On April 1, 2019, Sigma Corporation purchased 5-year P10,000,000 10% bonds dated January 1, 2019. The bonds

Question:

On April 1, 2019, Sigma Corporation purchased 5-year P10,000,000 10% bonds dated January 1, 2019. The bonds were purchased to yield 12%. Interest is payable annually every December 31. The entity holds investment in bonds in order to collect contractual cash flows.

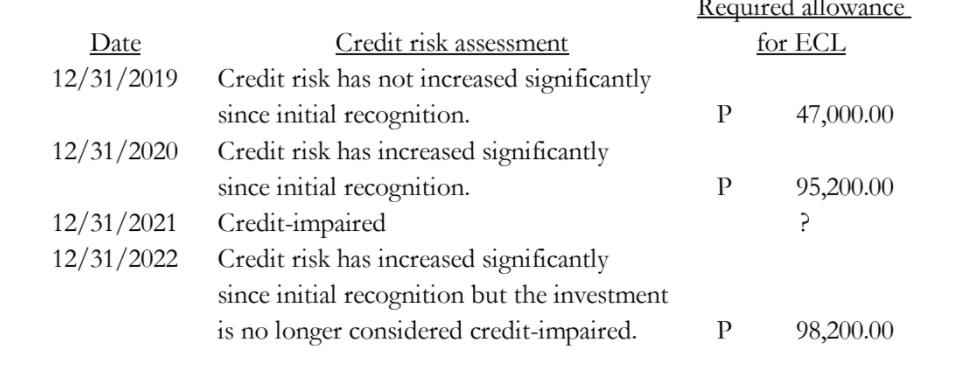

The entity monitors the change in credit quality of the investment since initial recognition and taking into account historical information, current conditions and forward- looking information, the entity computes the required expected credit losses (ECL) as follows:

On December 31, 2021, the issuer of the bonds is in financial difficulties and Sigma estimated that the issuer will not be able to pay interest for 2021 and 2022 and will be able to collect only P10,000,000 on December 31, 2023.

Answer the following: (Round off present value factors to four decimal places and final answers to nearest whole number)

1. How much was the total amount paid to acquire the investment in bonds on April 1, 2019?

2. How much is the amortized cost of the investment in bonds on December 31, 2019?

3. How much should be recognized as impairment loss in 2021?

4. How much should be recognized as interest income in 2022?

5. How much should be recognized as reversal on impairment loss in 2022?

Expert Answer:

1 The total amount paid to acquire the investment in bonds on April 1 2019 was P10000000 This is bec... View the full answer

Intermediate Accounting IFRS

ISBN: 978-1119372936

3rd edition

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield