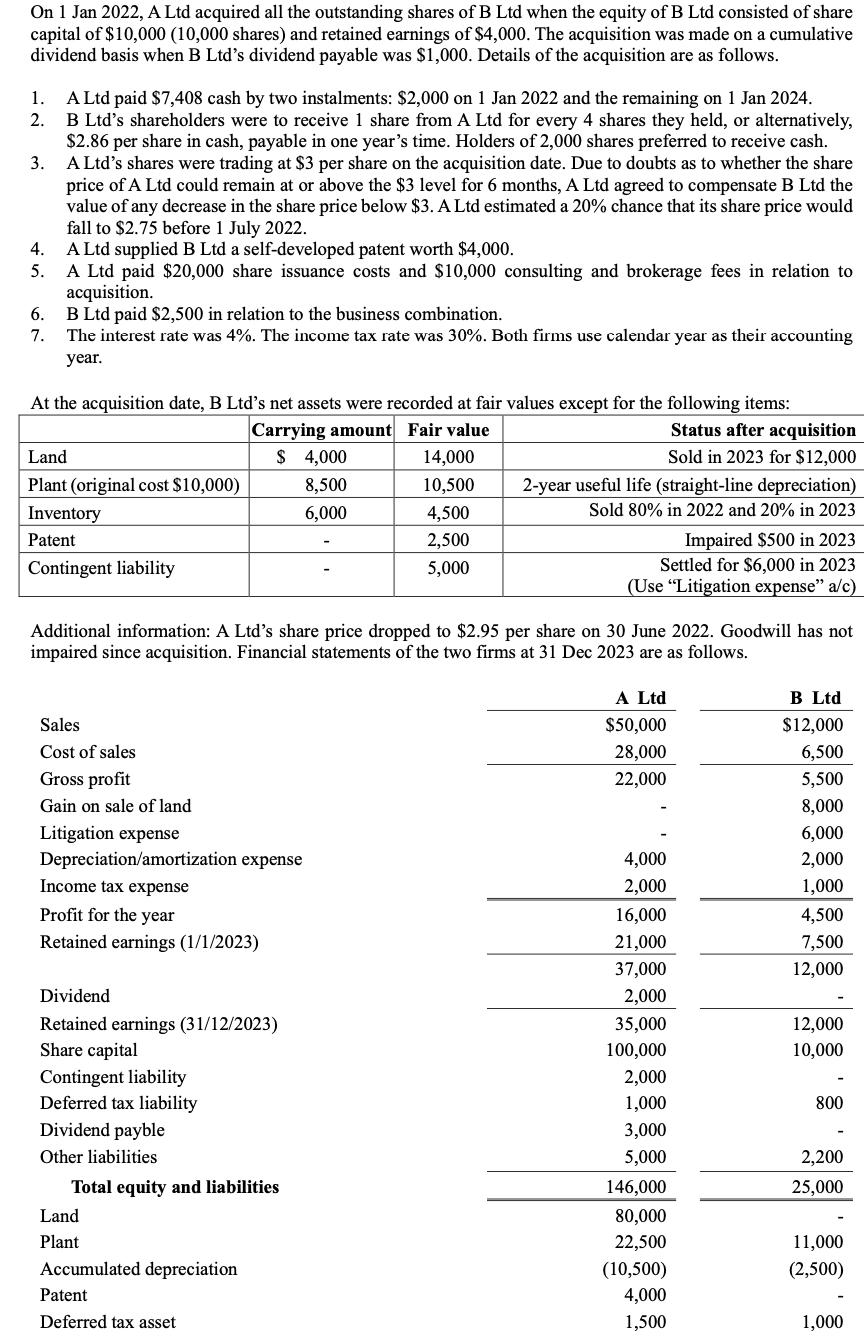

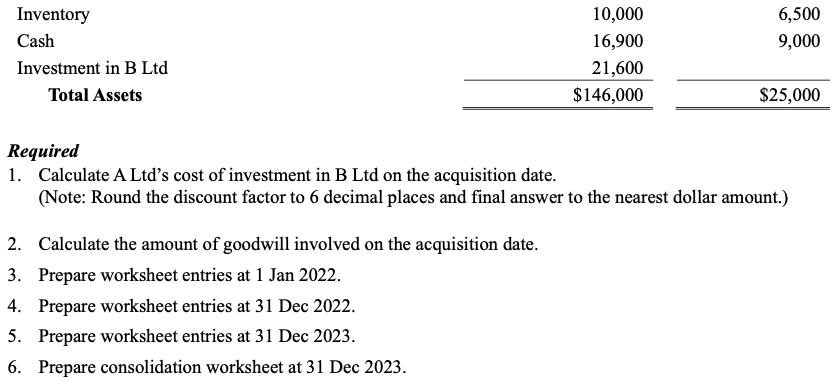

On 1 Jan 2022, A Ltd acquired all the outstanding shares of B Ltd when the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

1 Calculation of A Ltds cost of investment in B Ltd on the acquisition date Cost of shares issued to B Ltds shareholders Number of shares issued 10000 shares 4 2500 shares Cash payment per share 286 C... View the full answer

Related Book For

Posted Date: