Pine LLC (Pine) is a company with its corporate office in Boston. One of its main...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

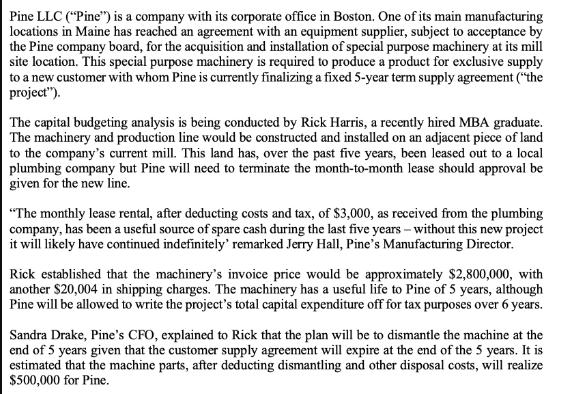

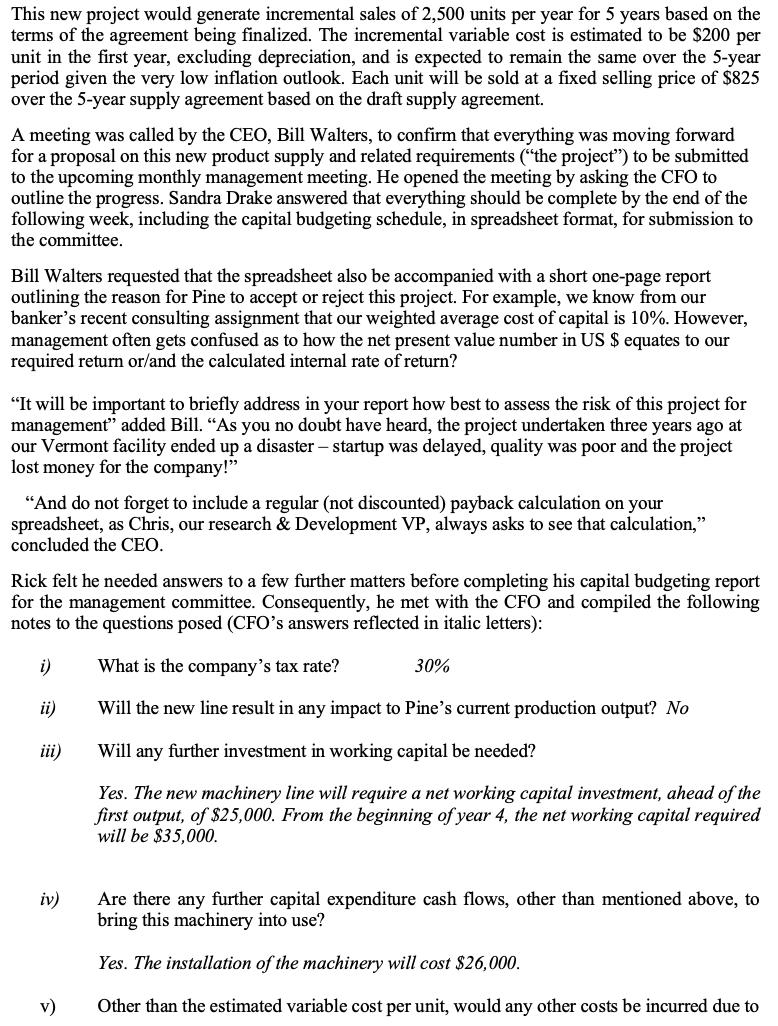

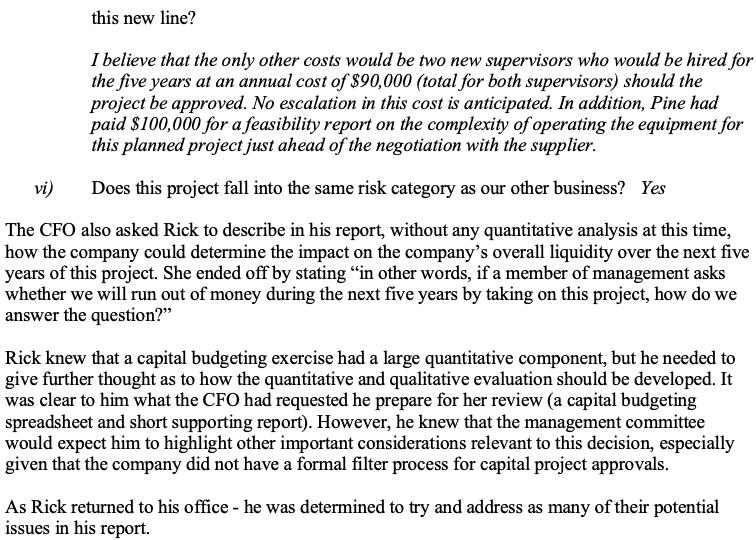

Pine LLC ("Pine") is a company with its corporate office in Boston. One of its main manufacturing locations in Maine has reached an agreement with an equipment supplier, subject to acceptance by the Pine company board, for the acquisition and installation of special purpose machinery at its mill site location. This special purpose machinery is required to produce a product for exclusive supply to a new customer with whom Pine is currently finalizing a fixed 5-year term supply agreement ("the project"). The capital budgeting analysis is being conducted by Rick Harris, a recently hired MBA graduate. The machinery and production line would be constructed and installed on an adjacent piece of land to the company's current mill. This land has, over the past five years, been leased out to a local plumbing company but Pine will need to terminate the month-to-month lease should approval be given for the new line. "The monthly lease rental, after deducting costs and tax, of $3,000, as received from the plumbing company, has been a useful source of spare cash during the last five years - without this new project it will likely have continued indefinitely' remarked Jerry Hall, Pine's Manufacturing Director. Rick established that the machinery's invoice price would be approximately $2,800,000, with another $20,004 in shipping charges. The machinery has a useful life to Pine of 5 years, although Pine will be allowed to write the project's total capital expenditure off for tax purposes over 6 years. Sandra Drake, Pine's CFO, explained to Rick that the plan will be to dismantle the machine at the end of 5 years given that the customer supply agreement will expire at the end of the 5 years. It is estimated that the machine parts, after deducting dismantling and other disposal costs, will realize $500,000 for Pine. This new project would generate incremental sales of 2,500 units per year for 5 years based on the terms of the agreement being finalized. The incremental variable cost is estimated to be $200 per unit in the first year, excluding depreciation, and is expected to remain the same over the 5-year period given the very low inflation outlook. Each unit will be sold at a fixed selling price of $825 over the 5-year supply agreement based on the draft supply agreement. A meeting was called by the CEO, Bill Walters, to confirm that everything was moving forward for a proposal on this new product supply and related requirements ("the project") to be submitted to the upcoming monthly management meeting. He opened the meeting by asking the CFO to outline the progress. Sandra Drake answered that everything should be complete by the end of the following week, including the capital budgeting schedule, in spreadsheet format, for submission to the committee. Bill Walters requested that the spreadsheet also be accompanied with a short one-page report outlining the reason for Pine to accept or reject this project. For example, we know from our banker's recent consulting assignment that our weighted average cost of capital is 10%. However, management often gets confused as to how the net present value number in US $ equates to our required return or/and the calculated internal rate of return? "It will be important to briefly address in your report how best to assess the risk of this project for management" added Bill. "As you no doubt have heard, the project undertaken three years ago at our Vermont facility ended up a disaster - startup was delayed, quality was poor and the project lost money for the company!" "And do not forget to include a regular (not discounted) payback calculation on your spreadsheet, as Chris, our research & Development VP, always asks to see that calculation," concluded the CEO. Rick felt he needed answers to a few further matters before completing his capital budgeting report for the management committee. Consequently, he met with the CFO and compiled the following notes to the questions posed (CFO's answers reflected in italic letters): What is the company's tax rate? 30% Will the new line result in any impact to Pine's current production output? No Will any further investment in working capital be needed? Yes. The new machinery line will require a net working capital investment, ahead of the first output, of $25,000. From the beginning of year 4, the net working capital required will be $35,000. i) ii) iii) iv) v) Are there any further capital expenditure cash flows, other than mentioned above, to bring this machinery into use? Yes. The installation of the machinery will cost $26,000. Other than the estimated variable cost per unit, would any other costs be incurred due to this new line? I believe that the only other costs would be two new supervisors who would be hired for the five years at an annual cost of $90,000 (total for both supervisors) should the project be approved. No escalation in this cost is anticipated. In addition, Pine had paid $100,000 for a feasibility report on the complexity of operating the equipment for this planned project just ahead of the negotiation with the supplier. vi) Does this project fall into the same risk category as our other business? Yes The CFO also asked Rick to describe in his report, without any quantitative analysis at this time, how the company could determine the impact on the company's overall liquidity over the next five years of this project. She ended off by stating "in other words, if a member of management asks whether we will run out of money during the next five years by taking on this project, how do we answer the question?" Rick knew that a capital budgeting exercise had a large quantitative component, but he needed to give further thought as to how the quantitative and qualitative evaluation should be developed. It was clear to him what the CFO had requested he prepare for her review (a capital budgeting spreadsheet and short supporting report). However, he knew that the management committee would expect him to highlight other important considerations relevant to this decision, especially given that the company did not have a formal filter process for capital project approvals. As Rick returned to his office - he was determined to try and address as many of their potential issues in his report. Pine LLC ("Pine") is a company with its corporate office in Boston. One of its main manufacturing locations in Maine has reached an agreement with an equipment supplier, subject to acceptance by the Pine company board, for the acquisition and installation of special purpose machinery at its mill site location. This special purpose machinery is required to produce a product for exclusive supply to a new customer with whom Pine is currently finalizing a fixed 5-year term supply agreement ("the project"). The capital budgeting analysis is being conducted by Rick Harris, a recently hired MBA graduate. The machinery and production line would be constructed and installed on an adjacent piece of land to the company's current mill. This land has, over the past five years, been leased out to a local plumbing company but Pine will need to terminate the month-to-month lease should approval be given for the new line. "The monthly lease rental, after deducting costs and tax, of $3,000, as received from the plumbing company, has been a useful source of spare cash during the last five years - without this new project it will likely have continued indefinitely' remarked Jerry Hall, Pine's Manufacturing Director. Rick established that the machinery's invoice price would be approximately $2,800,000, with another $20,004 in shipping charges. The machinery has a useful life to Pine of 5 years, although Pine will be allowed to write the project's total capital expenditure off for tax purposes over 6 years. Sandra Drake, Pine's CFO, explained to Rick that the plan will be to dismantle the machine at the end of 5 years given that the customer supply agreement will expire at the end of the 5 years. It is estimated that the machine parts, after deducting dismantling and other disposal costs, will realize $500,000 for Pine. This new project would generate incremental sales of 2,500 units per year for 5 years based on the terms of the agreement being finalized. The incremental variable cost is estimated to be $200 per unit in the first year, excluding depreciation, and is expected to remain the same over the 5-year period given the very low inflation outlook. Each unit will be sold at a fixed selling price of $825 over the 5-year supply agreement based on the draft supply agreement. A meeting was called by the CEO, Bill Walters, to confirm that everything was moving forward for a proposal on this new product supply and related requirements ("the project") to be submitted to the upcoming monthly management meeting. He opened the meeting by asking the CFO to outline the progress. Sandra Drake answered that everything should be complete by the end of the following week, including the capital budgeting schedule, in spreadsheet format, for submission to the committee. Bill Walters requested that the spreadsheet also be accompanied with a short one-page report outlining the reason for Pine to accept or reject this project. For example, we know from our banker's recent consulting assignment that our weighted average cost of capital is 10%. However, management often gets confused as to how the net present value number in US $ equates to our required return or/and the calculated internal rate of return? "It will be important to briefly address in your report how best to assess the risk of this project for management" added Bill. "As you no doubt have heard, the project undertaken three years ago at our Vermont facility ended up a disaster - startup was delayed, quality was poor and the project lost money for the company!" "And do not forget to include a regular (not discounted) payback calculation on your spreadsheet, as Chris, our research & Development VP, always asks to see that calculation," concluded the CEO. Rick felt he needed answers to a few further matters before completing his capital budgeting report for the management committee. Consequently, he met with the CFO and compiled the following notes to the questions posed (CFO's answers reflected in italic letters): What is the company's tax rate? 30% Will the new line result in any impact to Pine's current production output? No Will any further investment in working capital be needed? Yes. The new machinery line will require a net working capital investment, ahead of the first output, of $25,000. From the beginning of year 4, the net working capital required will be $35,000. i) ii) iii) iv) v) Are there any further capital expenditure cash flows, other than mentioned above, to bring this machinery into use? Yes. The installation of the machinery will cost $26,000. Other than the estimated variable cost per unit, would any other costs be incurred due to this new line? I believe that the only other costs would be two new supervisors who would be hired for the five years at an annual cost of $90,000 (total for both supervisors) should the project be approved. No escalation in this cost is anticipated. In addition, Pine had paid $100,000 for a feasibility report on the complexity of operating the equipment for this planned project just ahead of the negotiation with the supplier. vi) Does this project fall into the same risk category as our other business? Yes The CFO also asked Rick to describe in his report, without any quantitative analysis at this time, how the company could determine the impact on the company's overall liquidity over the next five years of this project. She ended off by stating "in other words, if a member of management asks whether we will run out of money during the next five years by taking on this project, how do we answer the question?" Rick knew that a capital budgeting exercise had a large quantitative component, but he needed to give further thought as to how the quantitative and qualitative evaluation should be developed. It was clear to him what the CFO had requested he prepare for her review (a capital budgeting spreadsheet and short supporting report). However, he knew that the management committee would expect him to highlight other important considerations relevant to this decision, especially given that the company did not have a formal filter process for capital project approvals. As Rick returned to his office - he was determined to try and address as many of their potential issues in his report.

Expert Answer:

Answer rating: 100% (QA)

Title Capital Budgeting for Pine LLC Evaluating the Viability of the New Project Introduction Pine LLC is considering a significant investment in special purpose machinery to meet the demands of a new ... View the full answer

Related Book For

Modern Advanced Accounting In Canada

ISBN: 9781259066481

7th Edition

Authors: Hilton Murray, Herauf Darrell

Posted Date:

Students also viewed these corporate finance questions

-

131.Darien and Hayden agree to accept Kevin into their partnership. Kevin will contribute $22,000 in cash. Prepare the journal entry to record this transaction. 132.Palmer withdraws from the FAP...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

Planning is one of the most important management functions in any business. A front office managers first step in planning should involve determine the departments goals. Planning also includes...

-

Why does Erasmus attack Church officials in his In Praise of Folly? O For spending money on lavish art O For not allowing clergy to marry O For supporting military campaigns O For selling pardons and...

-

Assume that the yield curves in the United States, France, and Japan are flat. If the U.S. yield curve suddenly becomes so positively sloped, do you think the yield curves in France and Japan would...

-

Consider the multifactor extension of the InuiKijima model. Let i F (t, T ), i = 1, 2, ,n, satisfy for some deterministic function k i (T ) and initial condition Define where Also, show that (i) it...

-

The following are independent situations for which ^you will recommend an appropriate auditor's report: 1. ^Subsequent to the date of the financial statements as part of the post-balance sheet date...

-

On May 31, the inventory balances of Princess Designs, a manufacturer of high-quality children's clothing, were as follows: Materials Inventory, $21,360; Work in Process Inventory, $15,112; and...

-

During the past 10 years, the percent returns on two mutual funds (aggressive and passive) expressed in percentages were as follows:. During the past 10 years, the percent returns on two mutual funds...

-

Table 1 shows Apple's online orders for the last week. When shoppers place an online order, several "recommended products" (upsells) are shown as at checkout an attempt to upsell See table 2 in cell...

-

Consider the following matrix and column vector : -8 1 2 2 0 5 A = 4 3 1 and v = 3 6 1 5 5. Verify that v E N(A) and then extend {v} to a basis of N(A). 133

-

Show how the imposition of a minimum wage on a monopsony can increase both wages and employment.

-

Why a system of pulleys is used for lifting load ?

-

Describe the trends in wages and employment implied by the cobweb model for the engineering market. What would happen to the cobwebs if a consulting firm sold information on the history of wages and...

-

What is the velocity ratio of the first system of pulleys ?

-

What is the velocity ratio of the second system of pulleys ?

-

Jan 12- Sold machinery to the Brigita's dance theatre in Mississauga Invoice #118 in cash for $4550 excluding tax. (do not attach a file until you have completed the test). Step by step how can do...

-

Distinguish between the work performed by public accountants and the work performed by accountants in commerce and industry and in not-for-profit organisations.

-

Able Company holds a 40% interest in Baker Corp. During the year, Able sold a portion of this investment. How should this investment be reported after the sale?

-

What is the purpose of IFRS 8 on Operating Segments?

-

Explain how the temporal method produces results that are consistent with the normal measurement and valuation of assets and liabilities for domestic transactions and operations.

-

Paymore Shoes acquired 80 percent of the voting stock of Spire Footwear on February 1, 2014, for \($21\) million. The fair value of the noncontrolling interest at the acquisition date was \($3\)...

-

Pacific Athletic Corporation owns all of the voting stock of Solovair Apparel. Acquisition cost was \($10\) million in excess of Solovairs book value of \($2\) million, and the excess was attributed...

-

Peninsula Industries and Seaport Company, a 90 percent owned subsidiary, engage in extensive intercompany transactions involving raw materials, component parts, and completed products. Peninsula...

Study smarter with the SolutionInn App