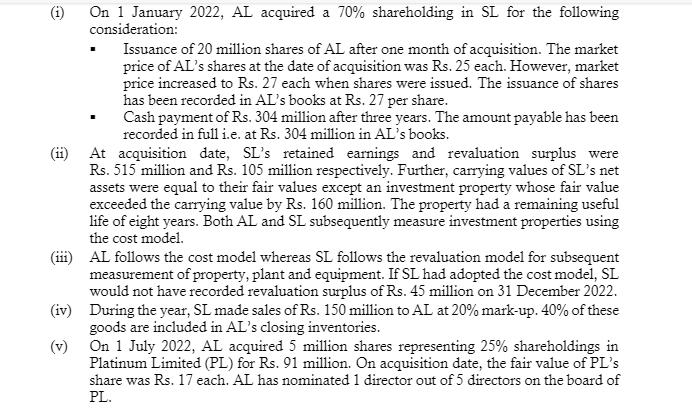

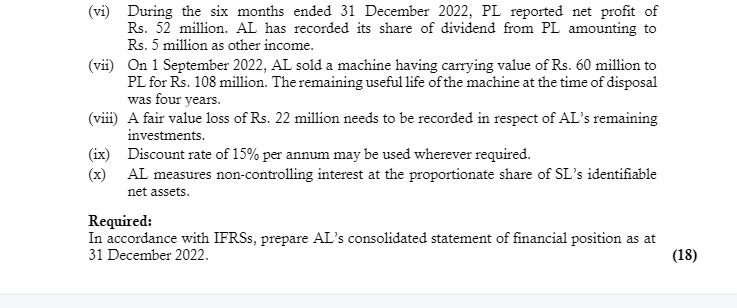

Q.8 Following are the summarized statements of financial position of Aluminium Limited (AL) and Silver Limited...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

To solve this problem well first calculate the contribution margin per unit and then determine the b... View the full answer

Related Book For

Posted Date: