Problem 1 (Weight 60%; each question weighted equally) After completing your degree in finance from NHH...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

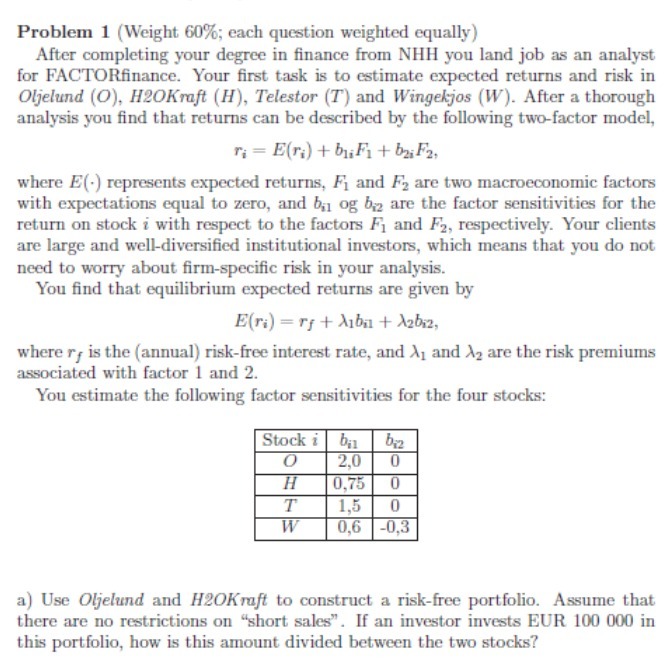

Problem 1 (Weight 60%; each question weighted equally) After completing your degree in finance from NHH you land job as an analyst for FACTORfinance. Your first task is to estimate expected returns and risk in Oljelund (O), H20Kraft (H), Telestor (T) and Wingekjos (W). After a thorough analysis you find that returns can be described by the following two-factor model, r=E(r)+bi Fi+bai F2, where E(-) represents expected returns, F and F are two macroeconomic factors with expectations equal to zero, and bi og b are the factor sensitivities for the return on stock i with respect to the factors F1 and F2, respectively. Your clients are large and well-diversified institutional investors, which means that you do not need to worry about firm-specific risk in your analysis. You find that equilibrium expected returns are given by E(ri) rf+Aiba + A2biz, where ry is the (annual) risk-free interest rate, and A1 and A2 are the risk premiums associated with factor 1 and 2. You estimate the following factor sensitivities for the four stocks: Stock i 0 bi b2 2,0 0 H 0,75 0 T 1,5 0 W 0,6 -0,3 a) Use Oljelund and H20Kraft to construct a risk-free portfolio. Assume that there are no restrictions on "short sales". If an investor invests EUR 100 000 in this portfolio, how is this amount divided between the two stocks? Problem 1 (Weight 60%; each question weighted equally) After completing your degree in finance from NHH you land job as an analyst for FACTORfinance. Your first task is to estimate expected returns and risk in Oljelund (O), H20Kraft (H), Telestor (T) and Wingekjos (W). After a thorough analysis you find that returns can be described by the following two-factor model, r=E(r)+bi Fi+bai F2, where E(-) represents expected returns, F and F are two macroeconomic factors with expectations equal to zero, and bi og b are the factor sensitivities for the return on stock i with respect to the factors F1 and F2, respectively. Your clients are large and well-diversified institutional investors, which means that you do not need to worry about firm-specific risk in your analysis. You find that equilibrium expected returns are given by E(ri) rf+Aiba + A2biz, where ry is the (annual) risk-free interest rate, and A1 and A2 are the risk premiums associated with factor 1 and 2. You estimate the following factor sensitivities for the four stocks: Stock i 0 bi b2 2,0 0 H 0,75 0 T 1,5 0 W 0,6 -0,3 a) Use Oljelund and H20Kraft to construct a risk-free portfolio. Assume that there are no restrictions on "short sales". If an investor invests EUR 100 000 in this portfolio, how is this amount divided between the two stocks?

Expert Answer:

Posted Date:

Students also viewed these finance questions

-

KYC's stock price can go up by 15 percent every year, or down by 10 percent. Both outcomes are equally likely. The risk free rate is 5 percent, and the current stock price of KYC is 100. (a) Price a...

-

MUST BE CORRECT ANSWERS A small software company has the following simplified cashflow, funded by shareholders' equity of 20,000 and a bank overdraft of 5000: Invoiced money received 2 months after...

-

The accompanying data are consistent with summary statistics that appeared in the paper Shape of Glass and Amount of Alcohol Poured: Comparative Study of Effect of Practice and Concentration (...

-

Classify each of the following accounts as an asset, liability, or stockholders equity. In the case of the assets, further classify them as current assets, long- term investments, property, plant,...

-

Journal entries (continuation of 8-29) Required 1. Prepare journal entries for variable and fixed manufacturing overhead (you will need to calculate the various variances to accomplish this). 2....

-

The efficiency ratio measures the relation between outputs from and inputs to a process. According to the WBCSD, a company wanting to become eco-efficient should strive to: 1.Reduce the material...

-

On January 1, 2016, Plymouth Corporation acquired 80 percent of the outstanding voting stock of Sander Company in exchange for $1,200,000 cash. At that time, although Sander's book value was...

-

Your task is to estimate VaR for an equity portfolio using the "Model-Building" approach. Suppose you have invested in two of the Fama-French factors, namely Mkt-RF and HML. Assume conditionally the...

-

You are finance director in a public sector organization that has experienced difficulty attracting and retaining skilled staff. To assist in overcoming this problem, the board has engaged a...

-

Consider the following table, which gives a security analyst's expected return on two stocks in two particular scenarios for the rate of return on the market: Market Return Aggressive Stock Defensive...

-

es Pretzelmania, Incorporated, issues 7%, 10-year bonds with a face amount of $64,000 for $64,000 on January 1, 2024. Interest is paid semiannually on June 30 and December 31. Required: 1. & 2....

-

Mr. Job's salary at the end of 1995 was USS25, 000.00 per annum. At the end of each year thereafter he received an increase of 7% of the previous years' salary. Find his salary at the end of 2009

-

find the efficiency for this binary symmetric channel P(y\x)= [0.1 0.9 0.11

-

The Walton Toy Company manufactures a line of dolls and a sewing kit. Demand for the company's products is increasing, and management requests assistance from you in determining an economical sales...

-

How did the cartels in Latin America manage to limit the flow of drugs in different markets? Why is the drug trade so profitable for illicit drug dealers? What is money laundering? How would drugs...

Study smarter with the SolutionInn App