Paul Dirac Enterprises actively manages its cost of funds and finances its operations by issuing floating rate

Question:

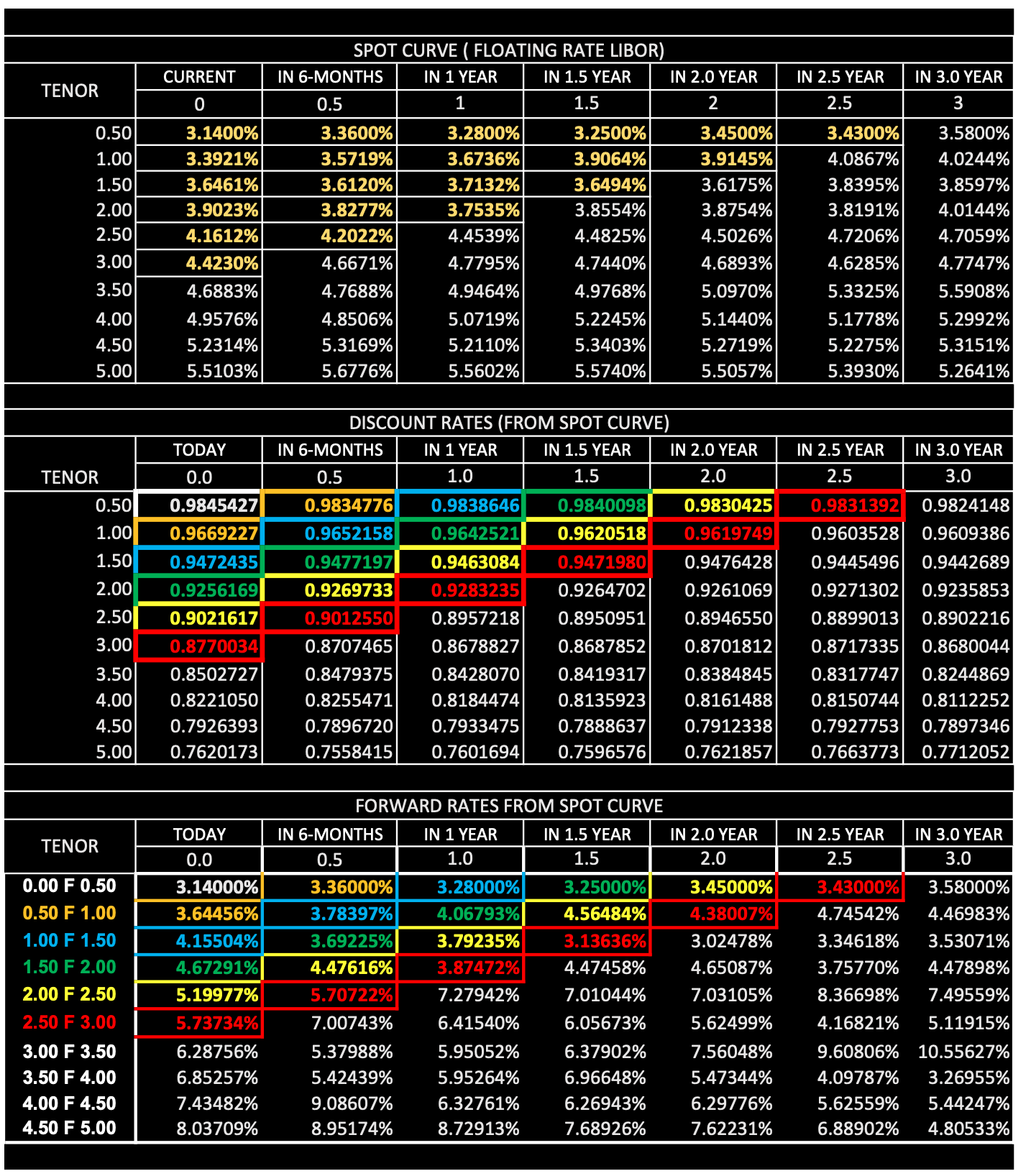

Paul Dirac Enterprises actively manages its cost of funds and finances its operations by issuing floating rate debt. The company recently issued a a 3-year floating rate bond based on LIBOR with 6-month resets (CURRENT floating rate LIBOR spot curve). The firms risk management team forecasts an increase in 6-mo LIBOR over the next 3-years. In order to protect themselves against increases in 6-Month LIBOR, the firm has decided to swap their 3 year floating rate bond to a 3 year fixed rate bond. The current 6-Month LIBOR spot curve and the future 6-Month LIBOR spot curves (over the next 3 years) are given in the table below. Furthermore, for every 6-Month LIBOR spot curve, the discount rates and 6-Month forward rates are also calculated.

1) Based on the Current 6-Month LIBOR Spot Rate Curve, calculate all SWAP RATES. 2) What is the SWAP RATE Dirac will use to convert his floating rate bond into a fixed rate bond? 3) Create the Payoff Table and the Profit Diagram for the SWAP 4) Value the Swap at every reset date (end of every 6-Month period). 5) Provide all journal entries and t-accounts necessary to account for the swap over the following 3 year period.

Expert Answer: