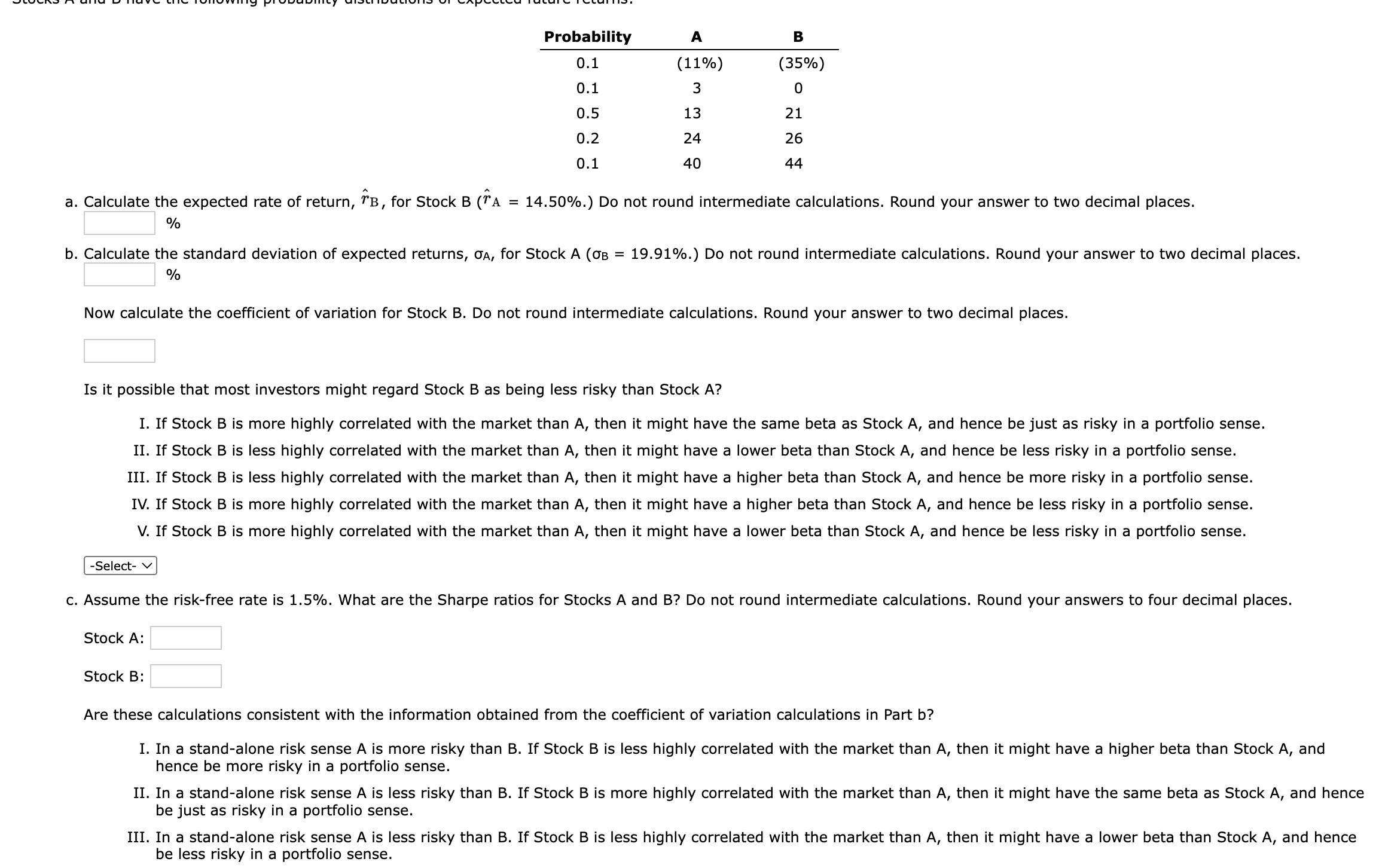

Probability A B 0.1 (11%) (35%) 0.1 3 0 0.5 0.2 0.1 NE 13 21 24...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Probability A B 0.1 (11%) (35%) 0.1 3 0 0.5 0.2 0.1 NE 13 21 24 40 26 44 a. Calculate the expected rate of return, ^B, for Stock B (A A = 14.50%.) Do not round intermediate calculations. Round your answer to two decimal places. % b. Calculate the standard deviation of expected returns, A, for Stock A (OB = % 19.91%.) Do not round intermediate calculations. Round your answer to two decimal places. Now calculate the coefficient of variation for Stock B. Do not round intermediate calculations. Round your answer to two decimal places. Is it possible that most investors might regard Stock B as being less risky than Stock A? I. If Stock B is more highly correlated with the market than A, then it might have the same beta as Stock A, and hence be just as risky in a portfolio sense. II. If Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. III. If Stock B is less highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be more risky in a portfolio sense. IV. If Stock B is more highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be less risky in a portfolio sense. V. If Stock B is more highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. -Select- c. Assume the risk-free rate is 1.5%. What are the Sharpe ratios for Stocks A and B? Do not round intermediate calculations. Round your answers to four decimal places. Stock A: Stock B: Are these calculations consistent with the information obtained from the coefficient of variation calculations in Part b? I. In a stand-alone risk sense A is more risky than B. If Stock B is less highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be more risky in a portfolio sense. II. In a stand-alone risk sense A is less risky than B. If Stock B is more highly correlated with the market than A, then it might have the same beta as Stock A, and hence be just as risky in a portfolio sense. III. In a stand-alone risk sense A is less risky than B. If Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. Probability A B 0.1 (11%) (35%) 0.1 3 0 0.5 0.2 0.1 NE 13 21 24 40 26 44 a. Calculate the expected rate of return, ^B, for Stock B (A A = 14.50%.) Do not round intermediate calculations. Round your answer to two decimal places. % b. Calculate the standard deviation of expected returns, A, for Stock A (OB = % 19.91%.) Do not round intermediate calculations. Round your answer to two decimal places. Now calculate the coefficient of variation for Stock B. Do not round intermediate calculations. Round your answer to two decimal places. Is it possible that most investors might regard Stock B as being less risky than Stock A? I. If Stock B is more highly correlated with the market than A, then it might have the same beta as Stock A, and hence be just as risky in a portfolio sense. II. If Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. III. If Stock B is less highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be more risky in a portfolio sense. IV. If Stock B is more highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be less risky in a portfolio sense. V. If Stock B is more highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. -Select- c. Assume the risk-free rate is 1.5%. What are the Sharpe ratios for Stocks A and B? Do not round intermediate calculations. Round your answers to four decimal places. Stock A: Stock B: Are these calculations consistent with the information obtained from the coefficient of variation calculations in Part b? I. In a stand-alone risk sense A is more risky than B. If Stock B is less highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be more risky in a portfolio sense. II. In a stand-alone risk sense A is less risky than B. If Stock B is more highly correlated with the market than A, then it might have the same beta as Stock A, and hence be just as risky in a portfolio sense. III. In a stand-alone risk sense A is less risky than B. If Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense.

Expert Answer:

Posted Date:

Students also viewed these finance questions

-

Inscribe a detailed paper on RFID Solutions and Standards in the Transportation Industry.

-

EAR versus APR Big Doms Pawn Shop charges an interest rate of 25 percent per month on loans to its customers like all lenders, Big Dom must report an APR to consumers. What rate should the shop...

-

How many stationary policies are there in the problem of Exercise 5?

-

Timing options make it less likely that a project will be accepted today. Often, if a firm can delay a decision, it can increase the expected NPV of a project.

-

(Multiple Choice) 1. What is the best source of income for a corporation? a. Prior-period adjustments b. Continuing operations c. Discontinued operations d. Extraordinary items 2. Leslies Lotion...

-

1) You rent a studio apartment and use a particular section of the apartment regularly and exclusively to run your drop shipping business.Thetotal square footage you use to run your business is 30...

-

A horizontal flow initially at Mach 1 flows over a downward-sloping expansion corner, thus creating a centered Prandtl-Meyer expansion wave. The streamlines that enter the head of the expansion wave...

-

Customer service costs at BA-929 Inc. are as follows: Number of Customers Customer Service Cost Served March 11,672 $28,348 April 11,468 $28,305 May 12,000 $28,417 June 14,500 $28,942 July 11,732...

-

What factors affect the size of a companys cash dividend?

-

a. List five steps in completing preliminary planning before specifying the substantive tests to be included in an audit program, b. List six steps in the general framework for specifying substantive...

-

What is the relationship between the acceptable level of detection risk and the extent of substantive tests?

-

How should the auditor's decisions regarding the design of substantive tests to be performed be documented in the working papers?

-

Explain the effect on the accounting equation of ordinary shares issued for cash.

-

i.Stock X has a beta of 1.79, Stock Y has a beta of 0.87, the expected rate of return on an average stock is 14.5%, and the risk-free rate is 9%. By how much does the required return on the riskier...

-

How do the principles of (a) Physical controls and (b) Documentation controls apply to cash disbursements?

-

Teague Corporation has the following long-term investments: 1. 60 percent of the common stock of Ariel Corporation 2. 13 percent of the common stock of Copper, Inc. 3. 50 percent of the nonvoting...

-

The stockholders equity section of Caritas Corporations balance sheet appeared as follows on December 31: Swanson Manufacturing Company owns 80 percent of Caritass voting stock and paid $11.20 per...

-

Edson Manufacturing Company purchased 100 percent of the common stock of Liverpool Manufacturing Company for $600,000. Liverpools stockholders equity included common stock of $400,000 and retained...

Study smarter with the SolutionInn App