Question (1) What inferences may you make from an initial analytical review of financial statements? O...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

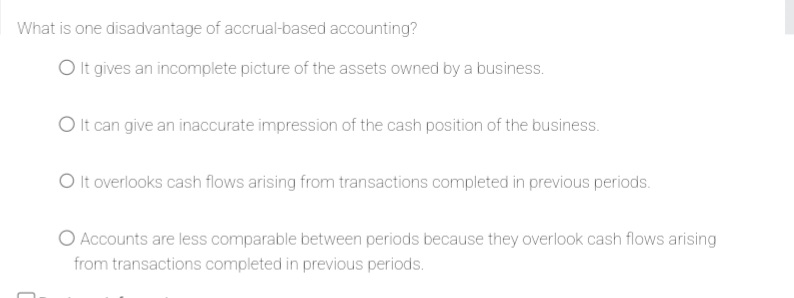

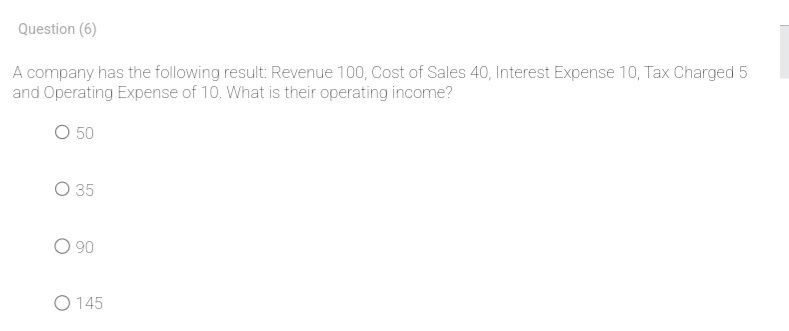

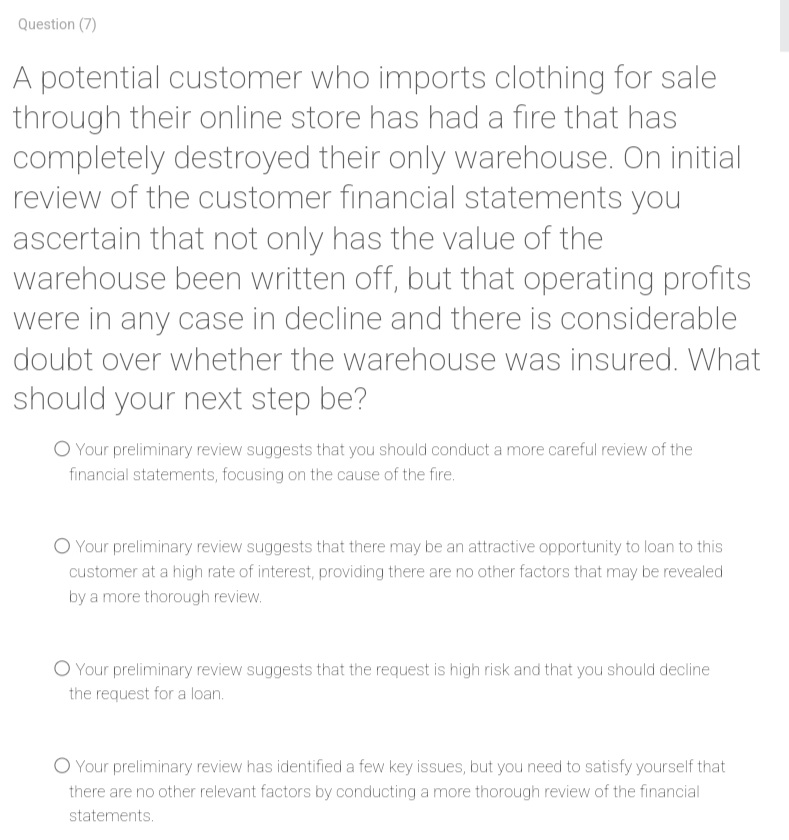

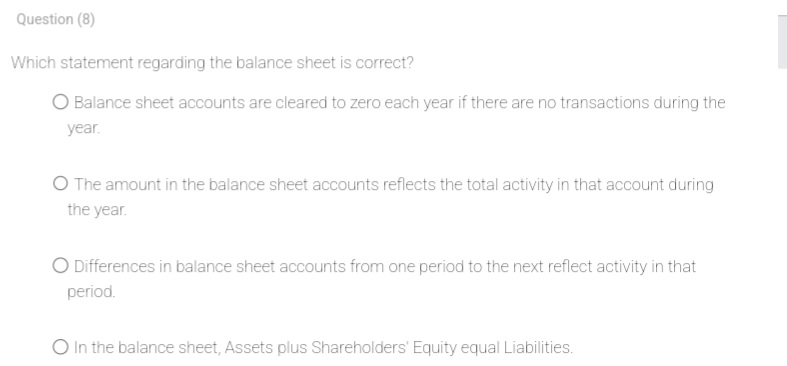

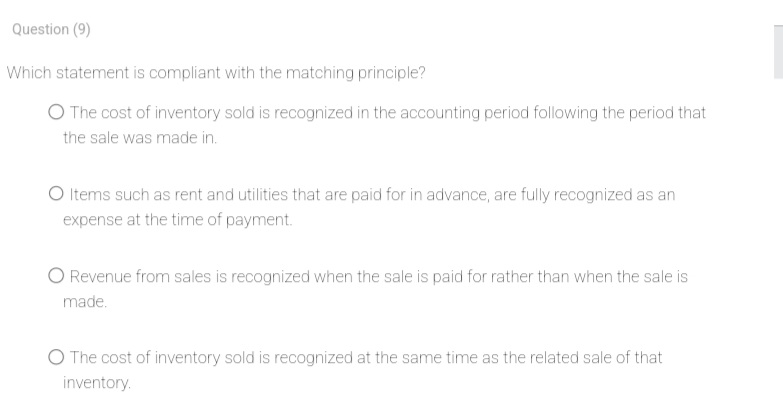

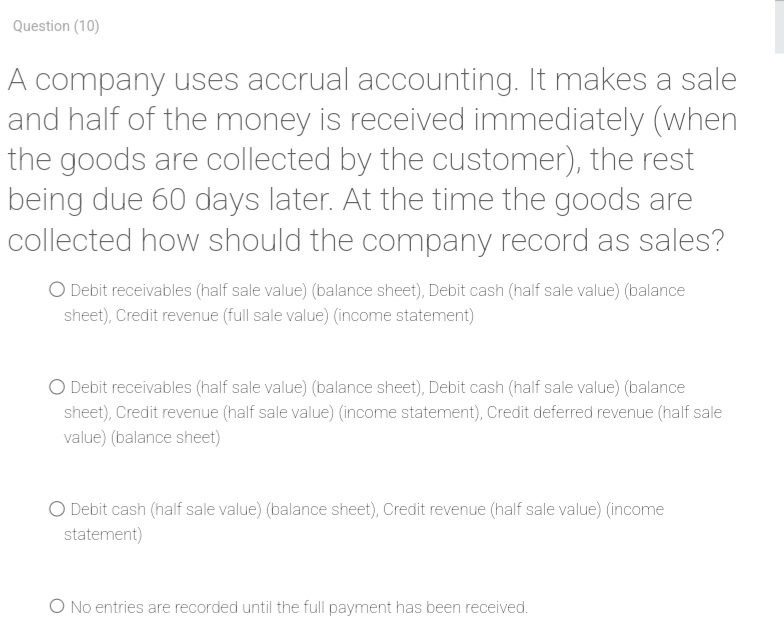

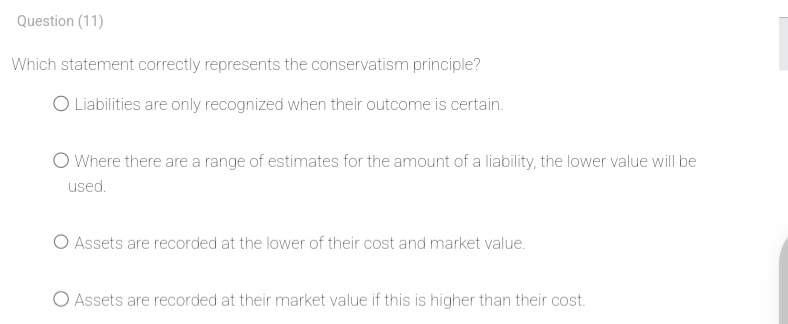

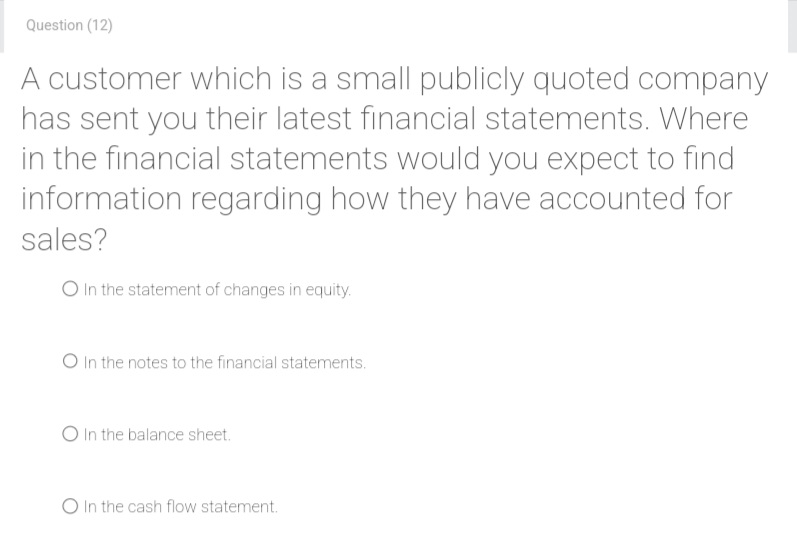

Question (1) What inferences may you make from an initial analytical review of financial statements? O Whether the business has performed at a satisfactory level during the period. O Whether all costs have been recognized in the correct accounting period. O Whether management may be involved in fraudulent activities. O Whether the business has hidden liabilities at the year end. Question (2) What are the five accounting blocks? O Asset accounts, Expense accounts, Liability accounts, Equity accounts (or net worth accounts), Revenue accounts O Asset accounts, Expense accounts, Liability accounts, Net cash flow, Revenue accounts O Asset accounts, Net cash flow, Deferral accounts, Liability accounts, Equity accounts (or net worth accounts) O Asset accounts, Expense accounts, Liability accounts, Deferral accounts, Revenue accounts Question (3) Why do credit institutions use accrual accounts to support lending decisions? O Because banks do not find information about past cash flows useful. O Because, most companies prepare financial statements using accrual accounting. O Because banking regulations require them to do so. O Because most companies are unable to provide information relating to cash flows. Question (4) You have been asked to examine the risk drivers in a client's financial statements. Which numbers in the statements should you pay attention to? O Depreciation. O Gains on disposal of assets. Sales growth. O Interest expense. What is one disadvantage of accrual-based accounting? O It gives an incomplete picture of the assets owned by a business. O It can give an inaccurate impression of the cash position of the business. O It overlooks cash flows arising from transactions completed in previous periods. O Accounts are less comparable between periods because they overlook cash flows arising from transactions completed in previous periods. Question (6) A company has the following result: Revenue 100, Cost of Sales 40, Interest Expense 10, Tax Charged 5 and Operating Expense of 10. What is their operating income? O 50 O 35 90 O 145 Question (7) A potential customer who imports clothing for sale through their online store has had a fire that has completely destroyed their only warehouse. On initial review of the customer financial statements you ascertain that not only has the value of the warehouse been written off, but that operating profits were in any case in decline and there is considerable doubt over whether the warehouse was insured. What should your next step be? O Your preliminary review suggests that you should conduct a more careful review of the financial statements, focusing on the cause of the fire. O Your preliminary review suggests that there may be an attractive opportunity to loan to this customer at a high rate of interest, providing there are no other factors that may be revealed by a more thorough review. O Your preliminary review suggests that the request is high risk and that you should decline the request for a loan. O Your preliminary review has identified a few key issues, but you need to satisfy yourself that there are no other relevant factors by conducting a more thorough review of the financial statements. Question (8) Which statement regarding the balance sheet is correct? O Balance sheet accounts are cleared to zero each year if there are no transactions during the year. O The amount in the balance sheet accounts reflects the total activity in that account during the year. O Differences in balance sheet accounts from one period to the next reflect activity in that period. O In the balance sheet, Assets plus Shareholders' Equity equal Liabilities. Question (9) Which statement is compliant with the matching principle? The cost of inventory sold is recognized in the accounting period following the period that the sale was made in. O Items such as rent and utilities that are paid for in advance, are fully recognized as an expense at the time of payment. Revenue from sales is recognized when the sale is paid for rather than when the sale is made. O The cost of inventory sold is recognized at the same time as the related sale of that inventory. Question (10) A company uses accrual accounting. It makes a sale and half of the money is received immediately (when the goods are collected by the customer), the rest being due 60 days later. At the time the goods are collected how should the company record as sales? O Debit receivables (half sale value) (balance sheet), Debit cash (half sale value) (balance sheet), Credit revenue (full sale value) (income statement) O Debit receivables (half sale value) (balance sheet), Debit cash (half sale value) (balance sheet), Credit revenue (half sale value) (income statement), Credit deferred revenue (half sale value) (balance sheet) O Debit cash (half sale value) (balance sheet), Credit revenue (half sale value) (income statement) O No entries are recorded until the full payment has been received. Question (11) Which statement correctly represents the conservatism principle? O Liabilities are only recognized when their outcome is certain. O Where there are a range of estimates for the amount of a liability, the lower value will be used. O Assets are recorded at the lower of their cost and market value. O Assets are recorded at their market value if this is higher than their cost. Question (12) A customer which is a small publicly quoted company has sent you their latest financial statements. Where in the financial statements would you expect to find information regarding how they have accounted for sales? O In the statement of changes in equity. O In the notes to the financial statements. O In the balance sheet. O In the cash flow statement. Question (13) Which statement best describes a key benefit of inferring analytical results from an initial review of a company's financial statements? O It helps you to understand whether the accounts have been correctly prepared. O It allows you to screen out high-risk loan applications at a relatively early stage in the process. O It saves time by reducing the amount of interaction required with borrowers. O It allows you to make a lending decision as long as no significant risks are noted. Question (14) When reviewing the financial statements of smaller businesses that have been prepared under the accrual basis, which statement may sometimes be missing? Balance sheet. Cash flow statement. O Profit and loss account. O Basis of accounting. Question (15) A company receives inventory on 15 April and pays for it in part by cash, with the balance payable 30 days later. What is recorded in the accounts on 15 April under the accrual method? O Cash elements only O The cash amount is recorded as an expense, with the balance recorded as a payable. O Both the cash and non-cash component O Nothing until the full amount is paid Question (16) Which statement is true regarding double-entry accounting? O The difference between debit and credit entries in the accounts equals profit or loss. O There will always be the same number of debit and credit entries. O The value of debit and credit entries for each financial transactions will not always be equal. O The total value of debit entries must equal the total value of credit entries Question (1) What inferences may you make from an initial analytical review of financial statements? O Whether the business has performed at a satisfactory level during the period. O Whether all costs have been recognized in the correct accounting period. O Whether management may be involved in fraudulent activities. O Whether the business has hidden liabilities at the year end. Question (2) What are the five accounting blocks? O Asset accounts, Expense accounts, Liability accounts, Equity accounts (or net worth accounts), Revenue accounts O Asset accounts, Expense accounts, Liability accounts, Net cash flow, Revenue accounts O Asset accounts, Net cash flow, Deferral accounts, Liability accounts, Equity accounts (or net worth accounts) O Asset accounts, Expense accounts, Liability accounts, Deferral accounts, Revenue accounts Question (3) Why do credit institutions use accrual accounts to support lending decisions? O Because banks do not find information about past cash flows useful. O Because, most companies prepare financial statements using accrual accounting. O Because banking regulations require them to do so. O Because most companies are unable to provide information relating to cash flows. Question (4) You have been asked to examine the risk drivers in a client's financial statements. Which numbers in the statements should you pay attention to? O Depreciation. O Gains on disposal of assets. Sales growth. O Interest expense. What is one disadvantage of accrual-based accounting? O It gives an incomplete picture of the assets owned by a business. O It can give an inaccurate impression of the cash position of the business. O It overlooks cash flows arising from transactions completed in previous periods. O Accounts are less comparable between periods because they overlook cash flows arising from transactions completed in previous periods. Question (6) A company has the following result: Revenue 100, Cost of Sales 40, Interest Expense 10, Tax Charged 5 and Operating Expense of 10. What is their operating income? O 50 O 35 90 O 145 Question (7) A potential customer who imports clothing for sale through their online store has had a fire that has completely destroyed their only warehouse. On initial review of the customer financial statements you ascertain that not only has the value of the warehouse been written off, but that operating profits were in any case in decline and there is considerable doubt over whether the warehouse was insured. What should your next step be? O Your preliminary review suggests that you should conduct a more careful review of the financial statements, focusing on the cause of the fire. O Your preliminary review suggests that there may be an attractive opportunity to loan to this customer at a high rate of interest, providing there are no other factors that may be revealed by a more thorough review. O Your preliminary review suggests that the request is high risk and that you should decline the request for a loan. O Your preliminary review has identified a few key issues, but you need to satisfy yourself that there are no other relevant factors by conducting a more thorough review of the financial statements. Question (8) Which statement regarding the balance sheet is correct? O Balance sheet accounts are cleared to zero each year if there are no transactions during the year. O The amount in the balance sheet accounts reflects the total activity in that account during the year. O Differences in balance sheet accounts from one period to the next reflect activity in that period. O In the balance sheet, Assets plus Shareholders' Equity equal Liabilities. Question (9) Which statement is compliant with the matching principle? The cost of inventory sold is recognized in the accounting period following the period that the sale was made in. O Items such as rent and utilities that are paid for in advance, are fully recognized as an expense at the time of payment. Revenue from sales is recognized when the sale is paid for rather than when the sale is made. O The cost of inventory sold is recognized at the same time as the related sale of that inventory. Question (10) A company uses accrual accounting. It makes a sale and half of the money is received immediately (when the goods are collected by the customer), the rest being due 60 days later. At the time the goods are collected how should the company record as sales? O Debit receivables (half sale value) (balance sheet), Debit cash (half sale value) (balance sheet), Credit revenue (full sale value) (income statement) O Debit receivables (half sale value) (balance sheet), Debit cash (half sale value) (balance sheet), Credit revenue (half sale value) (income statement), Credit deferred revenue (half sale value) (balance sheet) O Debit cash (half sale value) (balance sheet), Credit revenue (half sale value) (income statement) O No entries are recorded until the full payment has been received. Question (11) Which statement correctly represents the conservatism principle? O Liabilities are only recognized when their outcome is certain. O Where there are a range of estimates for the amount of a liability, the lower value will be used. O Assets are recorded at the lower of their cost and market value. O Assets are recorded at their market value if this is higher than their cost. Question (12) A customer which is a small publicly quoted company has sent you their latest financial statements. Where in the financial statements would you expect to find information regarding how they have accounted for sales? O In the statement of changes in equity. O In the notes to the financial statements. O In the balance sheet. O In the cash flow statement. Question (13) Which statement best describes a key benefit of inferring analytical results from an initial review of a company's financial statements? O It helps you to understand whether the accounts have been correctly prepared. O It allows you to screen out high-risk loan applications at a relatively early stage in the process. O It saves time by reducing the amount of interaction required with borrowers. O It allows you to make a lending decision as long as no significant risks are noted. Question (14) When reviewing the financial statements of smaller businesses that have been prepared under the accrual basis, which statement may sometimes be missing? Balance sheet. Cash flow statement. O Profit and loss account. O Basis of accounting. Question (15) A company receives inventory on 15 April and pays for it in part by cash, with the balance payable 30 days later. What is recorded in the accounts on 15 April under the accrual method? O Cash elements only O The cash amount is recorded as an expense, with the balance recorded as a payable. O Both the cash and non-cash component O Nothing until the full amount is paid Question (16) Which statement is true regarding double-entry accounting? O The difference between debit and credit entries in the accounts equals profit or loss. O There will always be the same number of debit and credit entries. O The value of debit and credit entries for each financial transactions will not always be equal. O The total value of debit entries must equal the total value of credit entries

Expert Answer:

Related Book For

Auditing A Practical Approach

ISBN: 9780730382645

4th Edition

Authors: Robyn Moroney, Fiona Campbell, Jane Hamilton

Posted Date:

Students also viewed these accounting questions

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

Planning is one of the most important management functions in any business. A front office managers first step in planning should involve determine the departments goals. Planning also includes...

-

How important it is to educate ourselves environmental issues impacting the future of tourism i.e., climate change The COVID-19 pandemic has changed the tourism industry forever and will impact our...

-

Nanette is a first-grade teacher. Potential deductions are charitable contributions of $800, personal property taxes on her car of $240, and various supplies purchased for use in her classroom of...

-

The Tollhouse Equipment Company manufactures lathes, routers, saws, and other woodworking equipment. The companys controller imported its weekly manufacturing data from the past year into Excel. The...

-

Crush Autosmashers can purchase a new electromagnet for moving cars at a cost of \($20,000.\) At the end of its useful life, the electromagnet will be worth \($1,000.\) If Crushs MARR is 12...

-

In recent years, Farr Company has purchased three machines. Because of frequent employee turnover in the accounting department, a different accountant was in charge of selecting the depreciation...

-

5. WORK HEALTH & SAFETY Provide at least three types of hazards, corresponding risks, rating and control measures. Risk Rating (Low/Medium/High) Control measures (Current/Required)

-

(a) For the circuit in Fig. 4.138, obtain the Thevenin equivalent at terminals a-b. (b) Calculate the current in RL = 8(. (c) Find RL for maximum power deliverable to RL. (d) Determine that maximum...

-

The manager of the customer service department of a software company is concerned about the number of errors committed in the software development process. A random sample of 250 coding was inspected...

-

(a) State exactly what property the string input by the user must have for the program below to print "Yes..." Explain the program logic concisely but clearly (i.e. give the key steps). (2 marks) int...

-

1. In your own words, kindly explain the Audit Trail, its importance in AIS and give an example of a complete audit trail in your personal life setting. 2. What are the types of files in a system and...

-

What happens to the difference between the billed amount and the allowed amount unless it can be billed to the patient under the payer's rules?

-

identify which are media and which are information assets: Traverse Accounting Software provides the following applications: General Ledger Accounts Payable Accounts Receivable Payroll (Employee...

-

What tax is both withheld from an employee's pay and matched by the employer?

-

Why is limiting reagent important? Give all of its purpose

-

Keating & Partners is a law firm specializing in labour relations and employee-related work. It employs 25 professionals (5 partners and 20 managers) who work directly with its clients. The average...

-

Onyx Operating Ltd has experienced sustained growth in recent years under the leadership of the last two CEOs, both of whom were promoted from within the business. The company began by making steel,...

-

Reliable Paper Ltd provides cardboard, paper and plastic packaging materials to a large number of manufacturers and distributors in all states. The cardboard and paper division is a well-established...

-

In preparation to test other items on the income statement, Rory reminds Leigh to remember her introductory accounting. An account balance is the result of the transactions that have been posted to...

-

Economy Appliance Co. manufactures lowprice, no-frills appliances that are in great demand for rental units. Pricing and cost information on Economys main products are as shown on page 943. Customers...

-

Grill Master Company sells total outdoor grilling solutions, providing gas and charcoal grills, accessories, and installation services for custom patio grilling stations. Instructions Respond to the...

-

Tablet Tailors sells tablet PCs combined with Internet service (Tablet Bundle A) that permits the tablet to connect to the Internet anywhere (set up a Wi-Fi hot spot). The price for the tablet and a...

Study smarter with the SolutionInn App