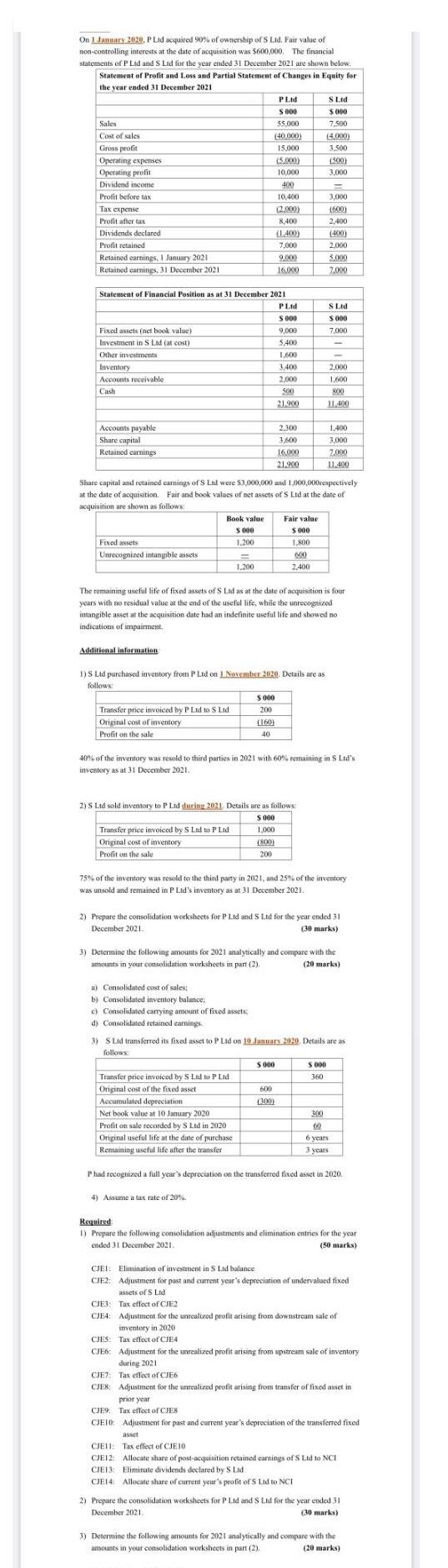

On 1 January 2020, P Ltd acquired 90% of ownership of S Ltd. Fair value of...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

On 1 January 2020, P Ltd acquired 90% of ownership of S Ltd. Fair value of non-controlling interests at the date of acquisition was $600,000. The financial statements of P Lid and S Ltd for the year ended 31 December 2021 are shown below. Statement of Profit and Loss and Partial Statement of Changes in Equity for the year ended 31 December 2021 Sales Cost of sales Gross profit Operating expenses Operating profit Dividend income Profit before tax Tax expense Profit after tas Dividends declared Profit retained Retained earnings, 1 January 2021 Retained earnings, 31 December 2021 Fixed assets (net book value) Investment in S Ltd (at cost). Other investments Inventory Accounts receivable. Cash Accounts payable Share capital Retained earnings Statement of Financial Position as at 31 December 2021 PLtd S000 9,000 5.400 1,600 Fixed assets Unrecognized intangible assets Additional information Book value S 000 1,200 Transfer price invoiced by P Ltd to S Lid Original cost of inventory Profit on the sale = 1,200 55,000 (40.000) 15,000 Transfer price invoiced by S Ltd to P Ltd Original cost of inventory Profit on the sale PLtd $ 000 (5.000) 10,000 400 10,400 (2.000) 8,400 (1.400) 7,000 9.000 16,000 $ 000 200 (160) 40 3,400 2,000 500 21.900 a) Consolidated cost of sales; b) Consolidated inventory balance: c) Consolidated carrying amount of fixed assets d) Consolidated retained earnings 1)S Ltd purchased inventory from P Ltd on 1 November 2620. Details are as follows: 4) Assume a tax rate of 20% 2.300 3,600 16,000 21.900 Share capital and retained earnings of S Lid were $3,000,000 and 1,000,000respectively at the date of acquisition. Fair and book values of net assets of S Ltd at the date of acquisition are shown as follows: 2)S Ltd sold inventory to P Lad during 2021. Details are as follows: $ 000 1,000 (800) 200 ||||||||▬▬▬▬▬ Fair value $ 000 1,800 600 2.400 600 (300) The remaining useful life of fixed assets of S Lad as at the date of acquisition is four years with no residual value at the end of the useful life, while the unrecognized intangible asset at the acquisition date had an indefinite useful life and showed no indications of impairment. $ 000 S Ltd $ 000 7,500 (4.000) 3.500 (500) 3.000 3,000 (600) 2,400 (400) 2,000 5.000 7,000 S Ltd $000 7,000 40% of the inventory was resold to third parties in 2021 with 60% remaining in S Ltd's inventory as at 31 December 2021. - 2,000 1,600 800 11,400 75% of the inventory was resold to the third party in 2021, and 25% of the inventory was unsold and remained in P Lid's inventory as at 31 December 2021. $ 000 360 1,400 3.000 7.000 11.400 2) Prepare the consolidation worksheets for P Ltd and S Ltd for the year ended 31 December 2021. (30 marks) 3) Determine the following amounts for 2021 analytically and compare with the amounts in your consolidation worksheets in part (2). (20 marks) 3) SLtd transferred its fixed asset to P Ltd on 10 January 2020. Details are as follows: Transfer price invoiced by S Ltd to P Lid Original cost of the fixed asset Accumulated depreciation Net book value at 10 January 2020 Profit on sale recorded by S Ltd in 2020 Original useful life at the date of purchase Remaining useful life after the transfer P had recognized a full year's depreciation on the transferred fixed asset in 2020. 300 60 6 years 3 years Required 1) Prepare the following consolidation adjustments and elimination entries for the year ended 31 December 2021. (50 marks) CJEI: Elimination of investment in S Ltd balance CJE2: Adjustment for past and current year's depreciation of undervalued fixed assets of S Ltd CJE3: Tax effect of CJE2 CJE4: Adjustment for the unrealized profit arising from downstream sale of inventory in 2020 CJES: Tax effect of CJE4 CJE6 Adjustment for the unrealized profit arising from upstream sale of inventory during 2021 CJE7: Tax effect of CJE6 CJES: Adjustment for the unrealized profit arising from transfer of fixed asset in prior year CJE9 Tax effect of CJES CJE10 Adjustment for past and current year's depreciation of the transferred fixed asset CJEII: Tax effect of CJE10 CJE12: Allocate share of post-acquisition retained earnings of S Ltd to NCI CJE13: Eliminate dividends declared by S Lid CJE14 Allocate share of current year's profit of S Ltd to NCI 2) Prepare the consolidation worksheets for P Ltd and S Ltd for the year ended 31 December 2021. (30 marks) 3) Determine the following amounts for 2021 analytically and compare with the amounts in your consolidation worksheets in part (2). (20 marks) a) Consolidated cost of sales b) Consolidated inventory balance c) Consolidated carrying amount of fixed assets Consolidated retained earnings On 1 January 2020, P Ltd acquired 90% of ownership of S Ltd. Fair value of non-controlling interests at the date of acquisition was $600,000. The financial statements of P Lid and S Ltd for the year ended 31 December 2021 are shown below. Statement of Profit and Loss and Partial Statement of Changes in Equity for the year ended 31 December 2021 Sales Cost of sales Gross profit Operating expenses Operating profit Dividend income Profit before tax Tax expense Profit after tas Dividends declared Profit retained Retained earnings, 1 January 2021 Retained earnings, 31 December 2021 Fixed assets (net book value) Investment in S Ltd (at cost). Other investments Inventory Accounts receivable. Cash Accounts payable Share capital Retained earnings Statement of Financial Position as at 31 December 2021 PLtd S000 9,000 5.400 1,600 Fixed assets Unrecognized intangible assets Additional information Book value S 000 1,200 Transfer price invoiced by P Ltd to S Lid Original cost of inventory Profit on the sale = 1,200 55,000 (40.000) 15,000 Transfer price invoiced by S Ltd to P Ltd Original cost of inventory Profit on the sale PLtd $ 000 (5.000) 10,000 400 10,400 (2.000) 8,400 (1.400) 7,000 9.000 16,000 $ 000 200 (160) 40 3,400 2,000 500 21.900 a) Consolidated cost of sales; b) Consolidated inventory balance: c) Consolidated carrying amount of fixed assets d) Consolidated retained earnings 1)S Ltd purchased inventory from P Ltd on 1 November 2620. Details are as follows: 4) Assume a tax rate of 20% 2.300 3,600 16,000 21.900 Share capital and retained earnings of S Lid were $3,000,000 and 1,000,000respectively at the date of acquisition. Fair and book values of net assets of S Ltd at the date of acquisition are shown as follows: 2)S Ltd sold inventory to P Lad during 2021. Details are as follows: $ 000 1,000 (800) 200 ||||||||▬▬▬▬▬ Fair value $ 000 1,800 600 2.400 600 (300) The remaining useful life of fixed assets of S Lad as at the date of acquisition is four years with no residual value at the end of the useful life, while the unrecognized intangible asset at the acquisition date had an indefinite useful life and showed no indications of impairment. $ 000 S Ltd $ 000 7,500 (4.000) 3.500 (500) 3.000 3,000 (600) 2,400 (400) 2,000 5.000 7,000 S Ltd $000 7,000 40% of the inventory was resold to third parties in 2021 with 60% remaining in S Ltd's inventory as at 31 December 2021. - 2,000 1,600 800 11,400 75% of the inventory was resold to the third party in 2021, and 25% of the inventory was unsold and remained in P Lid's inventory as at 31 December 2021. $ 000 360 1,400 3.000 7.000 11.400 2) Prepare the consolidation worksheets for P Ltd and S Ltd for the year ended 31 December 2021. (30 marks) 3) Determine the following amounts for 2021 analytically and compare with the amounts in your consolidation worksheets in part (2). (20 marks) 3) SLtd transferred its fixed asset to P Ltd on 10 January 2020. Details are as follows: Transfer price invoiced by S Ltd to P Lid Original cost of the fixed asset Accumulated depreciation Net book value at 10 January 2020 Profit on sale recorded by S Ltd in 2020 Original useful life at the date of purchase Remaining useful life after the transfer P had recognized a full year's depreciation on the transferred fixed asset in 2020. 300 60 6 years 3 years Required 1) Prepare the following consolidation adjustments and elimination entries for the year ended 31 December 2021. (50 marks) CJEI: Elimination of investment in S Ltd balance CJE2: Adjustment for past and current year's depreciation of undervalued fixed assets of S Ltd CJE3: Tax effect of CJE2 CJE4: Adjustment for the unrealized profit arising from downstream sale of inventory in 2020 CJES: Tax effect of CJE4 CJE6 Adjustment for the unrealized profit arising from upstream sale of inventory during 2021 CJE7: Tax effect of CJE6 CJES: Adjustment for the unrealized profit arising from transfer of fixed asset in prior year CJE9 Tax effect of CJES CJE10 Adjustment for past and current year's depreciation of the transferred fixed asset CJEII: Tax effect of CJE10 CJE12: Allocate share of post-acquisition retained earnings of S Ltd to NCI CJE13: Eliminate dividends declared by S Lid CJE14 Allocate share of current year's profit of S Ltd to NCI 2) Prepare the consolidation worksheets for P Ltd and S Ltd for the year ended 31 December 2021. (30 marks) 3) Determine the following amounts for 2021 analytically and compare with the amounts in your consolidation worksheets in part (2). (20 marks) a) Consolidated cost of sales b) Consolidated inventory balance c) Consolidated carrying amount of fixed assets Consolidated retained earnings

Expert Answer:

Answer rating: 100% (QA)

WNI Statement of Nell Assets of Leaf Share Capital Revaluation Reserve on NCA Reserve Surplus 810030... View the full answer

Related Book For

Advanced Accounting

ISBN: 978-1934319307

2nd edition

Authors: Susan S. Hamlen, Ronald J. Huefner, James A. Largay III

Posted Date:

Students also viewed these accounting questions

-

The financial statements for Lucky Ltd for the year ended 31 December 2014 were as follows. Additional information: Dividends paid during the year $60, 000 Retained earnings al 1 January 2014:...

-

After stocktaking for the year ended 31 May 20X2 had taken place, the closing inventory of Cobden Ltd was aggregated to a figure of 87,612. During the course of the audit that followed, the...

-

For the year ended 31 December 2019, Encik Remmy received annual salary of RM360,000. Besides, he received the following employment income and benefits from the company: Bonus equivalent to 1 month...

-

1 YOUR NAME: 2 Asset # 3 Asset name: 4 Date acquired: 5 Cost: 6 Depreciation method: 7 Salvage (residual) value: 8 Estimated useful life (years): 9 222 Computer 1/1/2018 $50,000 Straight Line (SL)...

-

Mumbai Company reported the following information for November and December 2010. Mumbais ending inventory at December 31 was destroyed in a fire. Instructions (a) Compute the gross profit rate for...

-

For the one-dimensional composite bar shown in Figure P13-1, determine the interface temperatures. For element 1, let Kxx = 200 W/(m ( oC); for element 2, let Kxx = 100 W/(m ( oC); and for element 3,...

-

For the goodness-of-fit test to be valid, each of the _______________ frequencies must be at least 5. In Exercises 9 and 10, fill in each blank with the appropriate word or phrase.

-

A water droplet falling in the atmosphere is spherical. Assume that as the droplet passes through a cloud, it acquires mass at a rate equal to kA where k is a constant (>0) and A its cross-sectional...

-

what is growth rate in real earnings A B 1 Index Numbers Problem 2 C D E F G 3 Nominal 2000 = 100 2005 = 100 4 Current $ Price 5 Year Earnings Index Price Index Real Constant $ Earnings 6 2003 7 2004...

-

Which series has the highest beta. BraveNewCoin Liquid Index for Bitcoin 1D BNC Trading Brave Ne Yellow Green Blue Orange

-

Question 3 Which C-X bond has the highest bond energy per mole? C-F C-Br OC-I OC-CI

-

_______ In the t test for a mean, the level of significance increases if the population standard deviation increases, holding the sample size constant.

-

_______ The t distribution is more dispersed than the normal.

-

_______ The mean of the t distribution is affected by the degrees of freedom.

-

_______ The t test can be applied with absolutely no assumptions about the distribution of the population.

-

You are cycling around a circular track at a constant speed. Does the magnitude of your acceleration change? The direction?

-

What are the various problems that could arise in Non-Return to Zero (NRZ) encoding if a continuous stream of 0s or 1s is sent?

-

Clark, PA, has been engaged to perform the audit of Kent Ltd.s financial statements for the current year. Clark is about to commence auditing Kents employee pension expense. Her preliminary enquiries...

-

On the consolidation working paper at the date of acquisition, elimination E credits the investment account by a. $ 2,400 b. $ 3,400 $ c. 5,000 d. $13,000 Use the following information to answer...

-

These descriptions of organizations relate to a city government. 1. The public school district is a legally separate entity responsible for the administration of city schools and has a separate board...

-

Present Value Analysis of Interest Rate Cap and Journal Entries At July I, 2013, Comiskey Company has $ 10,000,000 of debt due in four years with interest floating at prime. The rate is adjusted...

-

The wide-flange beam is subjected to the loading shown. Determine the stress components at points \(A\) and \(B\) and show the results on a volume element at each of these points. 2500 lb 3000 lb 500...

-

If the \(75-\mathrm{kg}\) man stands in the position shown, determine the state of stress at point \(A\) on the cross section of the plank at section \(a-a\). The center of gravity of the man is at...

-

The eccentric force \(\mathbf{P}\) is applied at a distance \(e_{y}\) from the centroid on the concrete support shown. Determine the range along the \(y\) axis where \(\mathbf{P}\) can be applied on...

Study smarter with the SolutionInn App