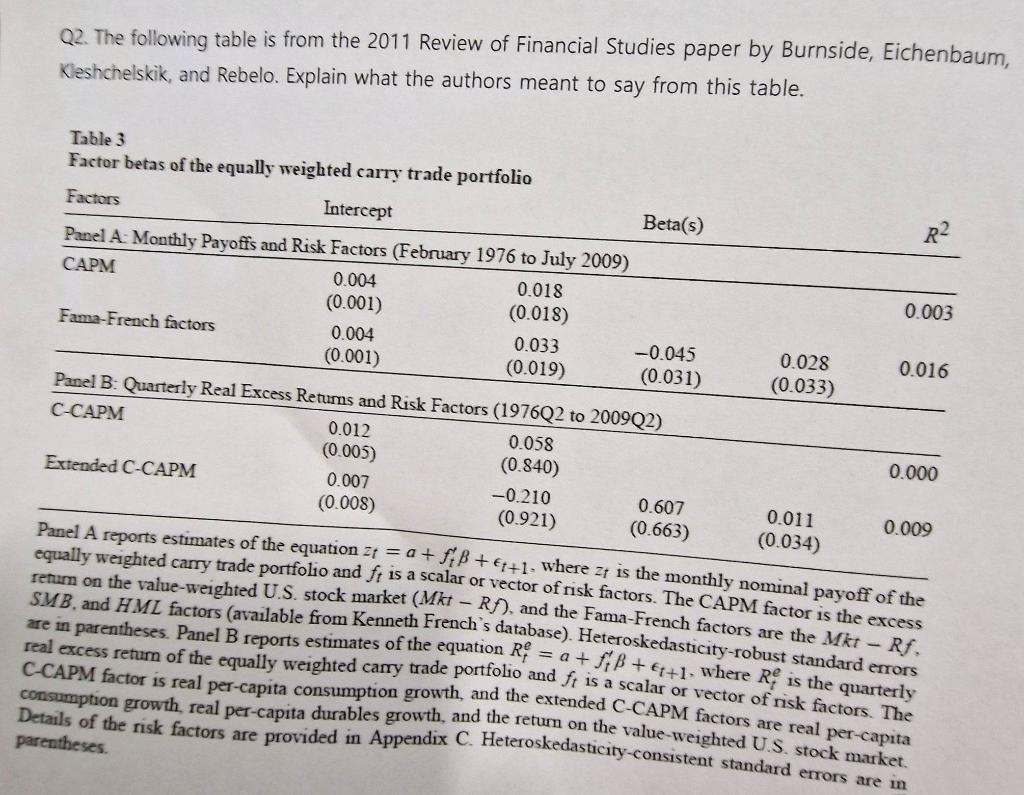

Q2. The following table is from the 2011 Review of Financial Studies paper by Burnside, Eichenbaum,...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

The table presented in the paper provides estimates of factor betas for the equally weighted carry t... View the full answer

Related Book For

Statistics The Art And Science Of Learning From Data

ISBN: 9780321755940

3rd Edition

Authors: Alan Agresti, Christine A. Franklin

Posted Date: