PHITBIT Limited is a sports wearable company, whose mission was to enhance passion of sports lovers, through

Question:

PHITBIT Limited is a sports wearable company, whose mission was to enhance passion of sports lovers, through innovative devices that collects and maps data to provide invaluable information.

The recent global pandemic crisis has opened up a window of opportunity in a new market segment; contact-tracing devices. Increasingly, governments are deploying tracking devices to better restraint the spread of the virus, as well as implement social distancing measures.

PHITBIT Limited has recently approached your firm, a management consultancy, to prepare a Request for Proposal (RFP) to tender for the government contract to manufacture an initial batch of wearable contact-tracing devices.

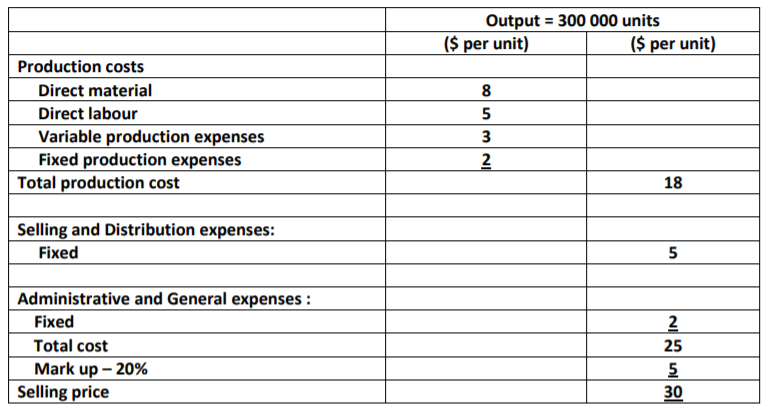

The costing details for a proposed output activity level is listed below:

The finance director of PHITBIT Limited needs your advice on their selling price policy. The sales price of $30 has been derived as above from a cost-plus mark-up pricing policy. The price was viewed as satisfactory, since the proposed output permits full capacity operation.

Your firm have been asked to analyze the effect on costs and profit of tendering at different selling prices. From marketing research conducted, you proposed three possible selling prices, with their respective annual demand:

You have collected the following information after analysing the effect that changes in production volume have on cost behaviour

? Direct material: cost per unit will increase by 20% for all units produced in the year if output decreases below 300 000 units per annum, due to loss of bulk discount.

? Direct labour: savings in bonus payments will reduce labour costs by $1 for all units produced in the year if activity decreases to 300 000 units and below per annum.

? Variable production expenses: due to savings arising from economies of scale, production expenses reduces to $1 per unit for output above 350 000 units per annum.

? Fixed production expenses: if annual production volume was below 300 000 units, then a machine rental cost of $50 000 per annum could be saved.

? Fixed selling expense: a reduction in the part time sales force would result in a $400 000 per annum savings if annual sales volume falls below 300 000 units.

? Administration and General expenses: to remain unaltered within the range of projected sales volume.

? Inventories: the company has no stock keeping policy.

Using MARGINAL ACCOUNTING approach,

(a) Prepare a schedule to show the expected annual profit to be earned for each of the three alternative selling price, and to make a recommendation to the finance director as to the selling price which should be set for the device.

(b) To better utilize limited resources, the Finance director has proposed deploying strategies directed at a relatively narrower class of potential customers.

Critically discuss how focused cost leadership and focused differentiation can enable PHITBIT Limited to achieve better financial performance, and the advantages and disadvantages of these strategies.

Expert Answer:

AnsA Following is the schedule showing cost structure and annual profit under the three scenarios given for varying levels of selling price and production Scenario I Scenario II Scenario III Selling P... View the full answer

Accounting for Decision Making and Control

ISBN: 978-0078025747

8th edition

Authors: Jerold Zimmerman