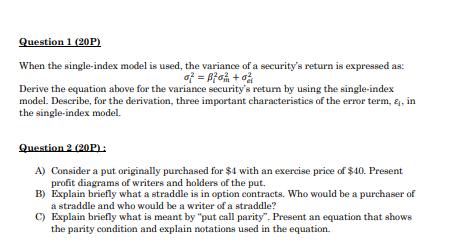

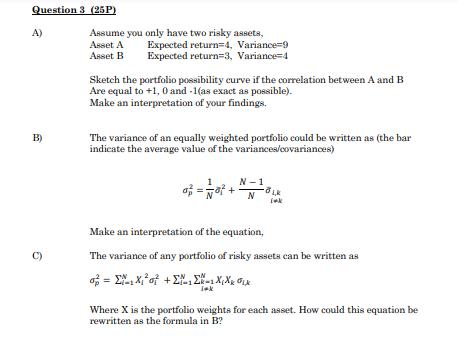

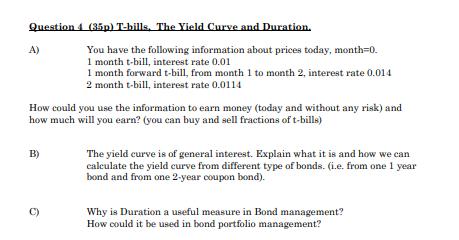

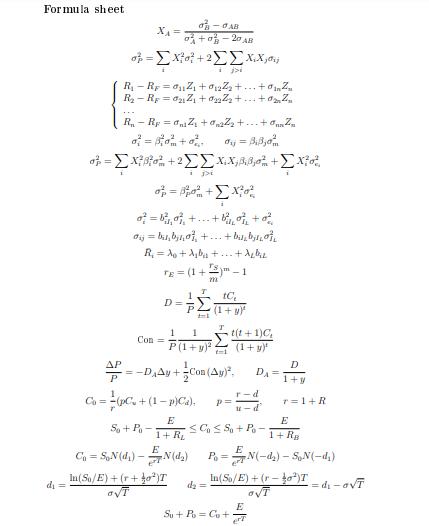

Question 1 (20P) When the single-index model is used, the variance of a security's return is...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Question 1 (20P) When the single-index model is used, the variance of a security's return is expressed as: o² = ²o +0² Derive the equation above for the variance security's return by using the single-index model. Describe, for the derivation, three important characteristics of the error term, &, in the single-index model. Question 2 (20P): A) Consider a put originally purchased for $4 with an exercise price of $40. Present profit diagrams of writers and holders of the put. B) Explain briefly what a straddle is in option contracts. Who would be a purchaser of a straddle and who would be a writer of a straddle? C) Explain briefly what is meant by "put call parity". Present an equation that shows the parity condition and explain notations used in the equation. Question 3 (25P) A) B) Assume you only have two risky assets, Asset A Expected return=4, Variance-9 Asset B Expected return=3, Variance 4 Sketch the portfolio possibility curve if the correlation between A and B Are equal to +1,0 and 1(as exact as possible). Make an interpretation of your findings. The variance of an equally weighted portfolio could be written as (the bar indicate the average value of the variances/covariances) 1 N-1 N -LK lak Make an interpretation of the equation, The variance of any portfolio of risky assets can be written as = ₁x₁² of +- Ex-XXx ₁x lak Where X is the portfolio weights for each asset. How could this equation be rewritten as the formula in B? Question A) 4 (35p) T-bills. The Yield Curve and Duration. You have the following information about prices today, month=0. 1 month t-bill, interest rate 0.01 1 month forward t-bill, from month 1 to month 2, interest rate 0.014 2 month t-bill, interest rate 0.0114 How could you use the information to earn money (today and without any risk) and how much will you earn? (you can buy and sell fractions of t-bills) B) The yield curve is of general interest. Explain what it is and how we can calculate the yield curve from different type of bonds. (i.e. from one 1 year bond and from one 2-year coupon bond). Why is Duration a useful measure in Bond management? How could it be used in bond portfolio management? Formula sheet d₁ = ΔΡ X₁ = +0 o = [X²0² + 2 ΣΣXiXj R₁ - R=₁₁Z₁ + 0₁22₂+...+0Z R₂-R=0₂1Z₁ +022 ²₂+...+0₂ ² R₁ - Rp = a₁Z₁ +0n2Z₂+...+0 Z₂ 2²=²0² +0². dj = B₂3,² o² = [X²²² +2ΣΣXX; +[X²² i pi ²=₁₁²++₁₁+0² TE= (1 + -AB aj = bu₂b₂,0], +...+b₁b₂,0 R₁ = A +₁₁+.+ debre D= Con= So + Po- 1 P -20 AB T In(S/E) + (r+²)T OVT 222 i 1 1 P(1+y)² d₂ = tC₂ (1 + y)² T =-D₁Ay+Con (Ay)² DA= t=1 t(t+1)C (1+y)¹ r-d u-d ≤co ≤ So + Po- Co= (pCu + (1-P)Ca), P= E 1 + R₂ C₁=S₂N (₁) N(d₂) P₁ = = N(-d₂) - SoN(-d₂) In(S/E)+(ro)T =d₁-ovī OVT Su + Po=Cu+ D 1+y E 27 T=1+R E 1+ RB Area under the standard normal distribution 0,09 0,00 0,01 0,02 0,03 0,04 0,05 0,06 0,0/ 0,08 0,0000 0,0040 0,0080 0,0120 0,0160 0,0199 0,0239 0,0279 0,0319 0,0359 0,0398 0,0438 0,0478 0,0517 0,0557 0,0596 0,0636 0,0675 0,0714 0,0753 0,0793 0,0832 0,0871 0,0910 0,0948 0,0987 0,1026 0,1064 0,1103 0,1141 0,1179 0,1217 0,1255 0,1293 0,1331 0,1368 0,1406 0,1443 0,1480 0,1517 0,1554 0,1591 0,1628 0,1664 0,1700 0,1736 0,1772 0,1808 0,1844 0,1879 0,1915 0,1950 0,1985 0,2019 0,2054 0,2088 0,2123 0,2157 0,2190 0,2224 0,2257 0,2291 0,2324 0,2357 0,2389 0,2422 0,2454 0,2486 0,2517 0,2549 0,2580 0,2611 0,2642 0,2673 0,2704 0,2734 0,2764 0,2794 0,2823 0,2852 0,2881 0,2910 0,2939 0,2967 0,2995 0,3023 0,3051 0,3078 0,3106 0,3133 0,3159 0,3186 0,3212 0,3238 0,3264 0,3289 0,3315 0,3340 0,3365 0,3389 0,3413 0,3438 0,3461 0,3485 0,3508 0,3531 0,3554 0,3577 0,3599 0,3621 0,3643 0,3665 0,3686 0,3708 0,3729 0,3749 0,3770 0,3790 0,3810 0,3830 0,3849 0,3869 0,3888 0,3907 0,3925 0,3944 0,3962 0,3980 0,3997 0,4015 0,4032 0,4049 0,4066 0,4082 0,4099 0,4115 0,4131 0,4147 0,4162 0,4177 0,4192 0,4207 0,4222 0,4236 0,4251 0,4265 0,4279 0,4292 0,4306 0,4319 0,4332 0,4345 0,4357 0,4370 0,4382 0,4394 0,4406 0,4418 0,4429 0,4441 0,4452 0,4463 0,4474 0,4484 0,4495 0,4505 0,4515 0,4525 0,4535 0,4545 0,4554 0,4564 0,4573 0,4582 0,4591 0,4599 0,4608 0,4616 0,4625 0,4633 0,4641 0,4649 0,4656 0,4664 0,4671 0,4678 0,4686 0,4693 0,4699 0,4706 0,4713 0,4719 0,4726 0,4732 0,4738 0,4744 0,4750 0,4756 0,4761 0,4767 0,4772 0,4778 0,4783 0,4788 0,4793 0,4798 0,4803 0,4808 0,4812 0,4817 2,1 0,4821 0,4826 0,4830 0,4834 0,4838 0,4842 0,4846 0,4850 0,4854 0,4857 2,2 0,4861 0,4864 0,4868 0,4871 0,4875 0,4878 0,4881 0,4884 0,4887 0,4890 2,3 0,4893 0,4896 0,4898 0,4901 0,4904 0,4906 0,4909 0,4911 0,4913 0,4916 2,4 0,4918 0,4920 0,4922 0,4925 0,4927 0,4929 0,4931 0,4932 0,4934 0,4936 0,4938 0,4940 0,4941 0,4943 0,4945 0,4946 0,4948 0,4949 0,4951 0,4952 0,4953 0,4955 0,4956 0,4957 0,4959 0,4960 0,4961 0,4962 0,4963 0,4964 0,4965 0,4966 0,4967 0,4968 0,4969 0,4970 0,4971 0,4972 0,4973 0,4974 0,4974 0,4975 0,4976 0,4977 0,4977 0,4978 0,4979 0,4979 0,4980 0,4981 0,4981 0,4982 0,4982 0,4983 0,4984 0,4984 0,4985 0,4985 0,4986 0,4986 0,4987 0,4987 0,4987 0,4988 0,4988 0,4989 0,4989 0,4989 0,4990 0,4990 z 0 0,1 0,2 0,3 0,4 0,5 0,6 0,7 0,8 0,9 1 1,1 1,2 1,3 1,4 1,5 1,6 1,7 1,8 1,9 2 NO 2,5 2,6 2,7 2,8 2,9 3 Question 1 (20P) When the single-index model is used, the variance of a security's return is expressed as: o² = ²o +0² Derive the equation above for the variance security's return by using the single-index model. Describe, for the derivation, three important characteristics of the error term, &, in the single-index model. Question 2 (20P): A) Consider a put originally purchased for $4 with an exercise price of $40. Present profit diagrams of writers and holders of the put. B) Explain briefly what a straddle is in option contracts. Who would be a purchaser of a straddle and who would be a writer of a straddle? C) Explain briefly what is meant by "put call parity". Present an equation that shows the parity condition and explain notations used in the equation. Question 3 (25P) A) B) Assume you only have two risky assets, Asset A Expected return=4, Variance-9 Asset B Expected return=3, Variance 4 Sketch the portfolio possibility curve if the correlation between A and B Are equal to +1,0 and 1(as exact as possible). Make an interpretation of your findings. The variance of an equally weighted portfolio could be written as (the bar indicate the average value of the variances/covariances) 1 N-1 N -LK lak Make an interpretation of the equation, The variance of any portfolio of risky assets can be written as = ₁x₁² of +- Ex-XXx ₁x lak Where X is the portfolio weights for each asset. How could this equation be rewritten as the formula in B? Question A) 4 (35p) T-bills. The Yield Curve and Duration. You have the following information about prices today, month=0. 1 month t-bill, interest rate 0.01 1 month forward t-bill, from month 1 to month 2, interest rate 0.014 2 month t-bill, interest rate 0.0114 How could you use the information to earn money (today and without any risk) and how much will you earn? (you can buy and sell fractions of t-bills) B) The yield curve is of general interest. Explain what it is and how we can calculate the yield curve from different type of bonds. (i.e. from one 1 year bond and from one 2-year coupon bond). Why is Duration a useful measure in Bond management? How could it be used in bond portfolio management? Formula sheet d₁ = ΔΡ X₁ = +0 o = [X²0² + 2 ΣΣXiXj R₁ - R=₁₁Z₁ + 0₁22₂+...+0Z R₂-R=0₂1Z₁ +022 ²₂+...+0₂ ² R₁ - Rp = a₁Z₁ +0n2Z₂+...+0 Z₂ 2²=²0² +0². dj = B₂3,² o² = [X²²² +2ΣΣXX; +[X²² i pi ²=₁₁²++₁₁+0² TE= (1 + -AB aj = bu₂b₂,0], +...+b₁b₂,0 R₁ = A +₁₁+.+ debre D= Con= So + Po- 1 P -20 AB T In(S/E) + (r+²)T OVT 222 i 1 1 P(1+y)² d₂ = tC₂ (1 + y)² T =-D₁Ay+Con (Ay)² DA= t=1 t(t+1)C (1+y)¹ r-d u-d ≤co ≤ So + Po- Co= (pCu + (1-P)Ca), P= E 1 + R₂ C₁=S₂N (₁) N(d₂) P₁ = = N(-d₂) - SoN(-d₂) In(S/E)+(ro)T =d₁-ovī OVT Su + Po=Cu+ D 1+y E 27 T=1+R E 1+ RB Area under the standard normal distribution 0,09 0,00 0,01 0,02 0,03 0,04 0,05 0,06 0,0/ 0,08 0,0000 0,0040 0,0080 0,0120 0,0160 0,0199 0,0239 0,0279 0,0319 0,0359 0,0398 0,0438 0,0478 0,0517 0,0557 0,0596 0,0636 0,0675 0,0714 0,0753 0,0793 0,0832 0,0871 0,0910 0,0948 0,0987 0,1026 0,1064 0,1103 0,1141 0,1179 0,1217 0,1255 0,1293 0,1331 0,1368 0,1406 0,1443 0,1480 0,1517 0,1554 0,1591 0,1628 0,1664 0,1700 0,1736 0,1772 0,1808 0,1844 0,1879 0,1915 0,1950 0,1985 0,2019 0,2054 0,2088 0,2123 0,2157 0,2190 0,2224 0,2257 0,2291 0,2324 0,2357 0,2389 0,2422 0,2454 0,2486 0,2517 0,2549 0,2580 0,2611 0,2642 0,2673 0,2704 0,2734 0,2764 0,2794 0,2823 0,2852 0,2881 0,2910 0,2939 0,2967 0,2995 0,3023 0,3051 0,3078 0,3106 0,3133 0,3159 0,3186 0,3212 0,3238 0,3264 0,3289 0,3315 0,3340 0,3365 0,3389 0,3413 0,3438 0,3461 0,3485 0,3508 0,3531 0,3554 0,3577 0,3599 0,3621 0,3643 0,3665 0,3686 0,3708 0,3729 0,3749 0,3770 0,3790 0,3810 0,3830 0,3849 0,3869 0,3888 0,3907 0,3925 0,3944 0,3962 0,3980 0,3997 0,4015 0,4032 0,4049 0,4066 0,4082 0,4099 0,4115 0,4131 0,4147 0,4162 0,4177 0,4192 0,4207 0,4222 0,4236 0,4251 0,4265 0,4279 0,4292 0,4306 0,4319 0,4332 0,4345 0,4357 0,4370 0,4382 0,4394 0,4406 0,4418 0,4429 0,4441 0,4452 0,4463 0,4474 0,4484 0,4495 0,4505 0,4515 0,4525 0,4535 0,4545 0,4554 0,4564 0,4573 0,4582 0,4591 0,4599 0,4608 0,4616 0,4625 0,4633 0,4641 0,4649 0,4656 0,4664 0,4671 0,4678 0,4686 0,4693 0,4699 0,4706 0,4713 0,4719 0,4726 0,4732 0,4738 0,4744 0,4750 0,4756 0,4761 0,4767 0,4772 0,4778 0,4783 0,4788 0,4793 0,4798 0,4803 0,4808 0,4812 0,4817 2,1 0,4821 0,4826 0,4830 0,4834 0,4838 0,4842 0,4846 0,4850 0,4854 0,4857 2,2 0,4861 0,4864 0,4868 0,4871 0,4875 0,4878 0,4881 0,4884 0,4887 0,4890 2,3 0,4893 0,4896 0,4898 0,4901 0,4904 0,4906 0,4909 0,4911 0,4913 0,4916 2,4 0,4918 0,4920 0,4922 0,4925 0,4927 0,4929 0,4931 0,4932 0,4934 0,4936 0,4938 0,4940 0,4941 0,4943 0,4945 0,4946 0,4948 0,4949 0,4951 0,4952 0,4953 0,4955 0,4956 0,4957 0,4959 0,4960 0,4961 0,4962 0,4963 0,4964 0,4965 0,4966 0,4967 0,4968 0,4969 0,4970 0,4971 0,4972 0,4973 0,4974 0,4974 0,4975 0,4976 0,4977 0,4977 0,4978 0,4979 0,4979 0,4980 0,4981 0,4981 0,4982 0,4982 0,4983 0,4984 0,4984 0,4985 0,4985 0,4986 0,4986 0,4987 0,4987 0,4987 0,4988 0,4988 0,4989 0,4989 0,4989 0,4990 0,4990 z 0 0,1 0,2 0,3 0,4 0,5 0,6 0,7 0,8 0,9 1 1,1 1,2 1,3 1,4 1,5 1,6 1,7 1,8 1,9 2 NO 2,5 2,6 2,7 2,8 2,9 3

Expert Answer:

Answer rating: 100% (QA)

Question 1 In the singleindex model the variance of a securitys return can be expressed as VarRi i2 VarRm Vari where VarRi is the variance of the securitys return i is the beta coefficient of the secu... View the full answer

Related Book For

Applied Regression Analysis and Other Multivariable Methods

ISBN: 978-1285051086

5th edition

Authors: David G. Kleinbaum, Lawrence L. Kupper, Azhar Nizam, Eli S. Rosenberg

Posted Date:

Students also viewed these finance questions

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

Question 1: Case Study Question (60 marks) Okinawa Blades plc (short OB) needs to order supplies two months ahead of the delivery date. It is considering an order from a Japanese supplier that...

-

Assume that you have a European call option and put an option with an exercise price of 9,000 won and a maturity of 3 months and another european call option and put option with the same maturity and...

-

People who earn a higher salary can afford more goods, including health care. However, according to Grossman, they will choose a higher desired health stock. Why is this so, according to the model?

-

Consider each of the following scenarios separately, assuming the company accounts for the arrangement: Scenario 1: Crown Construction Company enters into a contract with Star Hotel for building a...

-

What volume of n-hexane is required to decrease the concentration of X in Problem 31-11 to 1.00 x 10-4 M if 25.0 mL of 0.0500 M X is extracted with (a) 25.0-mL portions? (b) 10.0-mL portions? (c)...

-

Find a sample settlement agreement. Of those covered in this chapter, what type of settlement agreement did you find?

-

Suppose the marginal cost of writing a contract of length L is MC(L) = 10 + 2L. Find the optimal contract length when the marginal benefit of writing a contract is: a. MB(L) = 100. b. MB(L) = 150. c....

-

Identify and discuss the relation of Strategies (PESTLE, Porter's Five forces, the important P's) of a business and the Operations Management of a business. (Explain how do they complement each...

-

Laurman, Inc. is considering a new project and has provided the details of the project. The Controller has asked you to compute various capital budgeting methods to help aid in the decision to pursue...

-

Discuss important steps needed by the manufacturer to capitalize every possible advantage for business sustainability.

-

Describe the concept of the life cycle object, how it relates to collection objects, and give an example of a life cycle class with appropriate attributes.

-

Solve the following boundary value problem: \[y^{\prime \prime}(x)=f(x), \quad y(0)=0, \quad y(1)=0\] Hence solve \(y^{\prime \prime}(x)=x^{2}\) subject to the same boundary conditions.

-

Solve the following initial value problem using Laplace transform: (a) \[\frac{d y}{d t}=-y+e^{-3 t}, \quad y(0)=2\] (b) \[\frac{d y}{d t}+11 y=3, \quad y(0)=-2\] (c) \[\frac{d y}{d t}+2 y=2 e^{7 t},...

-

Show that the following eight vectors are pairwise orthogonal: \[\begin{aligned}& s 1=(1,1,0,0,0,0,0,0)^{T} \\& s 2=(0,0,1,1,0,0,0,0)^{T} \\& s 3=(0,0,0,0,1,1,0,0)^{T} \\& s 4=(0,0,,0,0,0,1,1)^{T}...

-

Evaluate machine XYZ on the basis of the PW method when the MARR is $12 \%$ per year. Pertinent cost data are as follows: Investment cost Useful life Market value Annual operating cost Overhaul cost...

-

A project manager assigned to an engineering construction project is receiving questions from the site engineers. Several questions are related to carrying out activities to meet timelines that...

-

Wilsons Auto Repair ended 2011 with Accounts Receivable of $85,000 and a credit balance in Allowance for Uncollectible Accounts balance of $11,000. During 2012, Wilsons Auto Repair had the following...

-

Sales revenue (Y) and advertising expenditure (X) data for a large retailer for the period 1988-1993 are given in the following table. a. Does the plot of Y versus X suggest that a linear...

-

The following table and accompanying computer output present data on the uric acid level found in the bloodstreams of persons with Down's syndrome and in the bloodstreams of nonDown's syndrome...

-

In September 1996, U.S. News & World Report published a report on America's health maintenance organizations (HMOs). The report was intended to serve as a consumer guide to HMO quality. For each HMO...

-

Share-based payments to employees are trued up by the end of the vesting period. If the plan is cash-settled, for what factors is it trued up? If it is equity-settled?

-

Assume that a Canadian company sells a product to a U.S. customer, and that the sale is denominated in U.S. dollars. What kind of a derivative instrument will eliminate the exchange risk? How will...

-

Explain the terms of a SARs program for employees.

Study smarter with the SolutionInn App