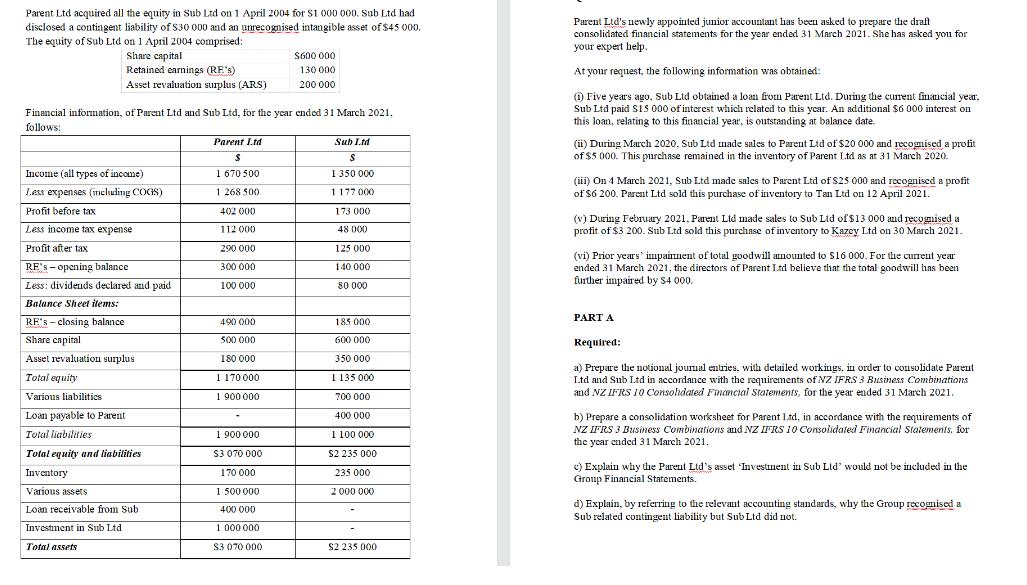

Parent Ltd acquired all the equity in Sub Ltd on 1 April 2004 for $1 000...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

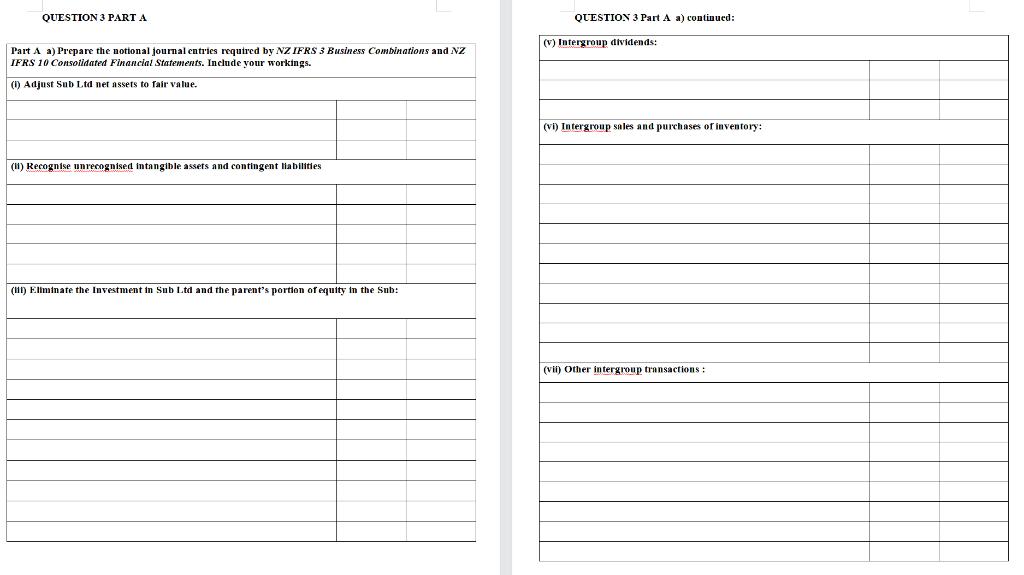

Parent Ltd acquired all the equity in Sub Ltd on 1 April 2004 for $1 000 000. Sub Ltd had disclosed a contingent liability of $30 000 and an unrecognised intangible asset of $45 000. The equity of Sub Ltd on 1 April 2004 comprised: Share capital Retained earnings (RE's) Asset revaluation surplus (ARS) Financial information, of Parent Ltd and Sub Ltd, for the year ended 31 March 2021. follows: Income (all types of income) Less expenses (including COGS) Profit before tax Less income tax expense Profit after tax RE's-opening balance Less: dividends declared and paid Balance Sheet items: RF's closing balance Share capital Asset revaluation surplus Total equity Various liabilities Loan payable to Parent Total liabilities Total equity and liabilities Inventory Various assets Loan receivable from Sub. Investment in Sub Ltd Total assets Parent Ltd $ 1 670 500 1 268 500 402 000 112 000 290 000 300 000 100 000 490 000 500 000 180 000 1 170 000 1900 000 1 900 000 $3 070 000 170 000 1 500 000 400 000 1 000 000 $600 000 130 000 200 000 $3 070 000 Sub Ltd $ 1 350 000 1177 000 173 000 48 000 125 000 140 000 80 000 185 000 600 000 350 000 1 135 000 700 000 400 000 1 100 000 $2 235 000 235 000 2 000 000 $2 235 000 Parent Ltd's newly appointed junior accountant has been asked to prepare the draft consolidated financial statements for the year ended 31 March 2021. She has asked you for your expert help. At your request, the following information was obtained: (1) Five years ago, Sub Ltd obtained a loan from Parent Ltd. During the current financial year. Sub Ltd paid $15 000 of interest which related to this year. An additional $6 000 interest on this loan, relating to this financial year, is outstanding at balance date. (ii) During March 2020, Sub Ltd made sales to Parent Ltd of $20 000 and recognised a profit of $5 000. This purchase remained in the inventory of Parent Ltd as at 31 March 2020. (iii) On 4 March 2021, Sub Ltd made sales to Parent Ltd of $25 000 and recognised a profit of $6 200. Parent Ltd sold this purchase of inventory to Tan Ltd on 12 April 2021. (v) During February 2021, Parent Ltd made sales to Sub Lid of $13 000 and recognised a profit of $3 200. Sub Ltd sold this purchase of inventory to Kazey Ltd on 30 March 2021. (vi) Prior years impainment of total goodwill amounted to $16 000. For the current year ended 31 March 2021, the directors of Parent Ltd believe that the total goodwill has been further impaired by $4 000. PART A Required: a) Prepare the notional joumal entries, with detailed workings, in order to consolidate Parent Ltd and Sub Ltd in accordance with the requirements of NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements, for the year ended 31 March 2021. b) Prepare a consolidation worksheet for Parent Ltd, in accordance with the requirements of NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements, for the year ended 31 March 2021. c) Explain why the Parent Ltd's asset Investment in Sub Ltd' would not be included in the Group Financial Statements. d) Explain, by referring to the relevant accounting standards, why the Group recognised a Sub related contingent liability but Sub Ltd did not. QUESTION 3 PART A Part A a) Prepare the notional journal entries required by NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements. Include your workings. (1) Adjust Sub Ltd net assets fair value. (1) Recognise unrecognised intangible assets and contingent liabilities (111) Eliminate the Investment in Sub Ltd and the parent's portion of equity in the Sub: QUESTION 3 Part A a) continued: (v) Intergroup dividends: (vi) Intergroup sales and purchases of inventory: (vii) Other intergroup transactions: Parent Ltd acquired all the equity in Sub Ltd on 1 April 2004 for $1 000 000. Sub Ltd had disclosed a contingent liability of $30 000 and an unrecognised intangible asset of $45 000. The equity of Sub Ltd on 1 April 2004 comprised: Share capital Retained earnings (RE's) Asset revaluation surplus (ARS) Financial information, of Parent Ltd and Sub Ltd, for the year ended 31 March 2021. follows: Income (all types of income) Less expenses (including COGS) Profit before tax Less income tax expense Profit after tax RE's-opening balance Less: dividends declared and paid Balance Sheet items: RF's closing balance Share capital Asset revaluation surplus Total equity Various liabilities Loan payable to Parent Total liabilities Total equity and liabilities Inventory Various assets Loan receivable from Sub. Investment in Sub Ltd Total assets Parent Ltd $ 1 670 500 1 268 500 402 000 112 000 290 000 300 000 100 000 490 000 500 000 180 000 1 170 000 1900 000 1 900 000 $3 070 000 170 000 1 500 000 400 000 1 000 000 $600 000 130 000 200 000 $3 070 000 Sub Ltd $ 1 350 000 1177 000 173 000 48 000 125 000 140 000 80 000 185 000 600 000 350 000 1 135 000 700 000 400 000 1 100 000 $2 235 000 235 000 2 000 000 $2 235 000 Parent Ltd's newly appointed junior accountant has been asked to prepare the draft consolidated financial statements for the year ended 31 March 2021. She has asked you for your expert help. At your request, the following information was obtained: (1) Five years ago, Sub Ltd obtained a loan from Parent Ltd. During the current financial year. Sub Ltd paid $15 000 of interest which related to this year. An additional $6 000 interest on this loan, relating to this financial year, is outstanding at balance date. (ii) During March 2020, Sub Ltd made sales to Parent Ltd of $20 000 and recognised a profit of $5 000. This purchase remained in the inventory of Parent Ltd as at 31 March 2020. (iii) On 4 March 2021, Sub Ltd made sales to Parent Ltd of $25 000 and recognised a profit of $6 200. Parent Ltd sold this purchase of inventory to Tan Ltd on 12 April 2021. (v) During February 2021, Parent Ltd made sales to Sub Lid of $13 000 and recognised a profit of $3 200. Sub Ltd sold this purchase of inventory to Kazey Ltd on 30 March 2021. (vi) Prior years impainment of total goodwill amounted to $16 000. For the current year ended 31 March 2021, the directors of Parent Ltd believe that the total goodwill has been further impaired by $4 000. PART A Required: a) Prepare the notional joumal entries, with detailed workings, in order to consolidate Parent Ltd and Sub Ltd in accordance with the requirements of NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements, for the year ended 31 March 2021. b) Prepare a consolidation worksheet for Parent Ltd, in accordance with the requirements of NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements, for the year ended 31 March 2021. c) Explain why the Parent Ltd's asset Investment in Sub Ltd' would not be included in the Group Financial Statements. d) Explain, by referring to the relevant accounting standards, why the Group recognised a Sub related contingent liability but Sub Ltd did not. QUESTION 3 PART A Part A a) Prepare the notional journal entries required by NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements. Include your workings. (1) Adjust Sub Ltd net assets fair value. (1) Recognise unrecognised intangible assets and contingent liabilities (111) Eliminate the Investment in Sub Ltd and the parent's portion of equity in the Sub: QUESTION 3 Part A a) continued: (v) Intergroup dividends: (vi) Intergroup sales and purchases of inventory: (vii) Other intergroup transactions:

Expert Answer:

Answer rating: 100% (QA)

ANSWER Why Parents Ltds asset Investment in Sub Ltd not included in the group financial statements C... View the full answer

Related Book For

Financial Accounting and Reporting

ISBN: 978-0273744443

14th Edition

Authors: Barry Elliott, Jamie Elliott

Posted Date:

Students also viewed these business communication questions

-

On 1 January 20X7 Parent Ltd acquired all the ordinary shares in Daughter Ltd for £6,000 cash. The fair value of the net assets in Daughter Ltd was their book value. Required: Prepare the...

-

In August 2018 Delz Ltd acquired all the equity shares of Eba Ltd, a large cable communications provider in Kenya. Eba Ltd is audited by a different audit practice where your firm has no...

-

On 1 July 2023, Gordon Ltd acquired all the issued shares (cum div.) of Henry Ltd for $528000. At that date, the financial statements of Henry Ltd showed the following information. Share capital...

-

The difference between case law and common is which of the following? O Common law creates law and case law interprets existing law. There is no difference. Case law is criminal law and common law is...

-

A recent survey of 992 people asked: In which professional sportfootball, boxing, hockey, or martial artsis an athlete most likely to sustain an injury that will affect the athlete after he or she...

-

What is the importance of writing minutes of the meeting? 2. What will happen if a company does not write minutes of the meeting every meeting? 3. What is the most difficult part in writing the...

-

Consider the sample space \(S=\{y y, y n, n y, n n\}\) in Example 2.2. Suppose that the subset of outcomes for which at least one camera conforms is denoted as \(E_{1}\). Then, \[ E_{1}=\{y y, y n, n...

-

The following transactions of Harmony Music Company occurred during 2010 and 2011: 2010 Mar 3 Purchased a piano (inventory) for $70,000, signing a six-month, 4% note payable. May 31 Borrowed $75,000...

-

The list below is a list of how many doses of a pain medication patients take in a hospital. Construct the histogram starting at -.5 and a class width of 20. 16 44 7 25 66 16 19 18 28 0 24 38 6 17 55...

-

Al Hansen, the newly appointed vice president of finance of Berkshire Instruments, was eager to talk to his investment dealer about future financing for the firm. One of Al's first assignments was to...

-

Choose a company that will be your client organization. You are taking the role of a consultant specializing in MIS and your task is to provide recommendations for how your client organization can...

-

YouGotThis LLC enters into a lease agreement on July 1, 2025, for equipment. YouGotThis LLC is the lessee. The following data are relevant to the lease agreement: 1. 2. 3. 4. The term of the...

-

Give an examples of democratic leadership style based on behaviors in a clinical setting. Give an example of self starter followership style based on behaviors in a clinical what are strengths...

-

In Business leadership, what are the process of servant leadership; democratic leadership; and enlightened leadership?

-

How does your emotional intelligence help or hinder your role as a leader ?

-

Discuss three features that characterize an economic evaluation/analysis in health economics and explain with examples.

-

Internal controls policies related to cash receipts include all of the following except: Different individuals receive cash, record cash receipts in the journal, and hold the cash. Checks received...

-

For liquid water the isothermal compressibility is given by; where r and b are functions of temperature only. If 1 kg of water is compressed isothermally and reversibly from I to 500 bar at 60(C. how...

-

(a) On 1 January 20X7 Parent Ltd acquired all the ordinary shares in Daughter Ltd for £16,200 cash. The fair value of the net assets in Daughter Ltd was their book value. (b) The purchase...

-

Summer plc acquired 60% of the common shares of Winter Ltd on 30 September 20X1 and gained control. At the date of acquisition, the balance of retained earnings of Winter was 35,000. At 31 December...

-

(a) The following ratios have been extracted from an analysis of the consolidated accounts of three companies North, South and East: Required: Comment on the respective performance of each of the...

-

Name some characteristics that allow you to observe light diffraction.

-

Planar waves from a monochromatic light source are normally incident on a circular obstacle, which casts a shadow on a screen positioned behind the obstacle. What do the wave properties of light...

-

Which wavelength of electromagnetic radiation do you expect to be diffracted by a window screen? What is the frequency of this radiation?

Study smarter with the SolutionInn App