Q1. Kramer claims that the standard deviation of return for the 50-50 portfolio of Groupon and Kinross

Question:

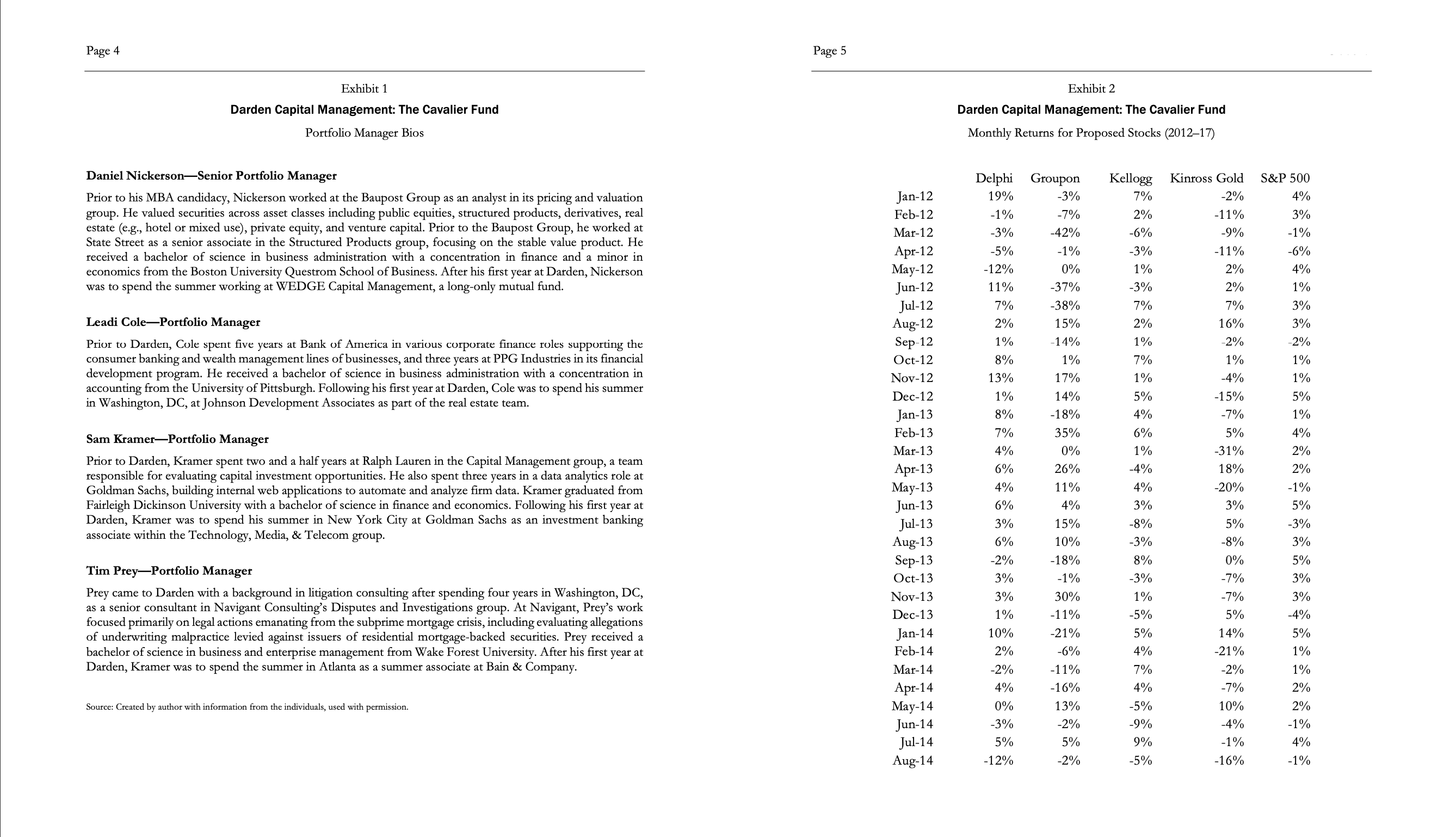

Q1.Kramer claims that the standard deviation of return for the 50-50 portfolio of Groupon and Kinross Gold is lower than the standard deviation of returns of a pure position in either Groupon or Kinross Gold stock alone. Compute the standard deviation and the expected return of the 50-50 portfolio. Do you agree with Kramer's argument?

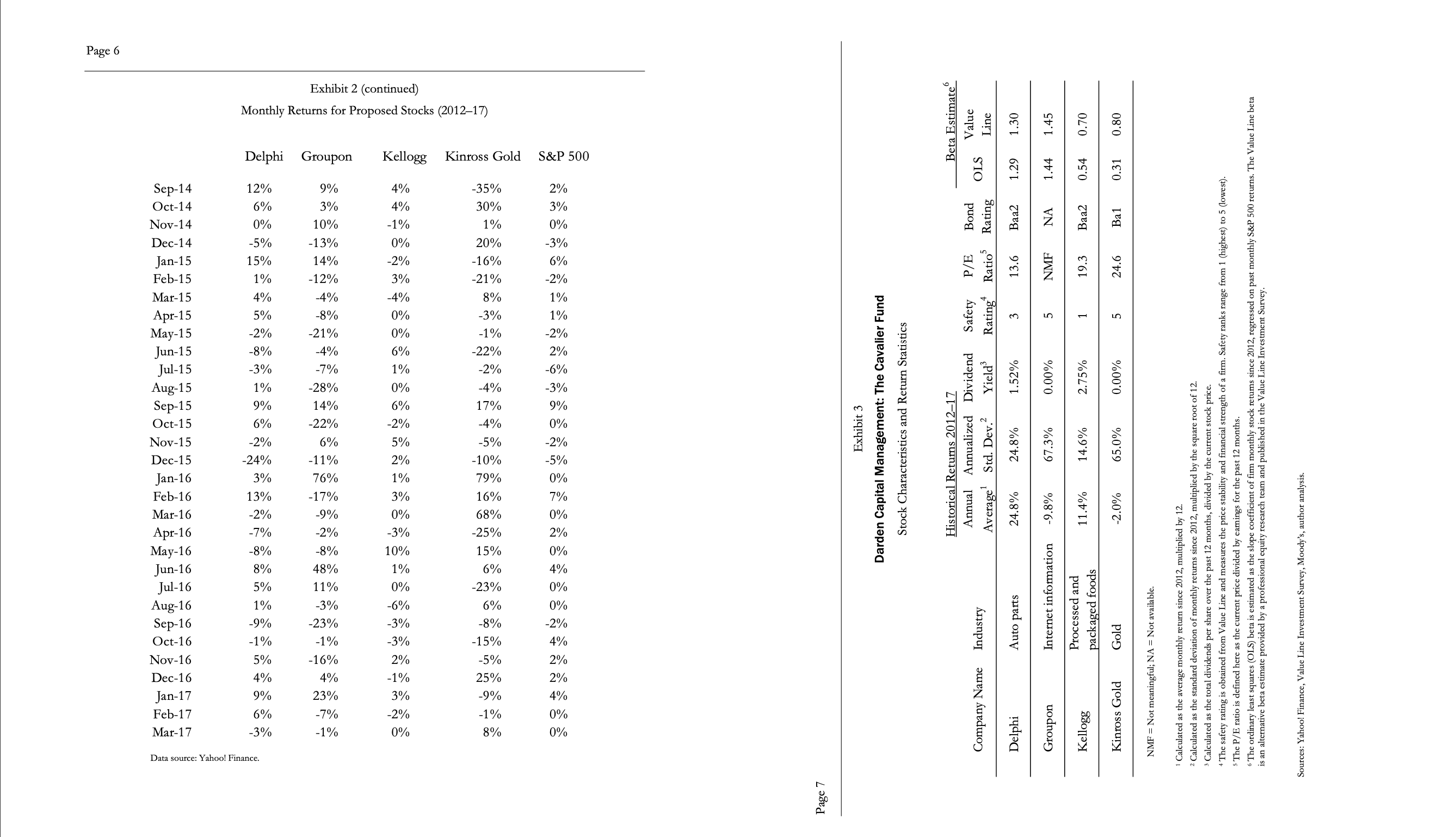

Q2.Exhibit 3 shows that Groupon and Kinross Gold have a similar annualized standard deviation. But why is Kinross Gold's beta so small compared to Groupon's?

Q3.Which of the four stocks should the Cavalier Fund pick? Explain answer.

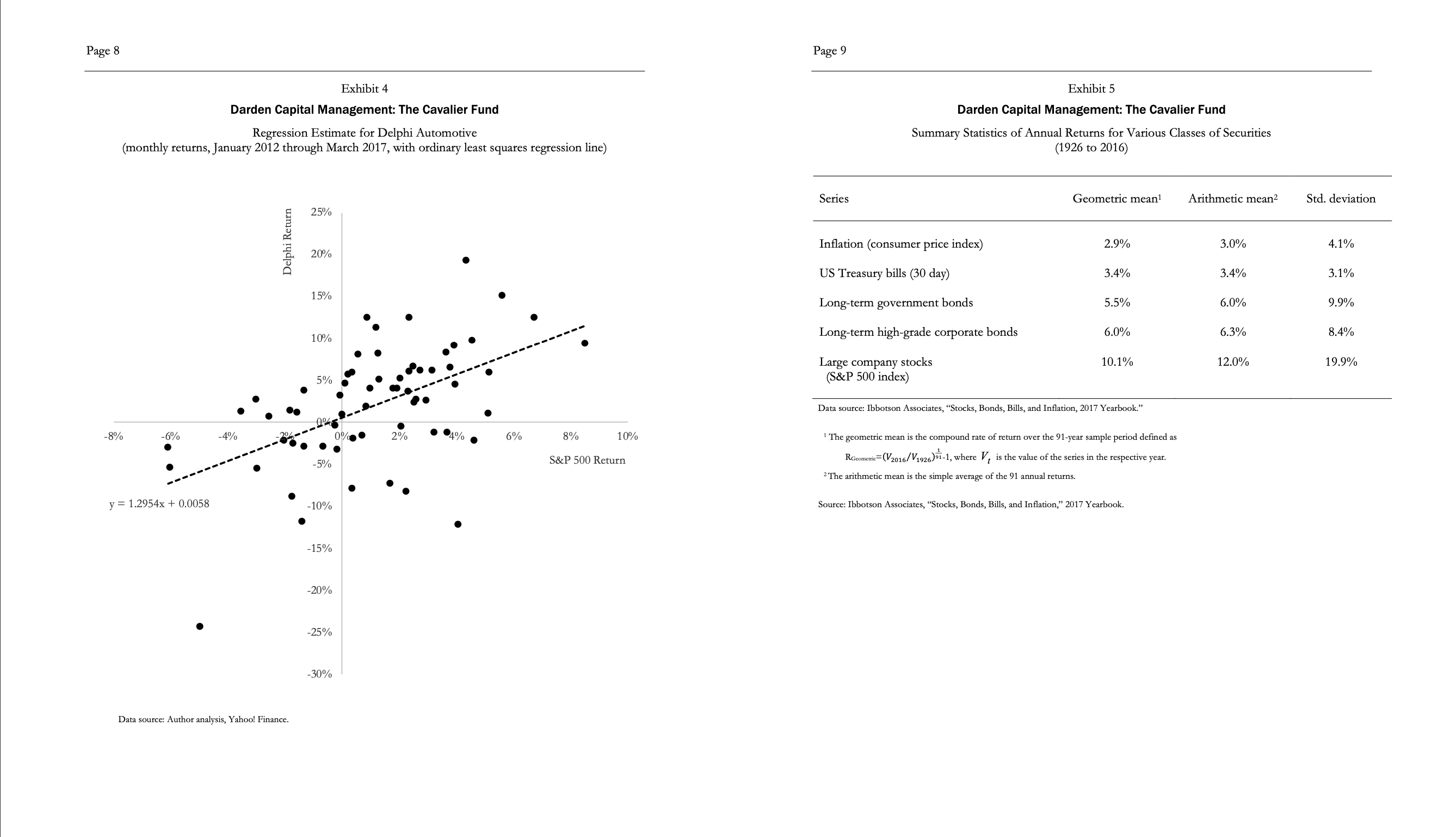

might even argue that the Cavalier Fund should not add any stocks at all. willing to accept any answers as long as provide good support for argument. However, recall that the Sharpe ratio is not the best benchmark for performance because it uses the total risk as a measure of the security risk.

- Compute the standard deviation

- The expected return of proposed portfolio investment

- Show understanding of the diversifiable risk by making a recommendation on the stock investment

Expert Answer: