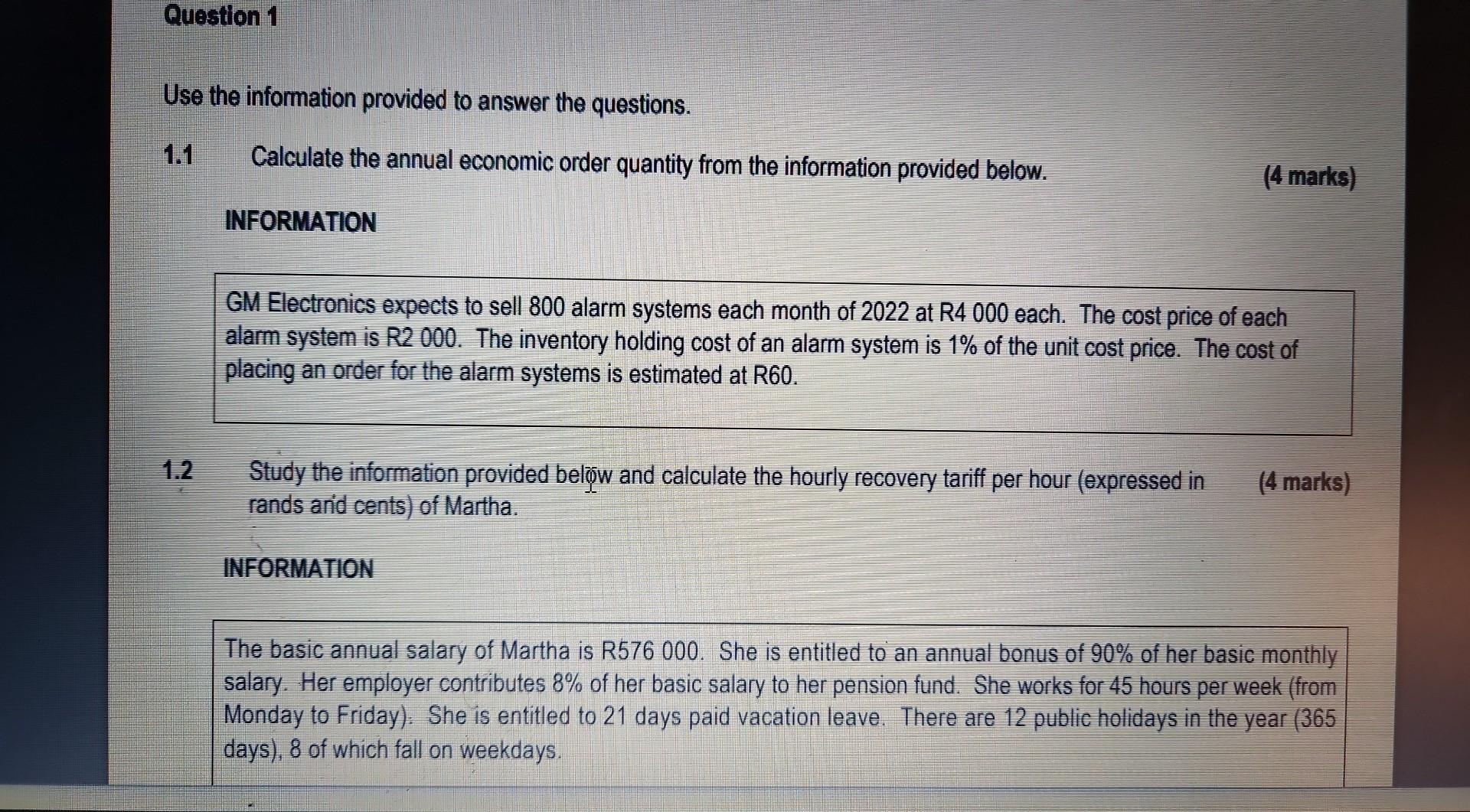

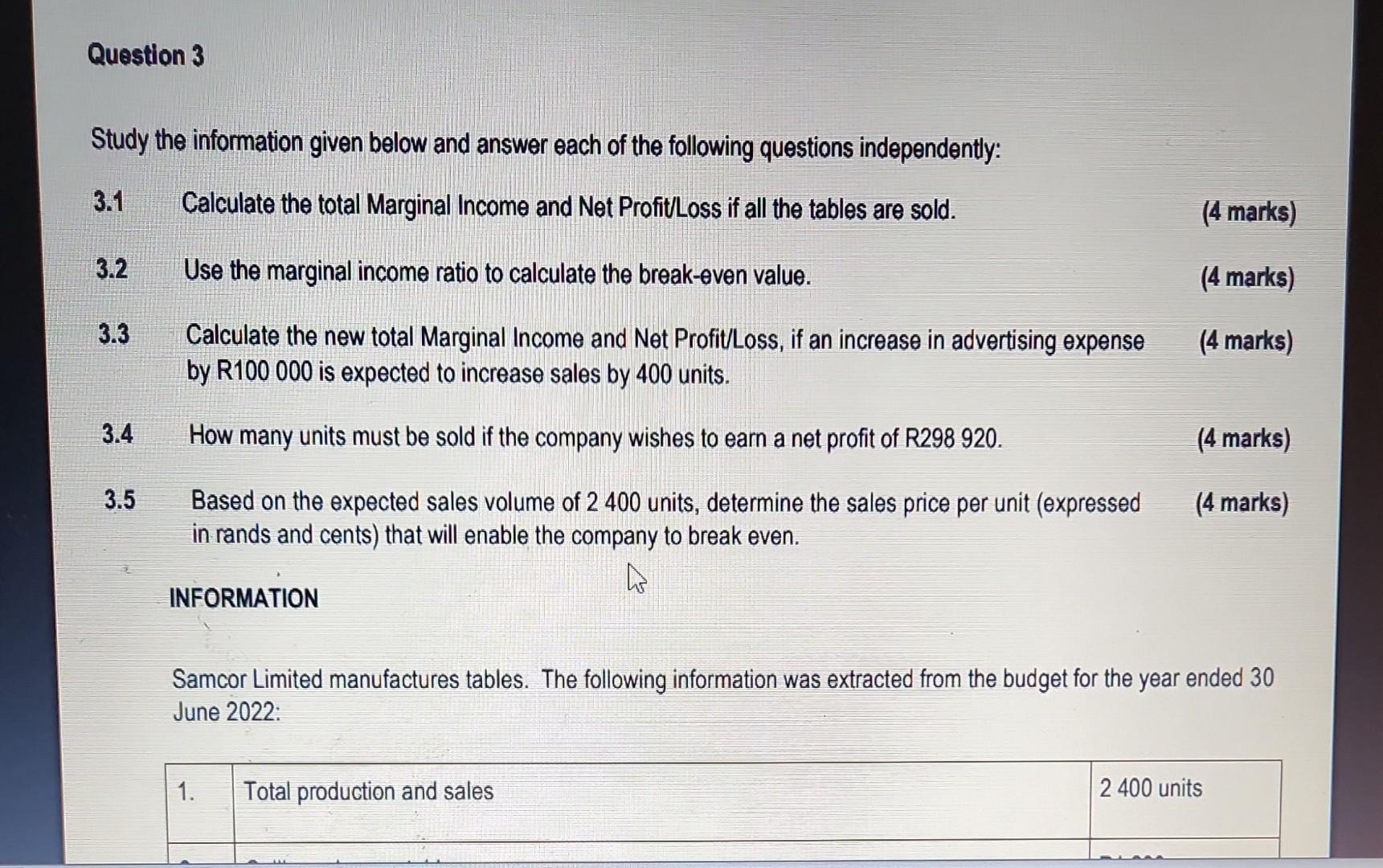

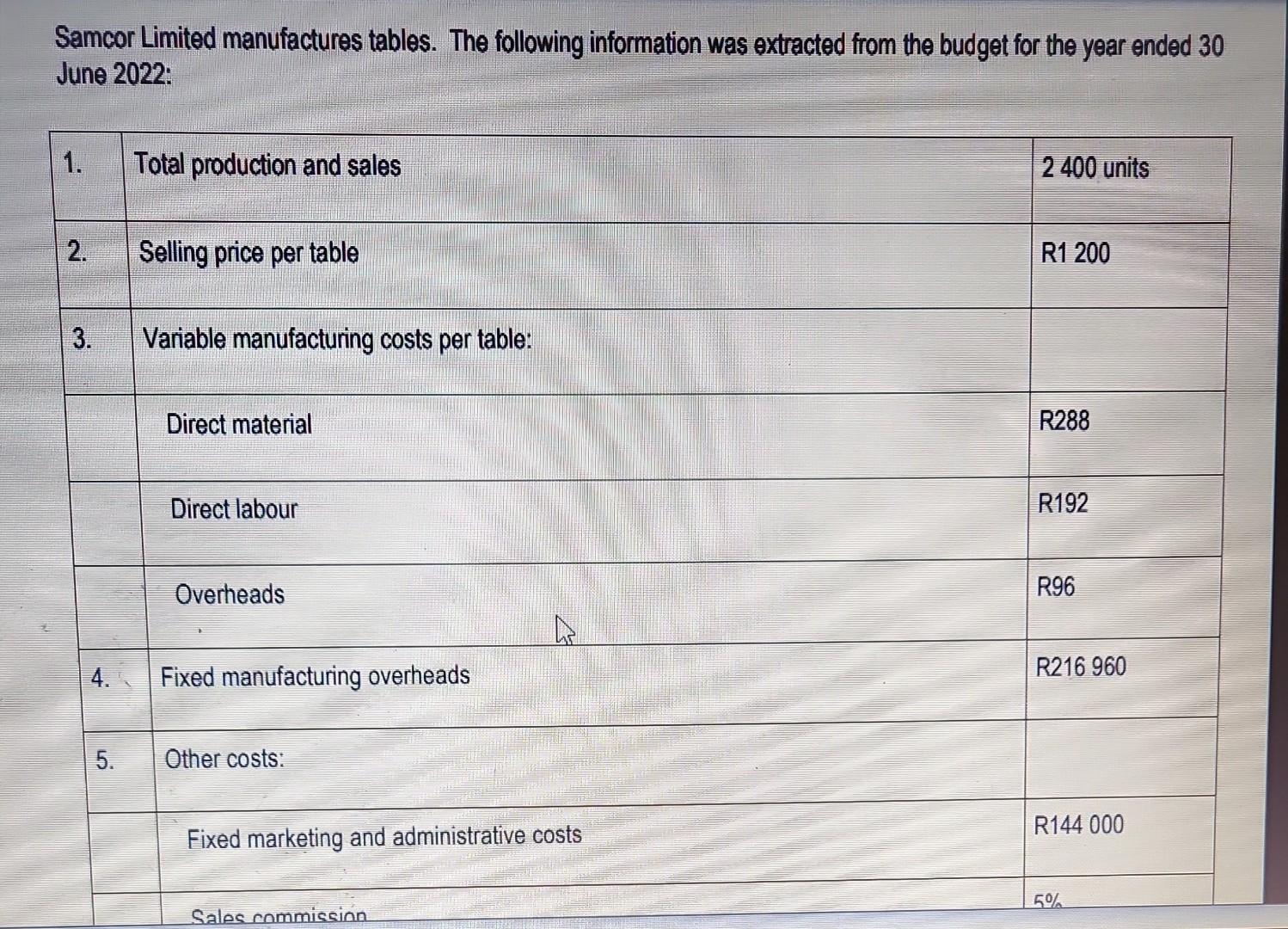

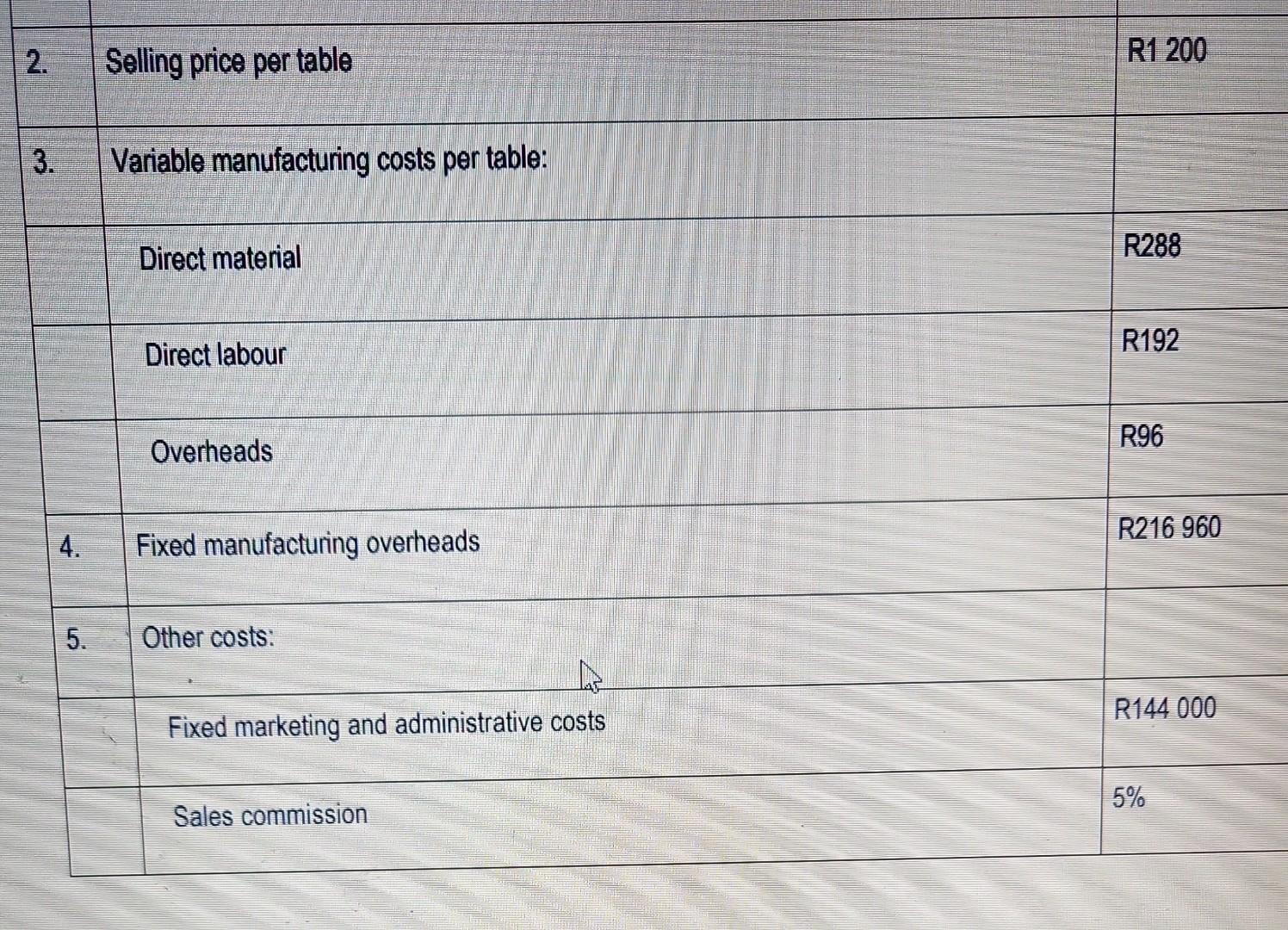

Question: Question 1 Use the information provided to answer the questions. 1.1 1.2 Calculate the annual economic order quantity from the information provided below. INFORMATION GM

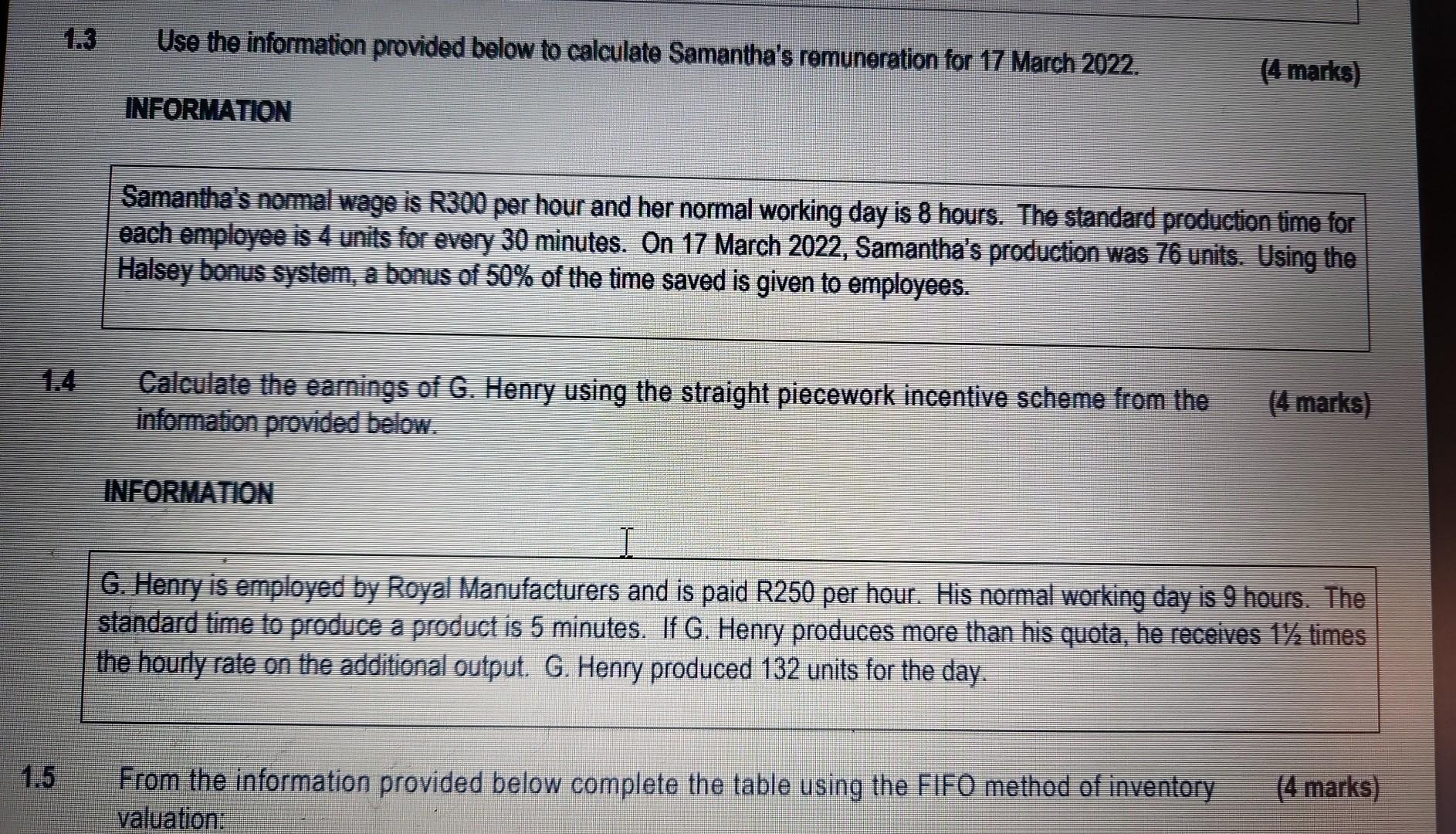

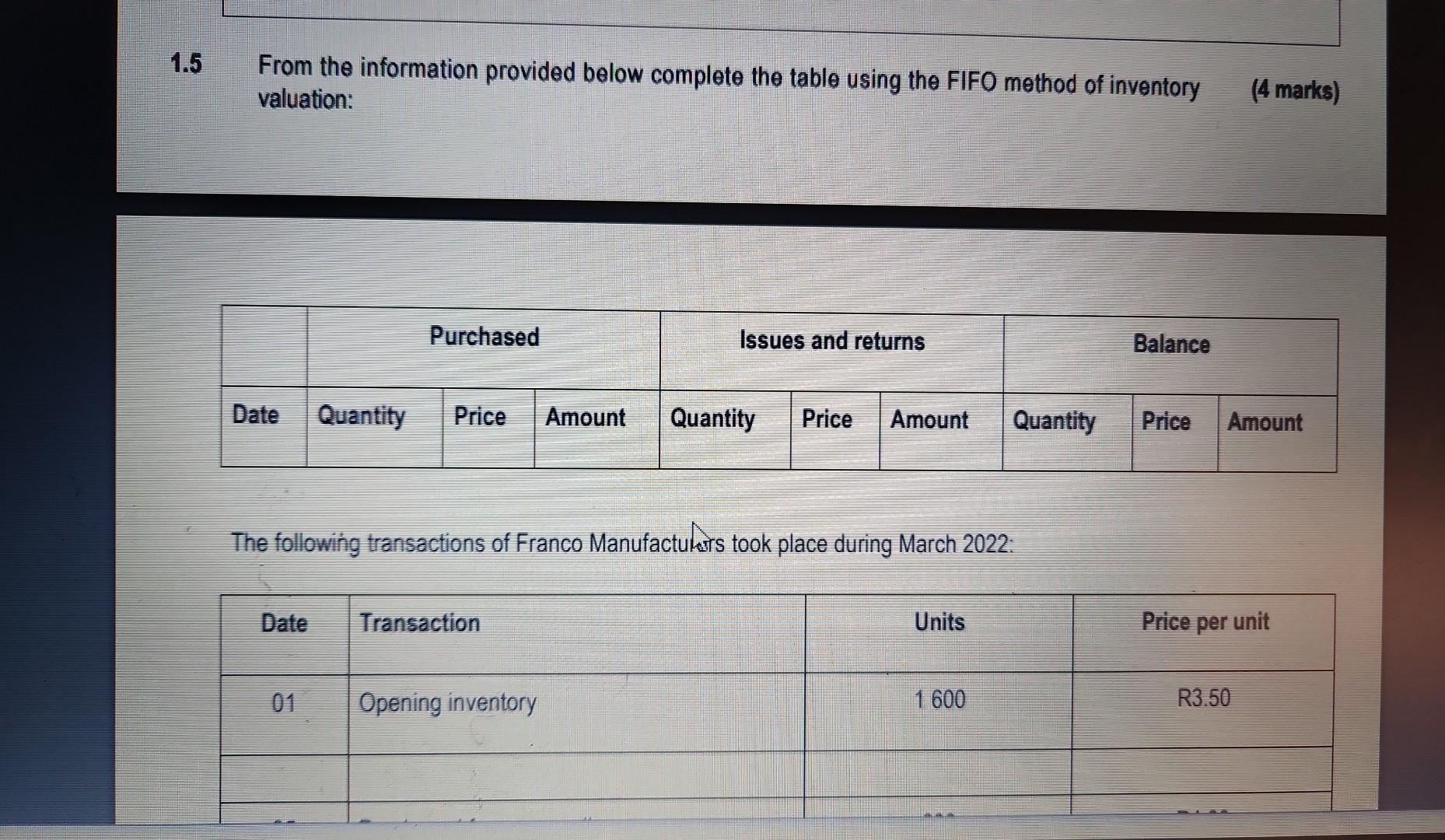

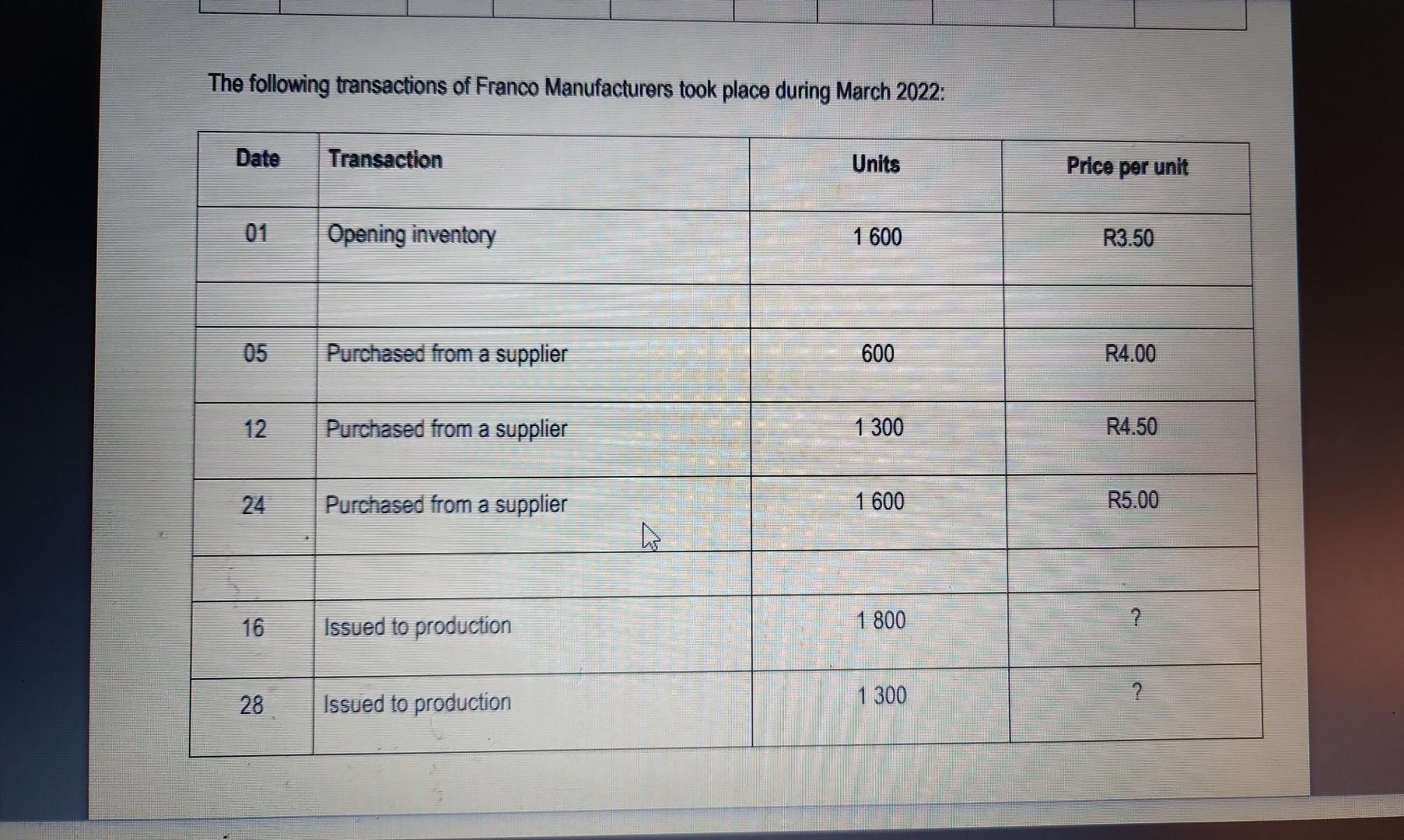

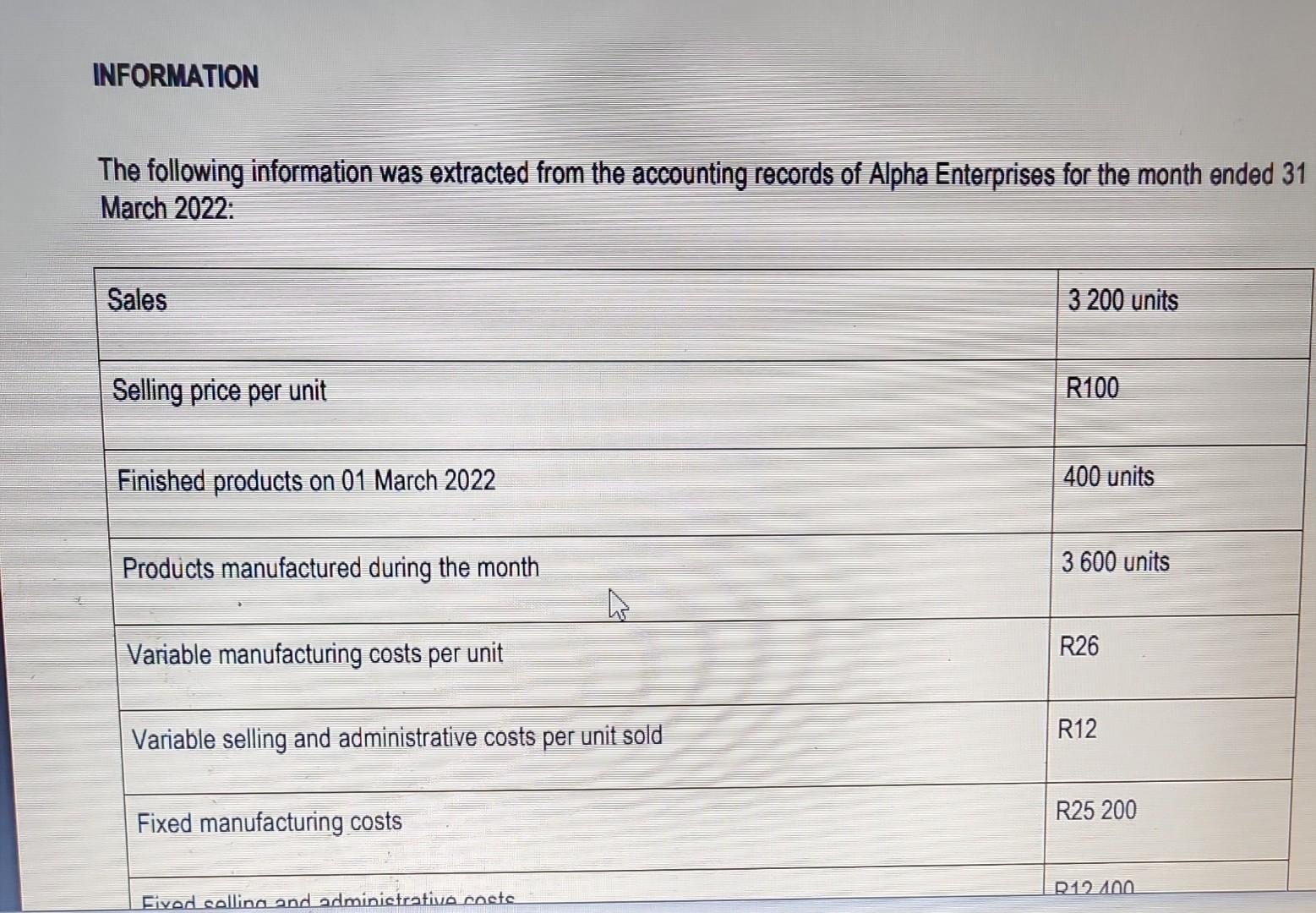

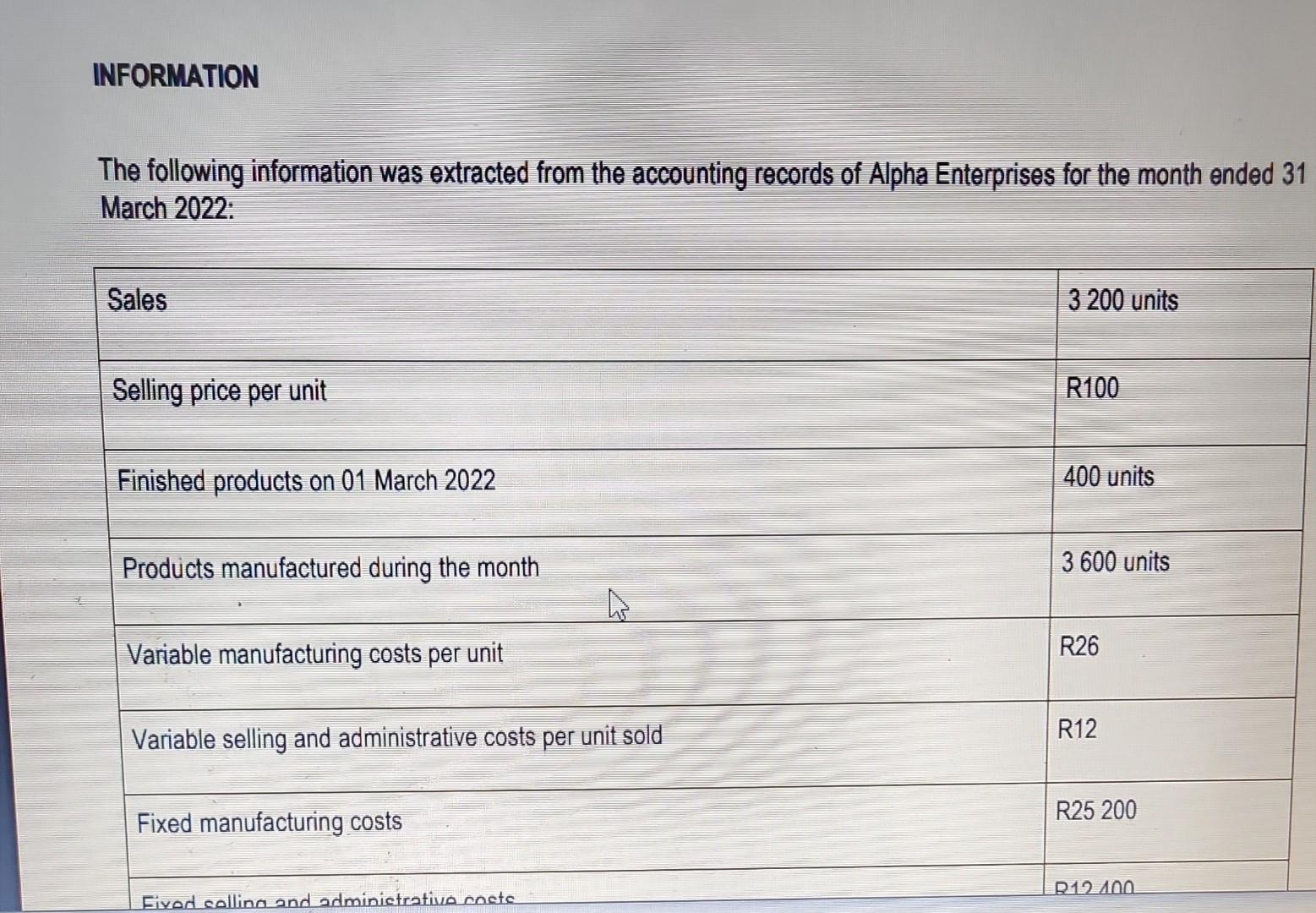

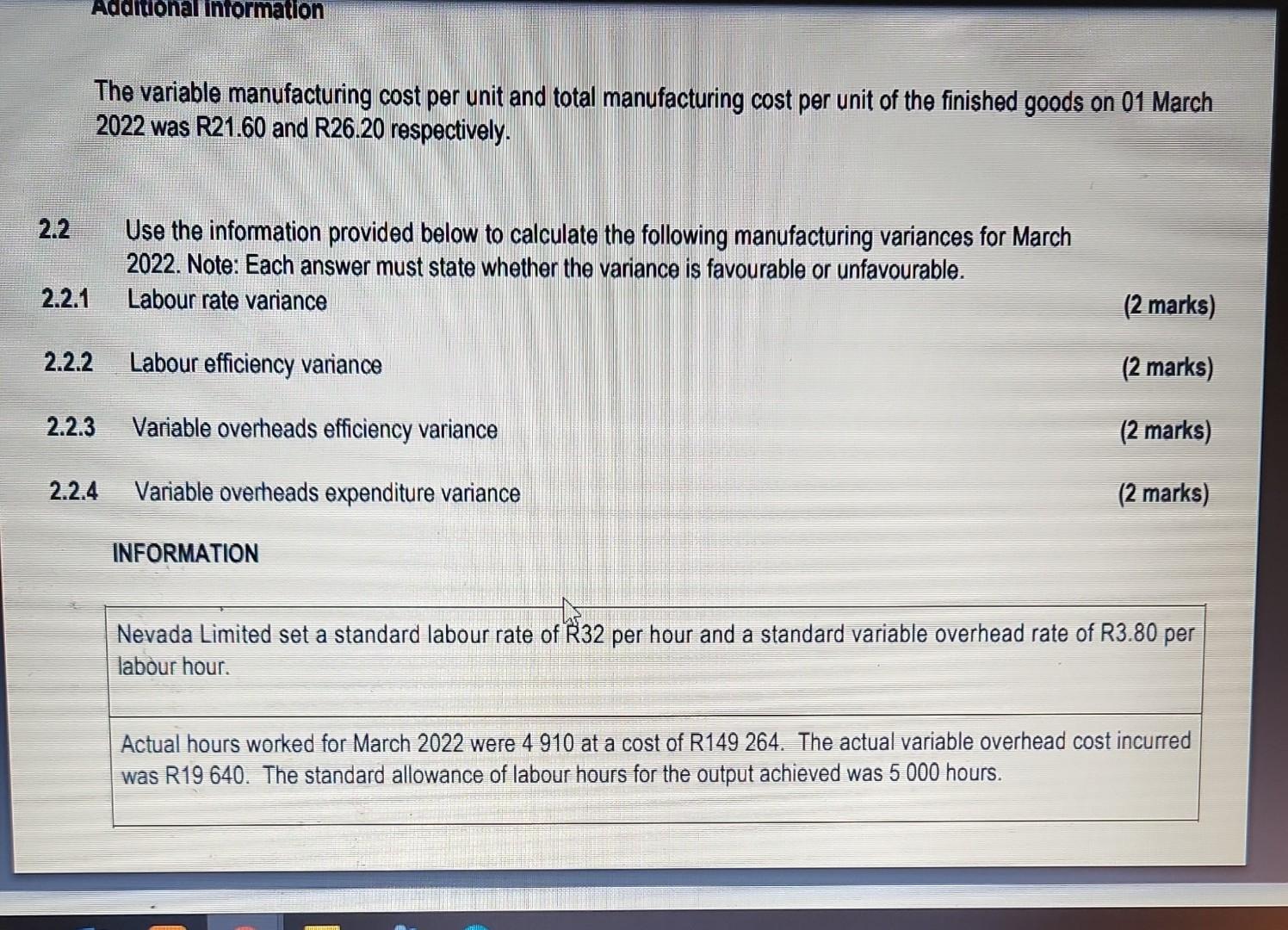

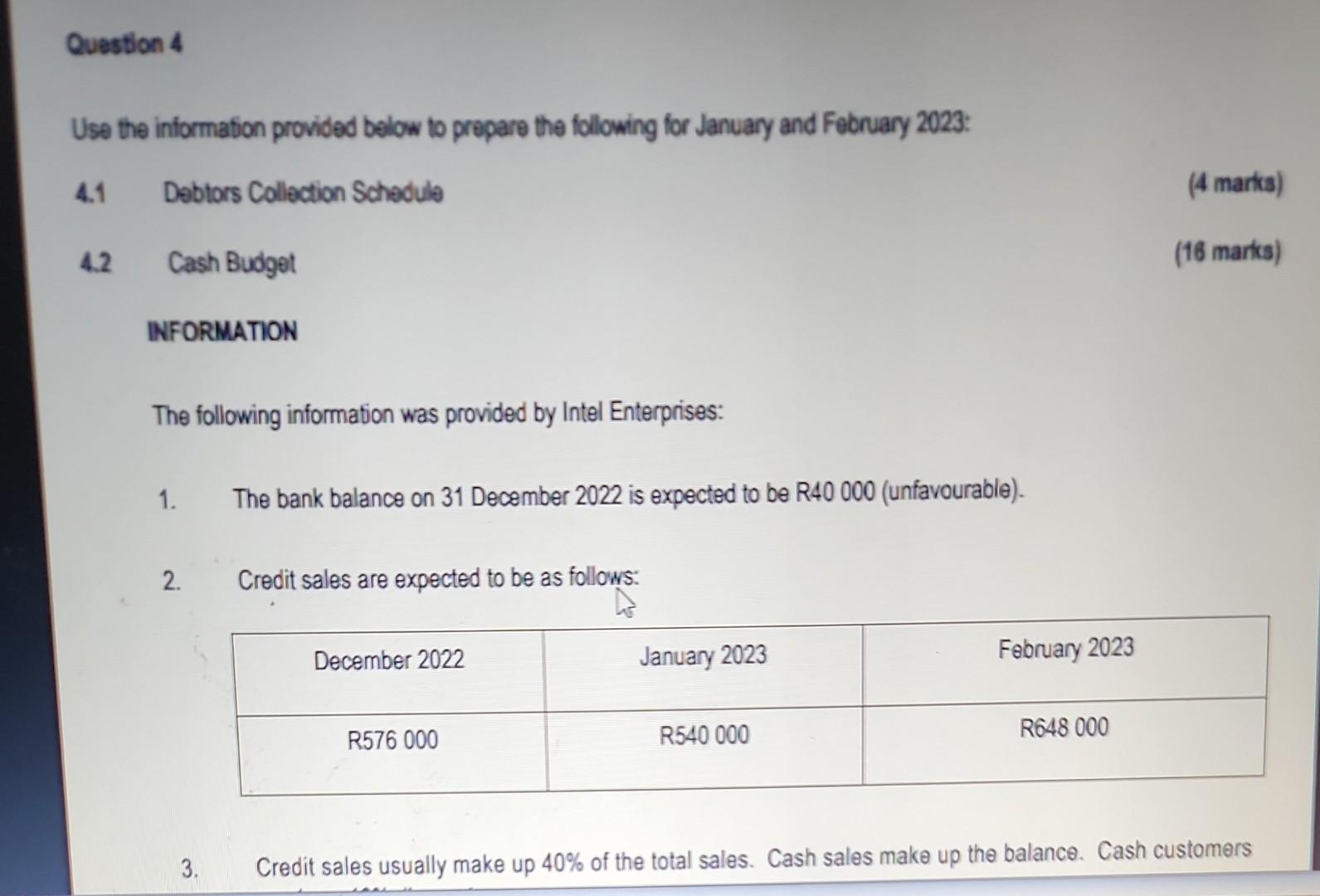

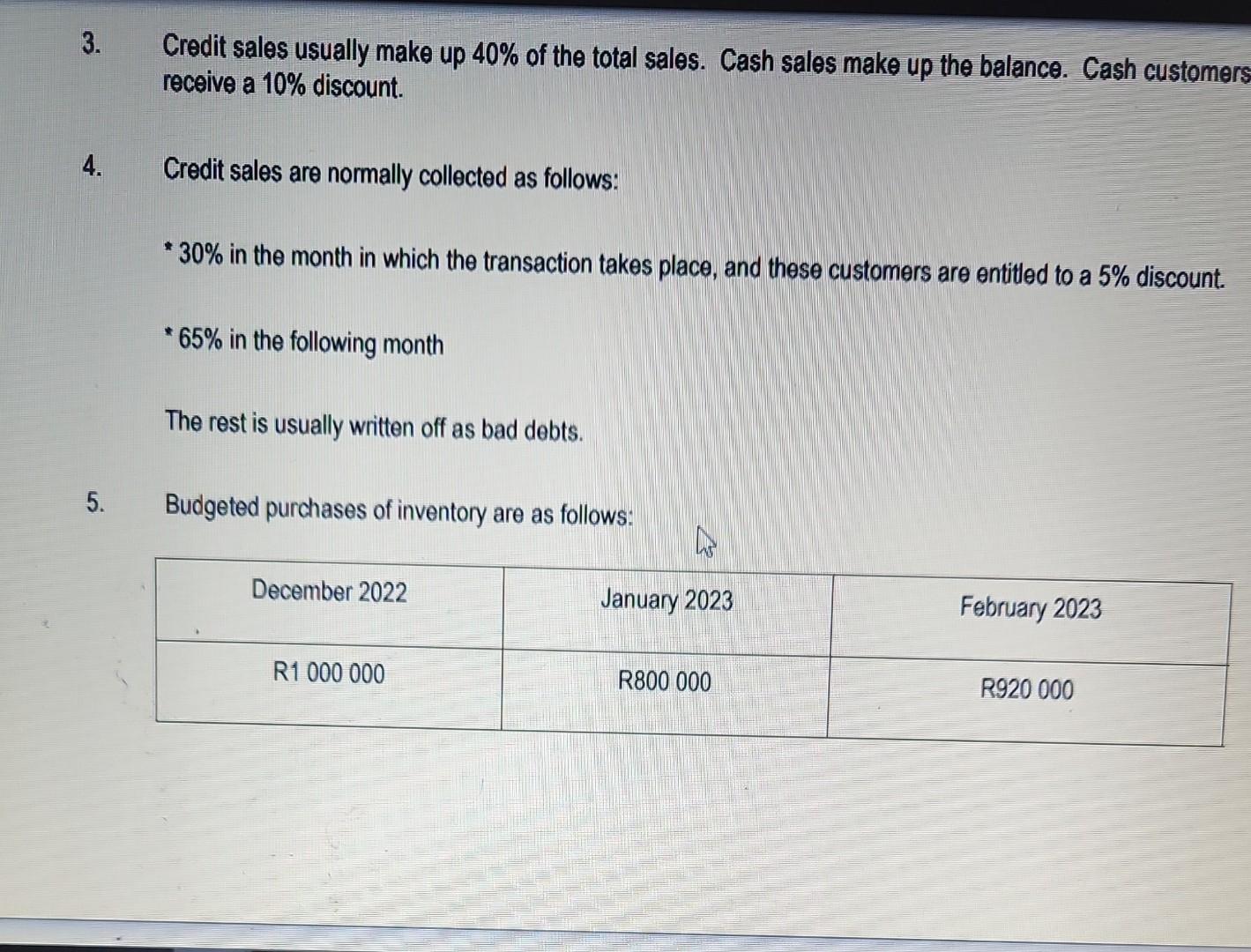

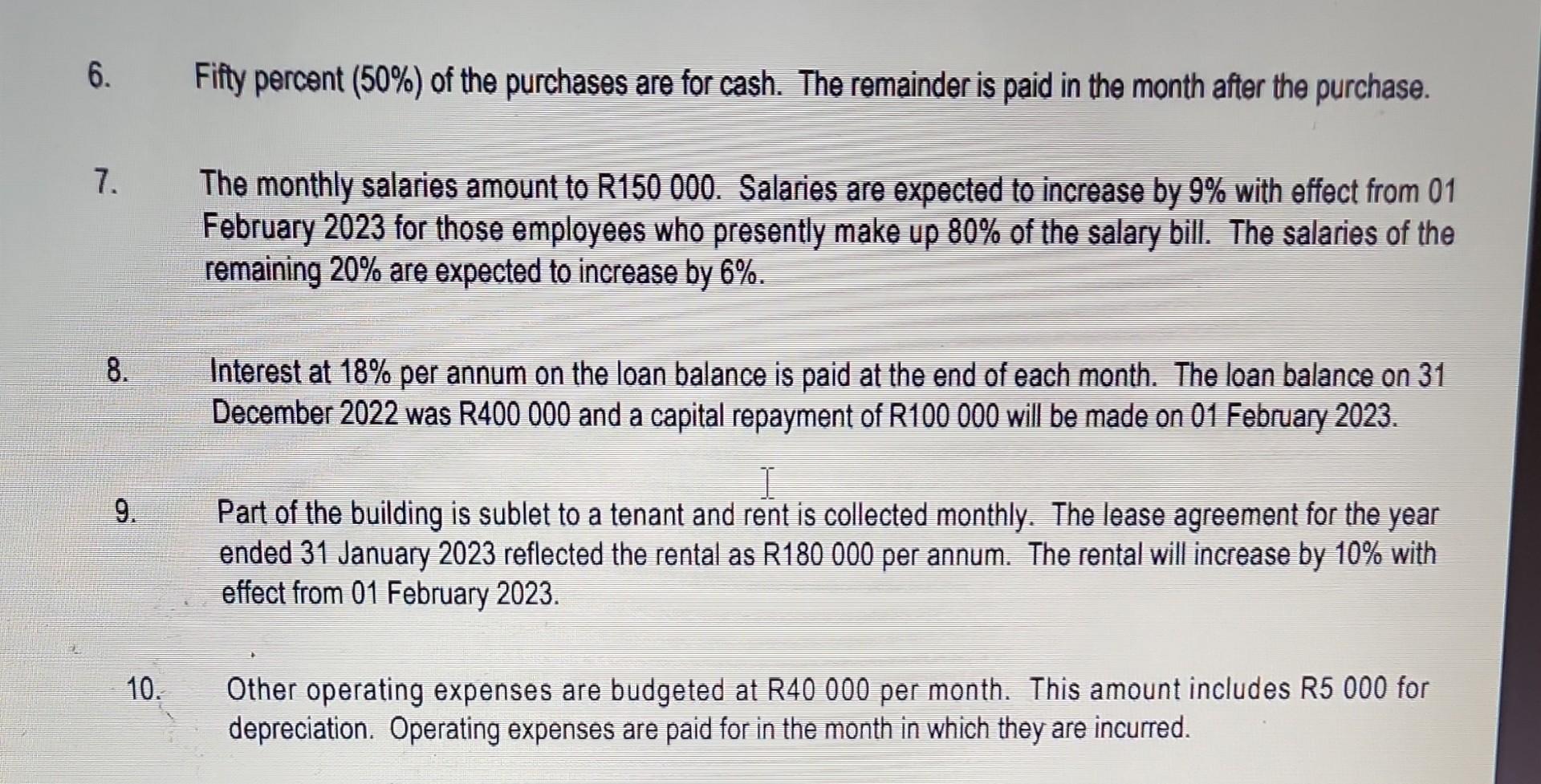

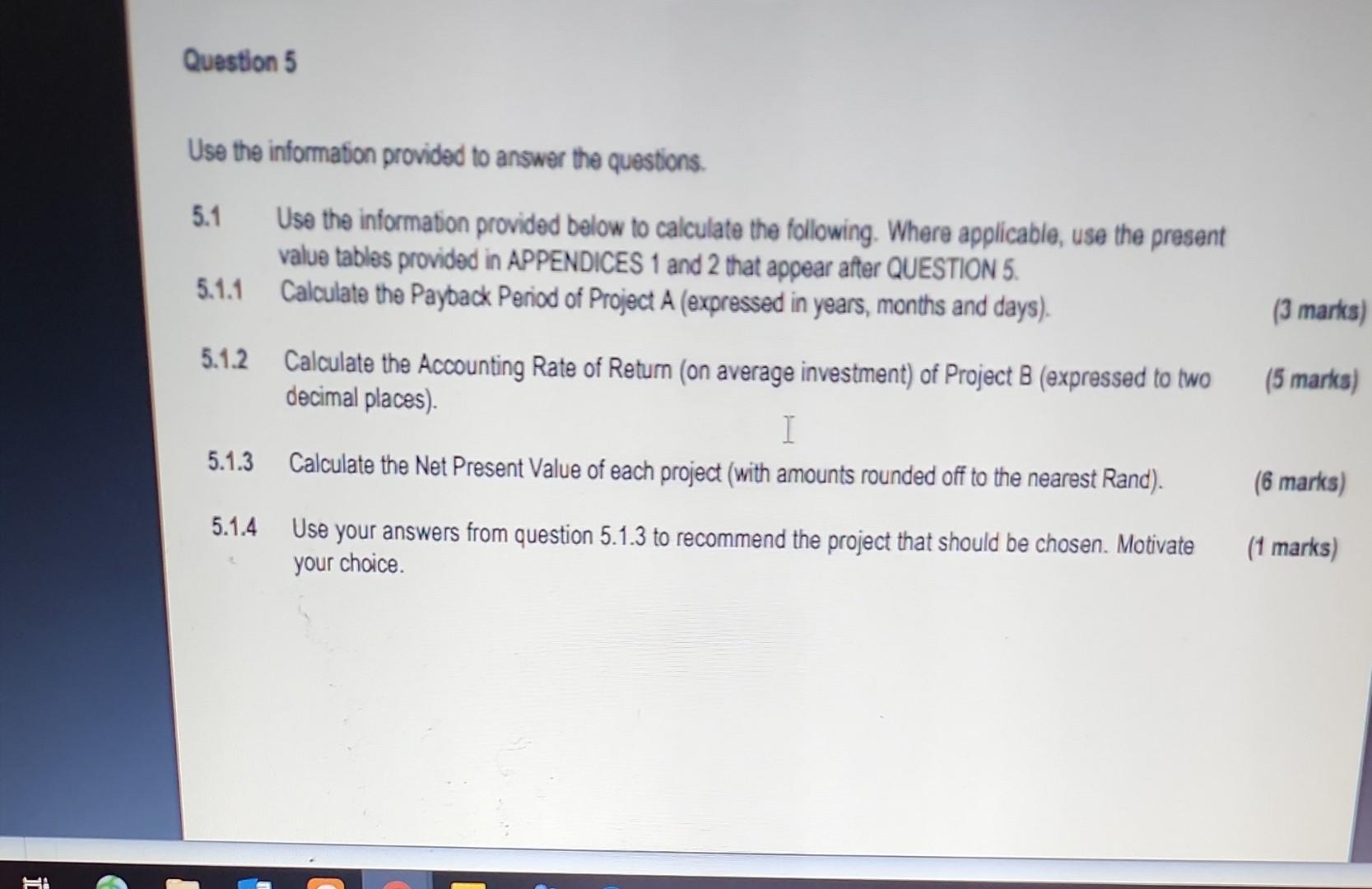

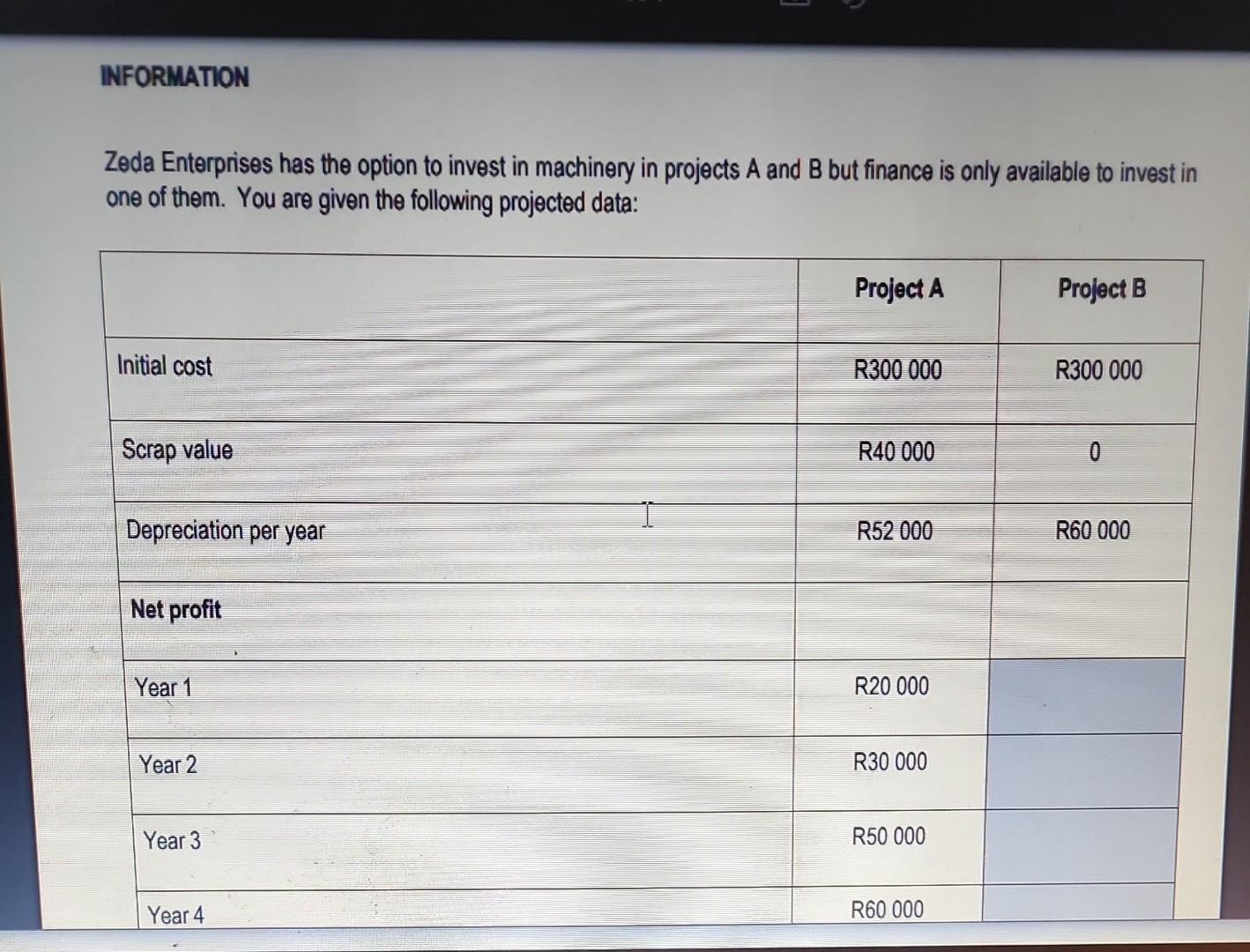

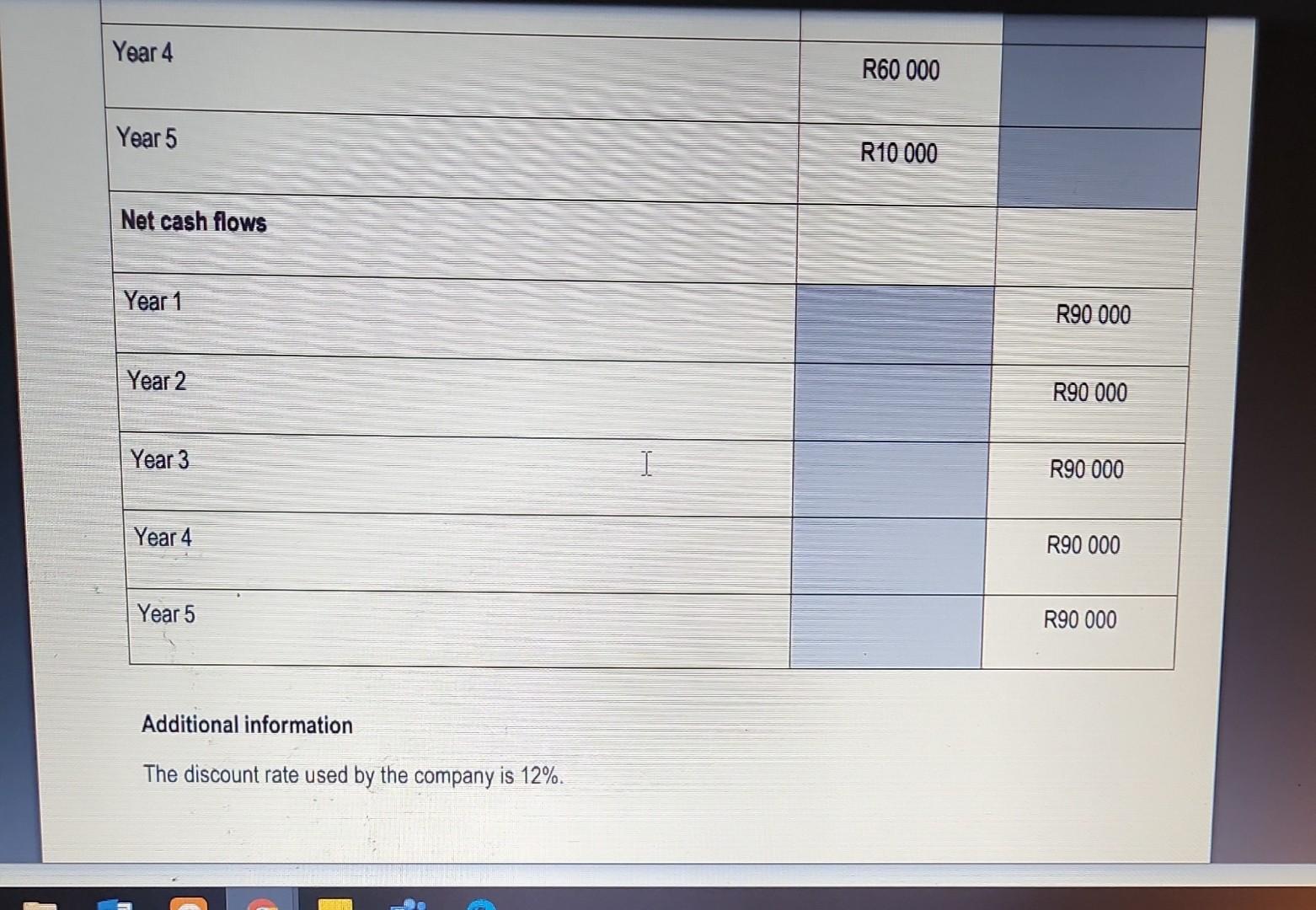

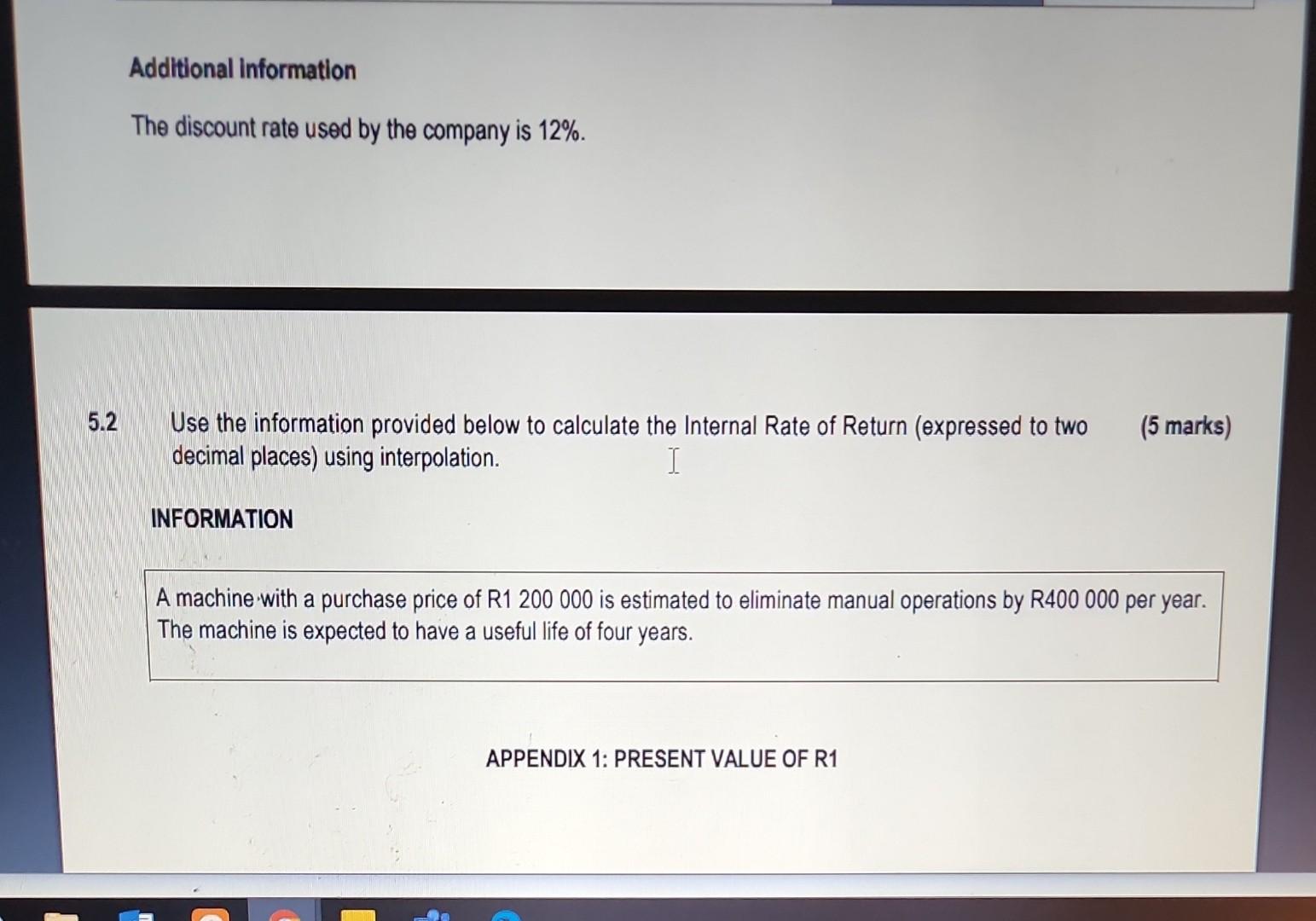

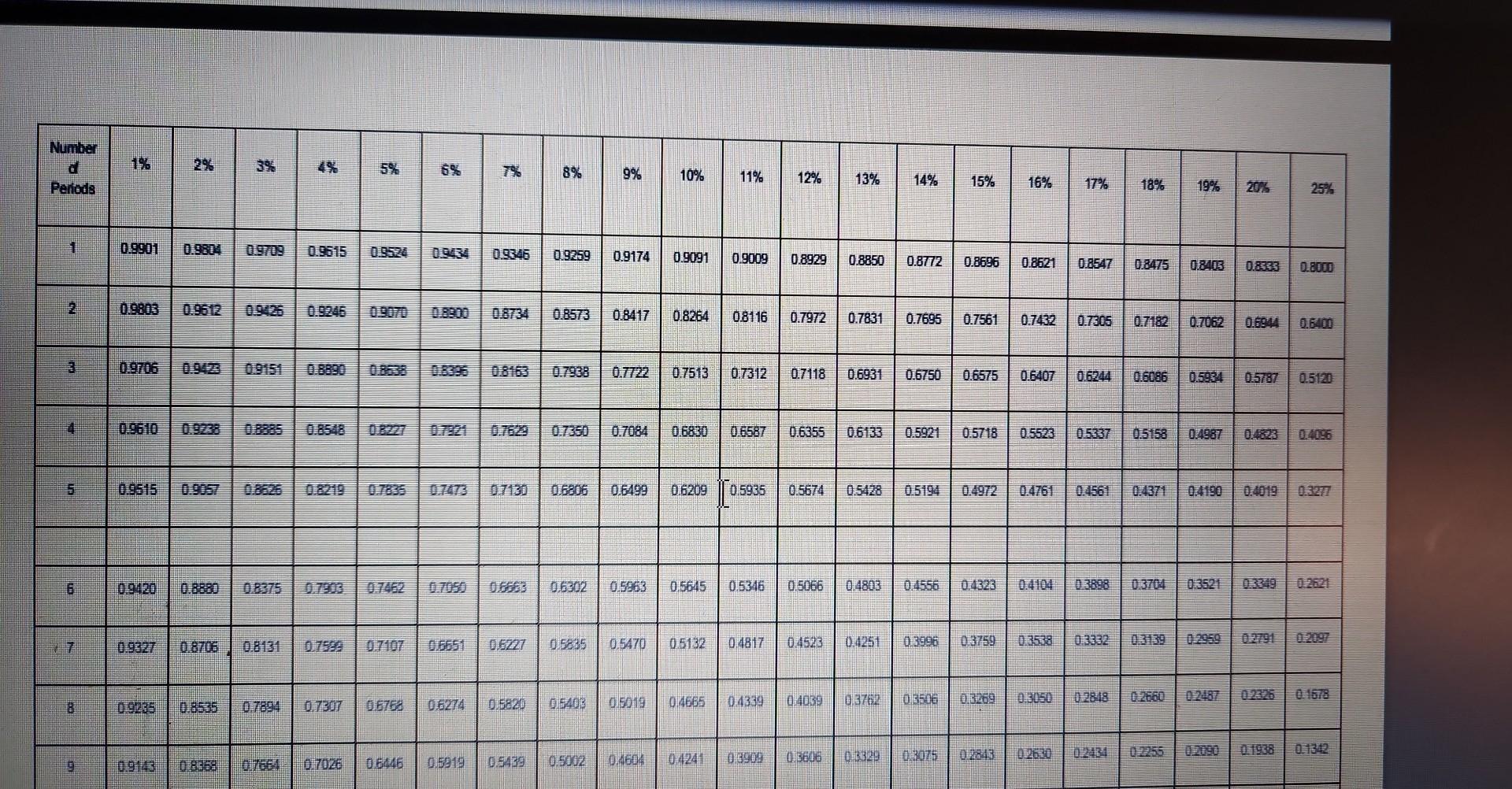

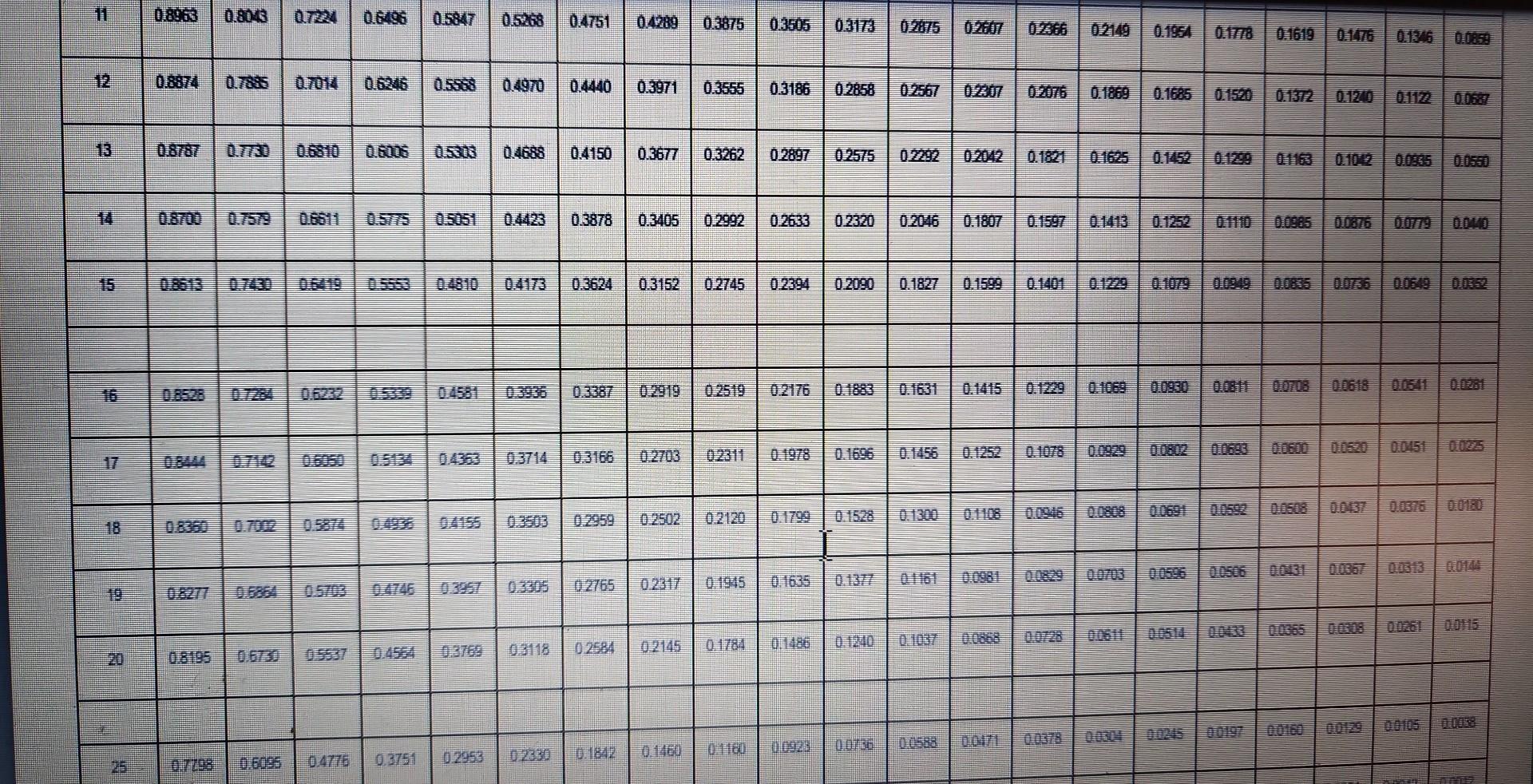

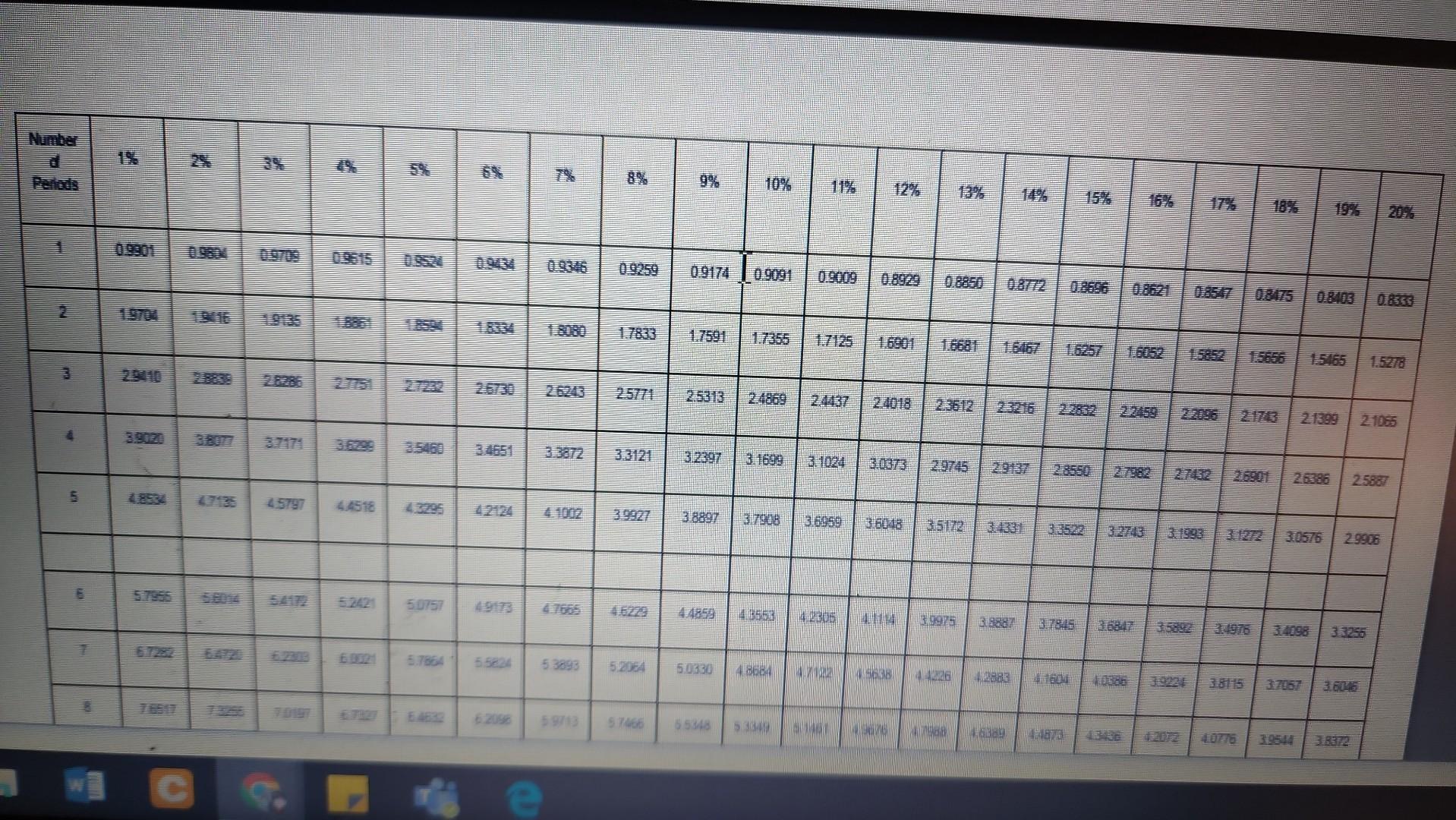

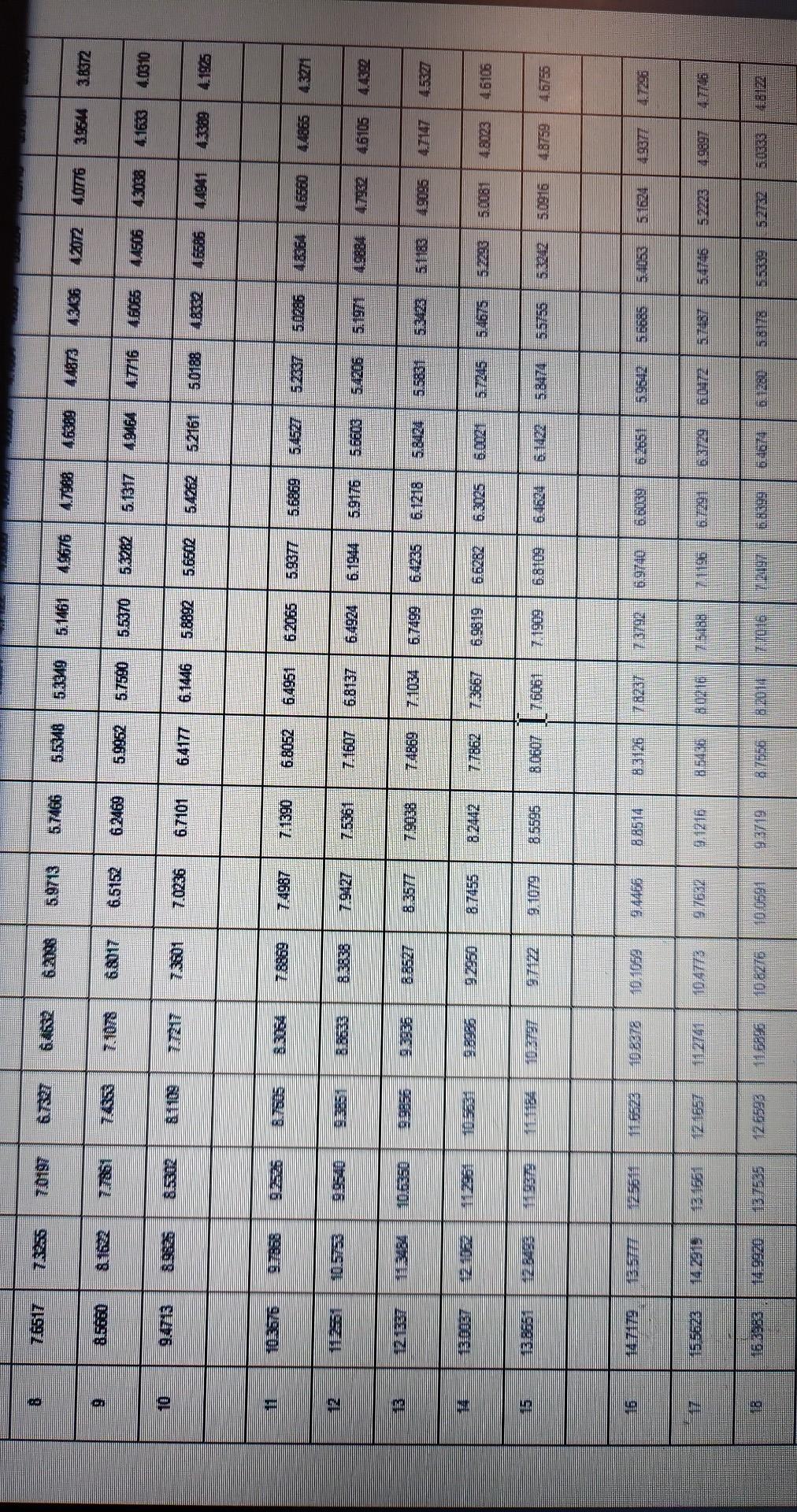

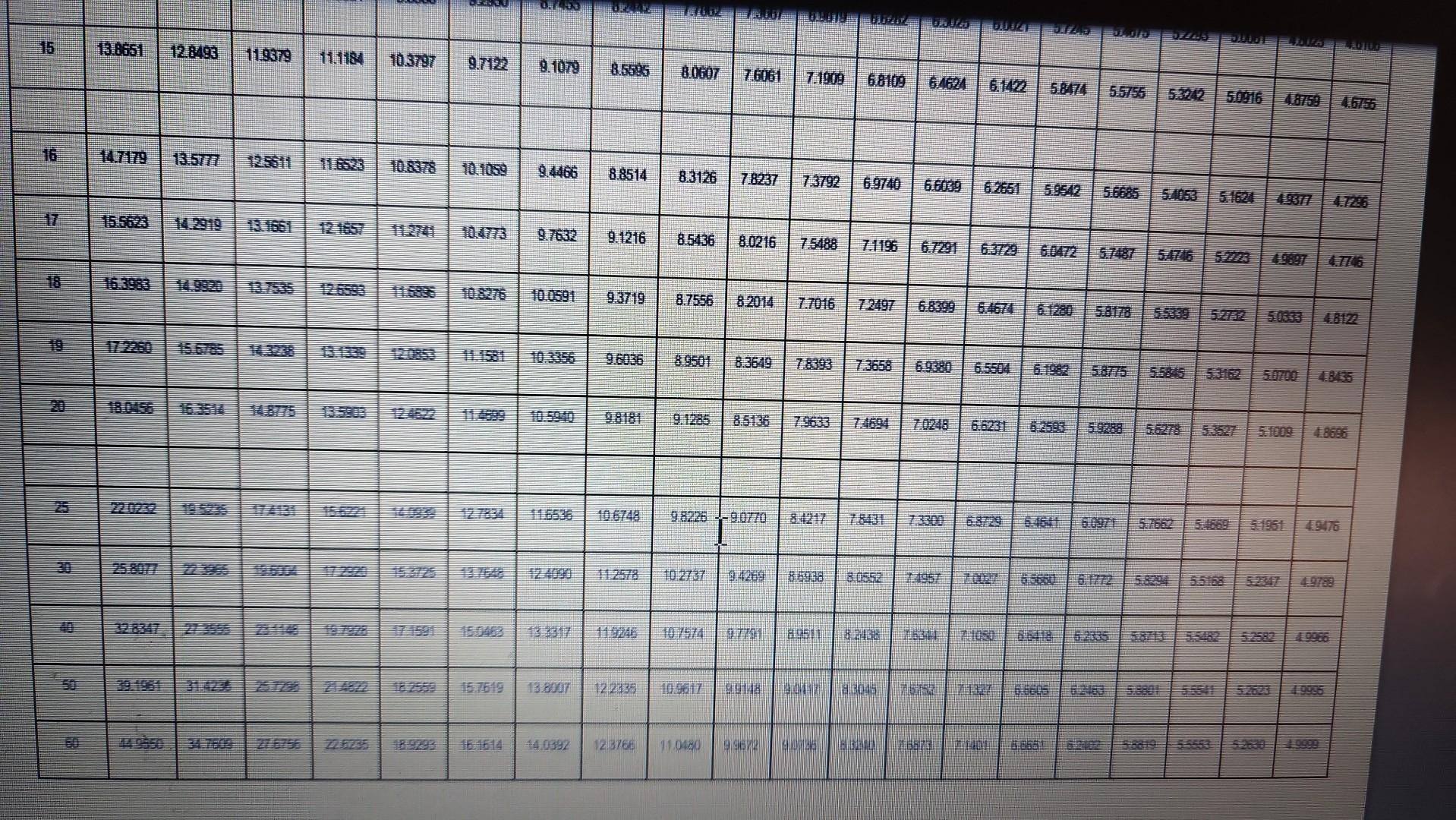

Question 1 Use the information provided to answer the questions. 1.1 1.2 Calculate the annual economic order quantity from the information provided below. INFORMATION GM Electronics expects to sell 800 alarm systems each month of 2022 at R4 000 each. The cost price of each alarm system is R2 000. The inventory holding cost of an alarm system is 1% of the unit cost price. The cost of placing an order for the alarm systems is estimated at R60. Study the information provided below and calculate the hourly recovery tariff per hour (expressed in rands and cents) of Martha. (4 marks) INFORMATION (4 marks) The basic annual salary of Martha is R576 000. She is entitled to an annual bonus of 90% of her basic monthly salary. Her employer contributes 8% of her basic salary to her pension fund. She works for 45 hours per week (from Monday to Friday). She is entitled to 21 days paid vacation leave. There are 12 public holidays in the year (365 days), 8 of which fall on weekdays. 1.3 1.4 1.5 Use the information provided below to calculate Samantha's remuneration for 17 March 2022. INFORMATION Samantha's normal wage is R300 per hour and her normal working day is 8 hours. The standard production time for each employee is 4 units for every 30 minutes. On 17 March 2022, Samantha's production was 76 units. Using the Halsey bonus system, a bonus of 50% of the time saved is given to employees. Calculate the earnings of G. Henry using the straight piecework incentive scheme from the information provided below. INFORMATION (4 marks) From the information provided below complete the table using the FIFO method of inventory valuation: (4 marks) I G. Henry is employed by Royal Manufacturers and is paid R250 per hour. His normal working day is 9 hours. The standard time to produce a product is 5 minutes. If G. Henry produces more than his quota, he receives 1 times the hourly rate on the additional output. G. Henry produced 132 units for the day. (4 marks) 1.5 From the information provided below complete the table using the FIFO method of inventory valuation: Purchased Date Quantity Price Amount Quantity Price Amount Date 01 The following transactions of Franco Manufacturers took place during March 2022: Issues and returns Transaction Opening inventory Units Quantity 1 600 Balance (4 marks) Price Amount Price per unit R3.50 The following transactions of Franco Manufacturers took place during March 2022: Date 01 05 12 24 16 28 Transaction Opening inventory Purchased from a supplier Purchased from a supplier Purchased from a supplier Issued to production Issued to production Units 1 600 600 1300 1 600 1 800 1 300 Price per unit R3.50 R4.00 R4.50 R5.00 INFORMATION The following information was extracted from the accounting records of Alpha Enterprises for the month ended 31 March 2022: Sales Selling price per unit Finished products on 01 March 2022 Products manufactured during the month Variable manufacturing costs per unit Variable selling and administrative costs per unit sold Fixed manufacturing costs A Fived selling and administrative costs 3 200 units R100 400 units 3 600 units R26 R12 R25 200 R12 100 Question 2 Answer the questions from the information provided. 2.1 Use the information given below to prepare the Income Statement for March 2022 according to the absorption costing method. 4 (12 marks) 2.2 Additional information 2.2.1 The variable manufacturing cost per unit and total manufacturing cost per unit of the finished goods on 01 March 2022 was R21.60 and R26.20 respectively. 2.2.2 2.2.3 2.2.4 Use the information provided below to calculate the following manufacturing variances for March 2022. Note: Each answer must state whether the variance is favourable or unfavourable. Labour rate variance Labour efficiency variance Variable overheads efficiency variance Variable overheads expenditure variance INFORMATION (2 marks) (2 marks) (2 marks) (2 marks) Nevada Limited set a standard labour rate of R32 per hour and a standard variable overhead rate of R3.80 per labour hour. Actual hours worked for March 2022 were 4 910 at a cost of R149 264. The actual variable overhead cost incurred was R19 640. The standard allowance of labour hours for the output achieved was 5 000 hours. Question 3 Study the information given below and answer each of the following questions independently: Calculate the total Marginal Income and Net Profit/Loss if all the tables are sold. 3.1 Use the marginal income ratio to calculate the break-even value. Calculate the new total Marginal Income and Net Profit/Loss, if an increase in advertising expense by R100 000 is expected to increase sales by 400 units. How many units must be sold if the company wishes to earn a net profit of R298 920. Based on the expected sales volume of 2 400 units, determine the sales price per unit (expressed in rands and cents) that will enable the company to break even. INFORMATION 3.2 3.3 3.4 3.5 (4 marks) (4 marks) (4 marks) 1. Total production and sales (4 marks) (4 marks) Samcor Limited manufactures tables. The following information was extracted from the budget for the year ended 30 June 2022: 2 400 units Samcor Limited manufactures tables. The following information was extracted from the budget for the year ended 30 June 2022: 1. 2. 3. 4. 5. Total production and sales Selling price per table Variable manufacturing costs per table: Direct material Direct labour Overheads Fixed manufacturing overheads Other costs: A Fixed marketing and administrative costs Sales commission 2 400 units R1 200 R288 R192 R96 R216 960 R144 000 5% 2. 3. 5. Selling price per table Variable manufacturing costs per table: Direct material Direct labour Overheads Fixed manufacturing overheads Other costs: A Fixed marketing and administrative costs Sales commission R1 200 R288 R192 R96 R216 960 R144 000 5% Question 4 Use the information provided below to prepare the following for January and February 2023: 4.1 Debtors Collection Schedule 4.2 Cash Budget INFORMATION The following information was provided by Intel Enterprises: 1. 2. 3. The bank balance on 31 December 2022 is expected to be R40 000 (unfavourable). Credit sales are expected to be as follows: lows: December 2022 R576 000 January 2023 R540 000 February 2023 R648 000 (4 marks) (16 marks) Credit sales usually make up 40% of the total sales. Cash sales make up the balance. Cash customers 3. 4. 5. Credit sales usually make up 40% of the total sales. Cash sales make up the balance. Cash customers- receive a 10% discount. Credit sales are normally collected as follows: * 30% in the month in which the transaction takes place, and these customers are entitled to a 5% discount. * 65% in the following month The rest is usually written off as bad debts. Budgeted purchases of inventory are as follows: December 2022 R1 000 000 A January 2023 R800 000 February 2023 R920 000 6. 7. 8. 9. 10. Fifty percent (50%) of the purchases are for cash. The remainder is paid in the month after the purchase. The monthly salaries amount to R150 000. Salaries are expected to increase by 9% with effect from 01 February 2023 for those employees who presently make up 80% of the salary bill. The salaries of the remaining 20% are expected to increase by 6%. Interest at 18% per annum on the loan balance is paid at the end of each month. The loan balance on 31 December 2022 was R400 000 and a capital repayment of R100 000 will be made on 01 February 2023. I Part of the building is sublet to a tenant and rent is collected monthly. The lease agreement for the year ended 31 January 2023 reflected the rental as R180 000 per annum. The rental will increase by 10% with effect from 01 February 2023. Other operating expenses are budgeted at R40 000 per month. This amount includes R5 000 for depreciation. Operating expenses are paid for in the month in which they are incurred. HI Question 5 Use the information provided to answer the questions. 5.1 Use the information provided below to calculate the following. Where applicable, use the present value tables provided in APPENDICES 1 and 2 that appear after QUESTION 5. Calculate the Payback Period of Project A (expressed in years, months and days). 5.1.1 5.1.2 Calculate the Accounting Rate of Return (on average investment) of Project B (expressed to two decimal places). I 5.1.3 Calculate the Net Present Value of each project (with amounts rounded off to the nearest Rand). 5.1.4 Use your answers from question 5.1.3 to recommend the project that should be chosen. Motivate your choice. (3 marks) (5 marks) (6 marks) (1 marks) INFORMATION Zeda Enterprises has the option to invest in machinery in projects A and B but finance is only available to invest in one of them. You are given the following projected data: Initial cost Scrap value Depreciation per year Net profit Year 1 Year 2 Year 3 Year 4 Project A R300 000 R40 000 R52 000 R20 000 R30 000 R50 000 R60 000 Project B R300 000 0 R60 000 Year 4 Year 5 Net cash flows Year 1 Year 2 Year 3 Year 4 Year 5 Additional information The discount rate used by the company is 12%. I R60 000 R10 000 R90 000 R90 000 R90 000 R90 000 R90 000 5.2 Additional information The discount rate used by the company is 12%. Use the information provided below to calculate the Internal Rate of Return (expressed to two decimal places) using interpolation. I INFORMATION (5 marks) A machine with a purchase price of R1 200 000 is estimated to eliminate manual operations by R400 000 per year. The machine is expected to have a useful life of four years. APPENDIX 1: PRESENT VALUE OF R1 Number 6 Periods 1 2 4 5 77 B 9 0.9901 0.9804 0.9803 0.9612 0.9706 0.9610 0.9515 0.9420 2% 09235 0.9143 0.9327 0.8706 0.8131 0.8880 0.8375 E 0.8535 0.8333 0.7894 0.9615 0.9524 0.7307 0.7026 0.9070 08998 0.7107 0.6768 0.6446 0.9346 8% 06274 0.5820 0.9259 0.5919 0.5439 0.8734 0.8573 0.8417 0.8264 0.6302 9% 0.6835 0.9174 0.5002 10% 0.7130 0,6806 0.6499 0.6209 0.5935 0.9091 0.5470 0.5403 05019 0.7722 0.7513 0.7312 0.4604 0.6830 0.5963 0.5645 0.5346 0.5132 0.9009 0.8929 04665 04241 0.6587 0.8116 0.7972 0.7831 0.7695 12% 13% 04817 0.4339 0.7118 0.8850 0.4523 0.5674 0.5428 0.4039 0.6133 0.6931 0.6750 14% 0.8772 0.5066 0.4803 0.4556 0.4251 0.3605 03329 0.5194 0.3996 0.3506 15% 16% 0.8696 0.8621 0.6575 0.5718 0.7561 0.7432 0.7305 0.7182 0.7062 0.2843 0.6407 0.6244 0.6086 0.4761 17% 0.5523 0.5337 0.5158 0.4104 0.3538 0.8547 0.8475 0.8403 03050 19% 0.4371 0.2660 0.4987 S 20% 0.3521 0.5934 10577877 0.5120 25% 0.8333 0.8000 0.4019 0.6400 0.1678 11 12 Z C o XXX 8 0.8963 0.8043 07344 0.6496 0.8874 0.7885 0.8195 0.6095 0.6246 0.6006 0.5847 0.5308 0.4776 0.3751 0.2953 0.4751 0.4289 0.3875 0.3505 0.3173 02875 0.4970 0.4440 0.3971 0.3555 0.3186 0.2858 0.2567 0.4688 0.4150 0.3118 0.3878 0.3405 0.2992 0.3624 0.3677 0.3262 02584 02765 0.2317 D. 1842 0.3152 0.2745 0.2120 02145 01784 01160 0.2176 0.2897 0.2575 0.2292 0.2042 0.1821 0.1625 0092 0.2633 0.2320 0.2046 0.1807 0.1597 0.2090 0.2307 2 0.2366 0.2149 0.1954 0.0585 0.2076 0.1869 0.1685 0.1252 0.1078 0.1229 0.1778 00506 0.1619 0.1372 0.1346 0.0440 00352 ATTE Number 1 - re - in LA 7 B 47135 45797 4456 621 50757 5.7864 5.5824 62098 25571 1.7591 39 2533 33121 =2397 3.1699 09091 5.3893 D2DB4 50330 59713 57466 55348 (38897 37908 36969 16048 32 5.149 A300 0.8929 4.7122 4114 45638 49076 25612 5 3.9975 1426 33887 B784 47988 14.6389 1601 4.4878 19 31272 19 08103 0.8333 3298 15165 2399 1.526 21065 25887 10576 2.9906 co 9 F S 7 S 103317 13.7636 7433 6593 B2098 5.9713. 57466 6.8017 97122 101059 10.4773 106270 65152 6.2469 7.0236 8.7455 9.7632 10:0531- 67101 6.4177 5.5348 7.4987 7.1390 6.8052 6.4951 85595 5.9952 9.1216 7.5361 7.1607 6.8137 7.1869 GVEES 8.0607 5.7590 5.5370 5.3282 5.1317 4.9464 6.1446 5.8892 5.6502 54262 7556 77862 7.3667 7.103 83514 832 7875 7,6061 5.1461 19676 4.7988 4.6389 4.4873 1336 42012 0776 39544 3.8372 20216 6-2065 6.7499 69819 1979 blo 77016 6.1944 5.9176 5.6603 6.4235 6.1218 6,8109 59377 5.6859 5.4527 523377 50286 3363 ppt 52161 63099 29 716 46065 44506 4038 4.1633 0310 50188 5.8399 6167 5.19711 5.8.24 55831 5.3423 4.6586 44941 4.3389 4.1925 5. 1183 199912 49095 3008- 4365m 43271 52 46105 4.53 5.0916 4.8759 4.6755 LO P 18 3 F S S 38651 28493 19379 1515623 525611 1184 103797 28785 10.8378 CERSAL 9.7122 0.7.33 9.1079 9.4466 8.8514 115 12.4090 9.1216 8.5595 B0607 7.6061 7.1909 6.8109 64624 518474 5.5755 9.3719 96036 98181 11.9246 14.0392 12.3766 8.5436 80216 7.5488 8.3126 7.8237 7.3792 6.9740 66039 6.2651 5999 56685 8.9501 8.3649 8.7556 8.2014 7.7016 72497 19.1285 8.136 7963 915226-90770 10.2737) 9.4269) 138007 12245 10.96177 11.0480 UJIFFE 03 (97791 (89511 7.1196 6.7291 8.0552 90736 7831 198 TERI (90417) 83045 VBAN Mossfer aloid 6.3729 THA 2 ( 2993 5418 57487 5242 50316 4.8759 465 588 56278 5182 0633 5.0700 1 2347 1286 4812 4.9476 Question 1 Use the information provided to answer the questions. 1.1 1.2 Calculate the annual economic order quantity from the information provided below. INFORMATION GM Electronics expects to sell 800 alarm systems each month of 2022 at R4 000 each. The cost price of each alarm system is R2 000. The inventory holding cost of an alarm system is 1% of the unit cost price. The cost of placing an order for the alarm systems is estimated at R60. Study the information provided below and calculate the hourly recovery tariff per hour (expressed in rands and cents) of Martha. (4 marks) INFORMATION (4 marks) The basic annual salary of Martha is R576 000. She is entitled to an annual bonus of 90% of her basic monthly salary. Her employer contributes 8% of her basic salary to her pension fund. She works for 45 hours per week (from Monday to Friday). She is entitled to 21 days paid vacation leave. There are 12 public holidays in the year (365 days), 8 of which fall on weekdays. 1.3 1.4 1.5 Use the information provided below to calculate Samantha's remuneration for 17 March 2022. INFORMATION Samantha's normal wage is R300 per hour and her normal working day is 8 hours. The standard production time for each employee is 4 units for every 30 minutes. On 17 March 2022, Samantha's production was 76 units. Using the Halsey bonus system, a bonus of 50% of the time saved is given to employees. Calculate the earnings of G. Henry using the straight piecework incentive scheme from the information provided below. INFORMATION (4 marks) From the information provided below complete the table using the FIFO method of inventory valuation: (4 marks) I G. Henry is employed by Royal Manufacturers and is paid R250 per hour. His normal working day is 9 hours. The standard time to produce a product is 5 minutes. If G. Henry produces more than his quota, he receives 1 times the hourly rate on the additional output. G. Henry produced 132 units for the day. (4 marks) 1.5 From the information provided below complete the table using the FIFO method of inventory valuation: Purchased Date Quantity Price Amount Quantity Price Amount Date 01 The following transactions of Franco Manufacturers took place during March 2022: Issues and returns Transaction Opening inventory Units Quantity 1 600 Balance (4 marks) Price Amount Price per unit R3.50 The following transactions of Franco Manufacturers took place during March 2022: Date 01 05 12 24 16 28 Transaction Opening inventory Purchased from a supplier Purchased from a supplier Purchased from a supplier Issued to production Issued to production Units 1 600 600 1300 1 600 1 800 1 300 Price per unit R3.50 R4.00 R4.50 R5.00 INFORMATION The following information was extracted from the accounting records of Alpha Enterprises for the month ended 31 March 2022: Sales Selling price per unit Finished products on 01 March 2022 Products manufactured during the month Variable manufacturing costs per unit Variable selling and administrative costs per unit sold Fixed manufacturing costs A Fived selling and administrative costs 3 200 units R100 400 units 3 600 units R26 R12 R25 200 R12 100 Question 2 Answer the questions from the information provided. 2.1 Use the information given below to prepare the Income Statement for March 2022 according to the absorption costing method. 4 (12 marks) 2.2 Additional information 2.2.1 The variable manufacturing cost per unit and total manufacturing cost per unit of the finished goods on 01 March 2022 was R21.60 and R26.20 respectively. 2.2.2 2.2.3 2.2.4 Use the information provided below to calculate the following manufacturing variances for March 2022. Note: Each answer must state whether the variance is favourable or unfavourable. Labour rate variance Labour efficiency variance Variable overheads efficiency variance Variable overheads expenditure variance INFORMATION (2 marks) (2 marks) (2 marks) (2 marks) Nevada Limited set a standard labour rate of R32 per hour and a standard variable overhead rate of R3.80 per labour hour. Actual hours worked for March 2022 were 4 910 at a cost of R149 264. The actual variable overhead cost incurred was R19 640. The standard allowance of labour hours for the output achieved was 5 000 hours. Question 3 Study the information given below and answer each of the following questions independently: Calculate the total Marginal Income and Net Profit/Loss if all the tables are sold. 3.1 Use the marginal income ratio to calculate the break-even value. Calculate the new total Marginal Income and Net Profit/Loss, if an increase in advertising expense by R100 000 is expected to increase sales by 400 units. How many units must be sold if the company wishes to earn a net profit of R298 920. Based on the expected sales volume of 2 400 units, determine the sales price per unit (expressed in rands and cents) that will enable the company to break even. INFORMATION 3.2 3.3 3.4 3.5 (4 marks) (4 marks) (4 marks) 1. Total production and sales (4 marks) (4 marks) Samcor Limited manufactures tables. The following information was extracted from the budget for the year ended 30 June 2022: 2 400 units Samcor Limited manufactures tables. The following information was extracted from the budget for the year ended 30 June 2022: 1. 2. 3. 4. 5. Total production and sales Selling price per table Variable manufacturing costs per table: Direct material Direct labour Overheads Fixed manufacturing overheads Other costs: A Fixed marketing and administrative costs Sales commission 2 400 units R1 200 R288 R192 R96 R216 960 R144 000 5% 2. 3. 5. Selling price per table Variable manufacturing costs per table: Direct material Direct labour Overheads Fixed manufacturing overheads Other costs: A Fixed marketing and administrative costs Sales commission R1 200 R288 R192 R96 R216 960 R144 000 5% Question 4 Use the information provided below to prepare the following for January and February 2023: 4.1 Debtors Collection Schedule 4.2 Cash Budget INFORMATION The following information was provided by Intel Enterprises: 1. 2. 3. The bank balance on 31 December 2022 is expected to be R40 000 (unfavourable). Credit sales are expected to be as follows: lows: December 2022 R576 000 January 2023 R540 000 February 2023 R648 000 (4 marks) (16 marks) Credit sales usually make up 40% of the total sales. Cash sales make up the balance. Cash customers 3. 4. 5. Credit sales usually make up 40% of the total sales. Cash sales make up the balance. Cash customers- receive a 10% discount. Credit sales are normally collected as follows: * 30% in the month in which the transaction takes place, and these customers are entitled to a 5% discount. * 65% in the following month The rest is usually written off as bad debts. Budgeted purchases of inventory are as follows: December 2022 R1 000 000 A January 2023 R800 000 February 2023 R920 000 6. 7. 8. 9. 10. Fifty percent (50%) of the purchases are for cash. The remainder is paid in the month after the purchase. The monthly salaries amount to R150 000. Salaries are expected to increase by 9% with effect from 01 February 2023 for those employees who presently make up 80% of the salary bill. The salaries of the remaining 20% are expected to increase by 6%. Interest at 18% per annum on the loan balance is paid at the end of each month. The loan balance on 31 December 2022 was R400 000 and a capital repayment of R100 000 will be made on 01 February 2023. I Part of the building is sublet to a tenant and rent is collected monthly. The lease agreement for the year ended 31 January 2023 reflected the rental as R180 000 per annum. The rental will increase by 10% with effect from 01 February 2023. Other operating expenses are budgeted at R40 000 per month. This amount includes R5 000 for depreciation. Operating expenses are paid for in the month in which they are incurred. HI Question 5 Use the information provided to answer the questions. 5.1 Use the information provided below to calculate the following. Where applicable, use the present value tables provided in APPENDICES 1 and 2 that appear after QUESTION 5. Calculate the Payback Period of Project A (expressed in years, months and days). 5.1.1 5.1.2 Calculate the Accounting Rate of Return (on average investment) of Project B (expressed to two decimal places). I 5.1.3 Calculate the Net Present Value of each project (with amounts rounded off to the nearest Rand). 5.1.4 Use your answers from question 5.1.3 to recommend the project that should be chosen. Motivate your choice. (3 marks) (5 marks) (6 marks) (1 marks) INFORMATION Zeda Enterprises has the option to invest in machinery in projects A and B but finance is only available to invest in one of them. You are given the following projected data: Initial cost Scrap value Depreciation per year Net profit Year 1 Year 2 Year 3 Year 4 Project A R300 000 R40 000 R52 000 R20 000 R30 000 R50 000 R60 000 Project B R300 000 0 R60 000 Year 4 Year 5 Net cash flows Year 1 Year 2 Year 3 Year 4 Year 5 Additional information The discount rate used by the company is 12%. I R60 000 R10 000 R90 000 R90 000 R90 000 R90 000 R90 000 5.2 Additional information The discount rate used by the company is 12%. Use the information provided below to calculate the Internal Rate of Return (expressed to two decimal places) using interpolation. I INFORMATION (5 marks) A machine with a purchase price of R1 200 000 is estimated to eliminate manual operations by R400 000 per year. The machine is expected to have a useful life of four years. APPENDIX 1: PRESENT VALUE OF R1 Number 6 Periods 1 2 4 5 77 B 9 0.9901 0.9804 0.9803 0.9612 0.9706 0.9610 0.9515 0.9420 2% 09235 0.9143 0.9327 0.8706 0.8131 0.8880 0.8375 E 0.8535 0.8333 0.7894 0.9615 0.9524 0.7307 0.7026 0.9070 08998 0.7107 0.6768 0.6446 0.9346 8% 06274 0.5820 0.9259 0.5919 0.5439 0.8734 0.8573 0.8417 0.8264 0.6302 9% 0.6835 0.9174 0.5002 10% 0.7130 0,6806 0.6499 0.6209 0.5935 0.9091 0.5470 0.5403 05019 0.7722 0.7513 0.7312 0.4604 0.6830 0.5963 0.5645 0.5346 0.5132 0.9009 0.8929 04665 04241 0.6587 0.8116 0.7972 0.7831 0.7695 12% 13% 04817 0.4339 0.7118 0.8850 0.4523 0.5674 0.5428 0.4039 0.6133 0.6931 0.6750 14% 0.8772 0.5066 0.4803 0.4556 0.4251 0.3605 03329 0.5194 0.3996 0.3506 15% 16% 0.8696 0.8621 0.6575 0.5718 0.7561 0.7432 0.7305 0.7182 0.7062 0.2843 0.6407 0.6244 0.6086 0.4761 17% 0.5523 0.5337 0.5158 0.4104 0.3538 0.8547 0.8475 0.8403 03050 19% 0.4371 0.2660 0.4987 S 20% 0.3521 0.5934 10577877 0.5120 25% 0.8333 0.8000 0.4019 0.6400 0.1678 11 12 Z C o XXX 8 0.8963 0.8043 07344 0.6496 0.8874 0.7885 0.8195 0.6095 0.6246 0.6006 0.5847 0.5308 0.4776 0.3751 0.2953 0.4751 0.4289 0.3875 0.3505 0.3173 02875 0.4970 0.4440 0.3971 0.3555 0.3186 0.2858 0.2567 0.4688 0.4150 0.3118 0.3878 0.3405 0.2992 0.3624 0.3677 0.3262 02584 02765 0.2317 D. 1842 0.3152 0.2745 0.2120 02145 01784 01160 0.2176 0.2897 0.2575 0.2292 0.2042 0.1821 0.1625 0092 0.2633 0.2320 0.2046 0.1807 0.1597 0.2090 0.2307 2 0.2366 0.2149 0.1954 0.0585 0.2076 0.1869 0.1685 0.1252 0.1078 0.1229 0.1778 00506 0.1619 0.1372 0.1346 0.0440 00352 ATTE Number 1 - re - in LA 7 B 47135 45797 4456 621 50757 5.7864 5.5824 62098 25571 1.7591 39 2533 33121 =2397 3.1699 09091 5.3893 D2DB4 50330 59713 57466 55348 (38897 37908 36969 16048 32 5.149 A300 0.8929 4.7122 4114 45638 49076 25612 5 3.9975 1426 33887 B784 47988 14.6389 1601 4.4878 19 31272 19 08103 0.8333 3298 15165 2399 1.526 21065 25887 10576 2.9906 co 9 F S 7 S 103317 13.7636 7433 6593 B2098 5.9713. 57466 6.8017 97122 101059 10.4773 106270 65152 6.2469 7.0236 8.7455 9.7632 10:0531- 67101 6.4177 5.5348 7.4987 7.1390 6.8052 6.4951 85595 5.9952 9.1216 7.5361 7.1607 6.8137 7.1869 GVEES 8.0607 5.7590 5.5370 5.3282 5.1317 4.9464 6.1446 5.8892 5.6502 54262 7556 77862 7.3667 7.103 83514 832 7875 7,6061 5.1461 19676 4.7988 4.6389 4.4873 1336 42012 0776 39544 3.8372 20216 6-2065 6.7499 69819 1979 blo 77016 6.1944 5.9176 5.6603 6.4235 6.1218 6,8109 59377 5.6859 5.4527 523377 50286 3363 ppt 52161 63099 29 716 46065 44506 4038 4.1633 0310 50188 5.8399 6167 5.19711 5.8.24 55831 5.3423 4.6586 44941 4.3389 4.1925 5. 1183 199912 49095 3008- 4365m 43271 52 46105 4.53 5.0916 4.8759 4.6755 LO P 18 3 F S S 38651 28493 19379 1515623 525611 1184 103797 28785 10.8378 CERSAL 9.7122 0.7.33 9.1079 9.4466 8.8514 115 12.4090 9.1216 8.5595 B0607 7.6061 7.1909 6.8109 64624 518474 5.5755 9.3719 96036 98181 11.9246 14.0392 12.3766 8.5436 80216 7.5488 8.3126 7.8237 7.3792 6.9740 66039 6.2651 5999 56685 8.9501 8.3649 8.7556 8.2014 7.7016 72497 19.1285 8.136 7963 915226-90770 10.2737) 9.4269) 138007 12245 10.96177 11.0480 UJIFFE 03 (97791 (89511 7.1196 6.7291 8.0552 90736 7831 198 TERI (90417) 83045 VBAN Mossfer aloid 6.3729 THA 2 ( 2993 5418 57487 5242 50316 4.8759 465 588 56278 5182 0633 5.0700 1 2347 1286 4812 4.9476

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts