On May 1, 2014, the company sold an additional 150 bonds with warrants attached. The bonds, which

Question:

On May 1, 2014, the company sold an additional 150 bonds with warrants attached. The bonds, which mature in 2029, had a face value of $1,000 each, with 6% annual coupon rate, interest due June 1 and December 1. (Each bond carries 10 warrants to buy one share of the common stock of the company at $15.00 per share one warrant .) The bonds were sold to a private investor at 103 (priced to yield 8%), plus accrued interest. By comparison to other similar securities, the company has determined that the day after the sale the fair value of the bonds without the warrants was 98, and that the warrants would be expected to trade at 14. On December 31, 2014, 750 warrants (with the appropriate amount of cash) were tendered to the company in exchange for common stock. The average price of the common stock during 2014 was $40 per share.

XYZ, Inc. began 2014 with 100,000 shares of $10 par common stock that were initially issued for $17.50 per share. These shares have been recorded.

Assumption: Effective interest method is used for discount amortization.

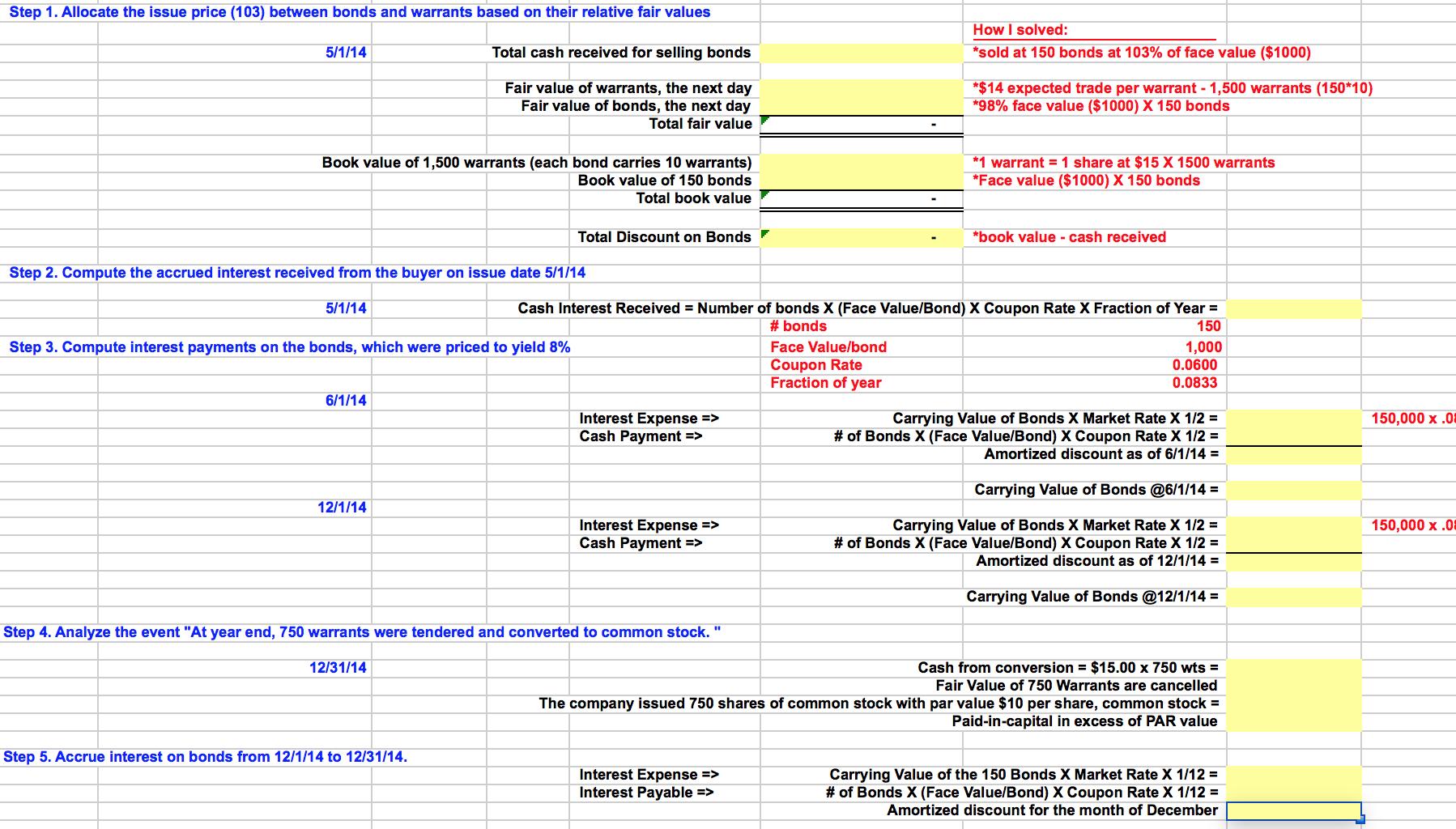

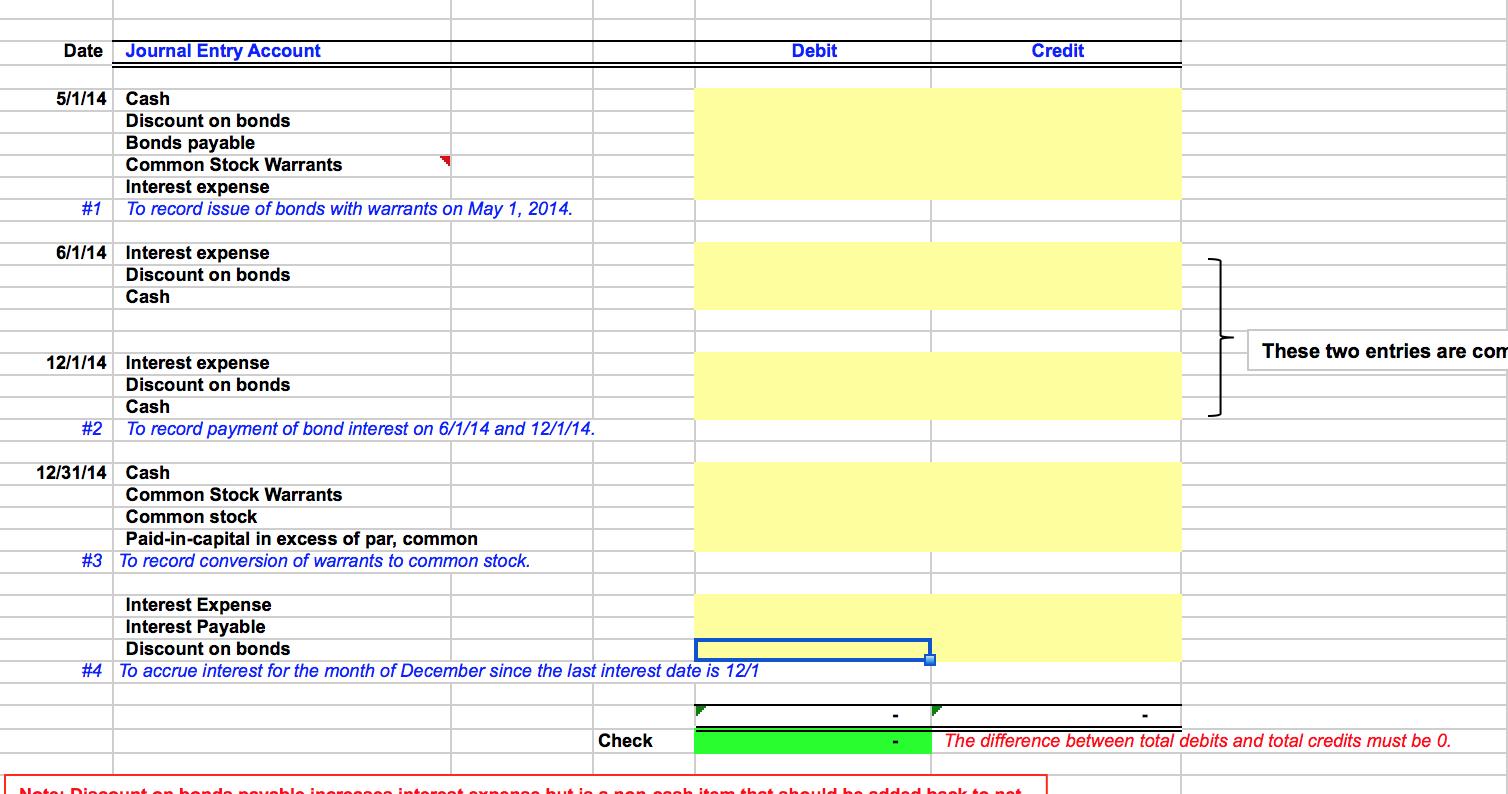

Step 1. Allocate the issue price (103) between bonds and warrants based on their relative fair values

Step 2. Compute the accrued interest received from the buyer on issue date 5/1/14

Step 3. Compute interest payments on the bonds, which were priced to yield 8%

Step 4. Analyze the event "At year end, 750 warrants were tendered and converted to common stock.

Step 5. Accrue interest on bonds from 12/1/14 to 12/31/14.

Expert Answer:

Answer and Explanation Step 1 Allocate the issue price 103 between bonds and warrants based on their ... View the full answer

Financial and managerial accounting

ISBN: 978-1118016114

1st edition

Authors: Jerry J. Weygandt, Paul D. Kimmel, Donald E. Kieso