Question 3 (17 marks) Steven is a financial planner at Morgan Investment Bank. He has just...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

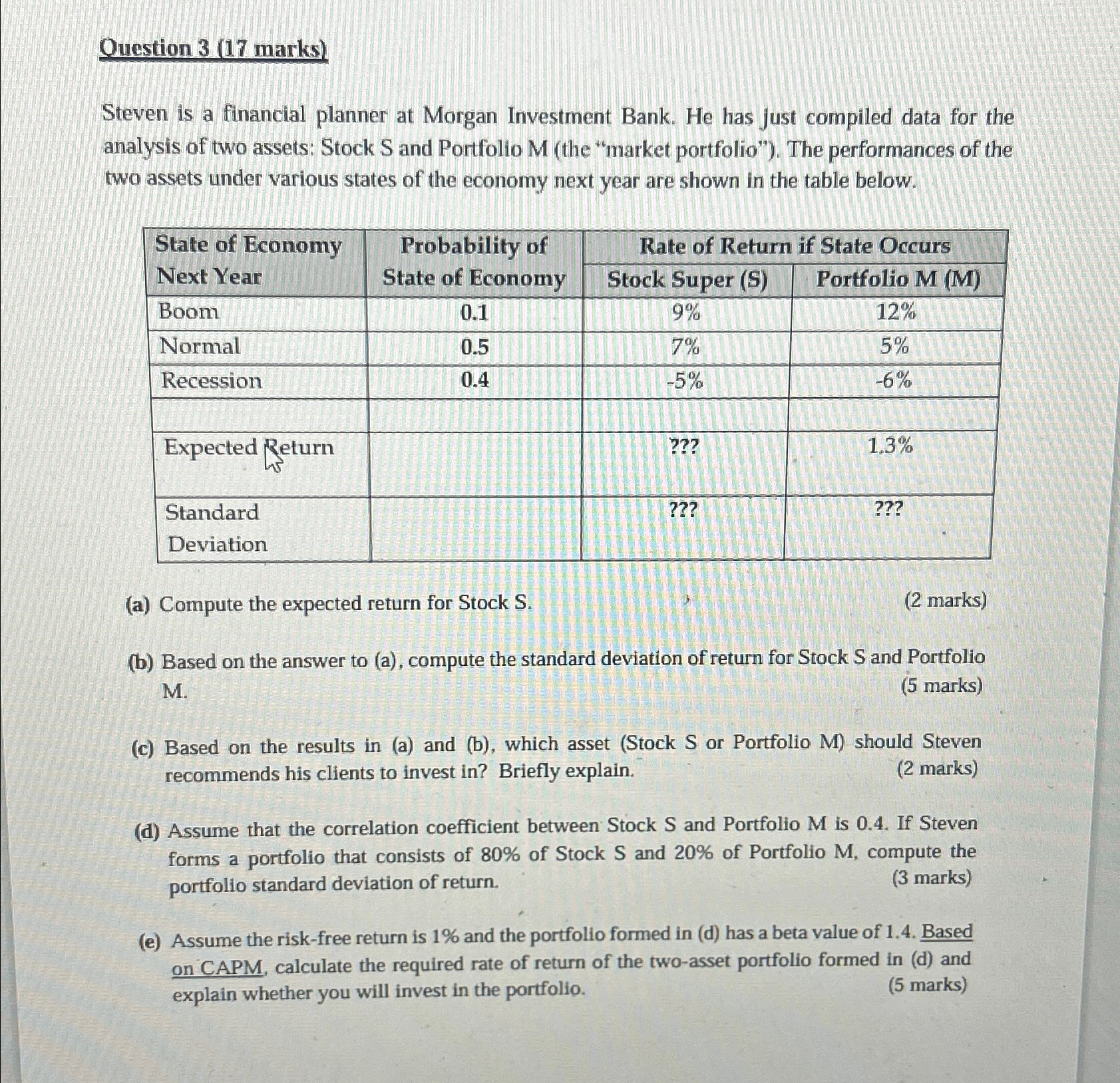

Question 3 (17 marks) Steven is a financial planner at Morgan Investment Bank. He has just compiled data for the analysis of two assets: Stock S and Portfolio M (the "market portfolio"). The performances of the two assets under various states of the economy next year are shown in the table below. State of Economy Next Year Boom Normal Recession Probability of State of Economy Rate of Return if State Occurs Stock Super (S) Portfolio M (M) 0.1 9% 12% 0.5 7% 5% 0.4 -5% -6% Expected Return Standard Deviation (a) Compute the expected return for Stock S. ??? 1.3% ??? ??? (2 marks) (b) Based on the answer to (a), compute the standard deviation of return for Stock S and Portfolio M. (5 marks) (c) Based on the results in (a) and (b), which asset (Stock S or Portfolio M) should Steven recommends his clients to invest in? Briefly explain. (2 marks) (d) Assume that the correlation coefficient between Stock S and Portfolio M is 0.4. If Steven forms a portfolio that consists of 80% of Stock S and 20% of Portfolio M, compute the (3 marks) portfolio standard deviation of return. (e) Assume the risk-free return is 1% and the portfolio formed in (d) has a beta value of 1.4. Based on CAPM, calculate the required rate of return of the two-asset portfolio formed in (d) and (5 marks) explain whether you will invest in the portfolio. Question 3 (17 marks) Steven is a financial planner at Morgan Investment Bank. He has just compiled data for the analysis of two assets: Stock S and Portfolio M (the "market portfolio"). The performances of the two assets under various states of the economy next year are shown in the table below. State of Economy Next Year Boom Normal Recession Probability of State of Economy Rate of Return if State Occurs Stock Super (S) Portfolio M (M) 0.1 9% 12% 0.5 7% 5% 0.4 -5% -6% Expected Return Standard Deviation (a) Compute the expected return for Stock S. ??? 1.3% ??? ??? (2 marks) (b) Based on the answer to (a), compute the standard deviation of return for Stock S and Portfolio M. (5 marks) (c) Based on the results in (a) and (b), which asset (Stock S or Portfolio M) should Steven recommends his clients to invest in? Briefly explain. (2 marks) (d) Assume that the correlation coefficient between Stock S and Portfolio M is 0.4. If Steven forms a portfolio that consists of 80% of Stock S and 20% of Portfolio M, compute the (3 marks) portfolio standard deviation of return. (e) Assume the risk-free return is 1% and the portfolio formed in (d) has a beta value of 1.4. Based on CAPM, calculate the required rate of return of the two-asset portfolio formed in (d) and (5 marks) explain whether you will invest in the portfolio.

Expert Answer:

Posted Date:

Students also viewed these finance questions

-

The accompanying table shows proportions of computer salespeople classified according to marital status and whether they left their jobs or stayed over a period of 1 year. a. What is the probability...

-

A cylindrical metal specimen having an original diameter of 12.8 mm (0.505 in.) and gauge length of 50.80 mm (2.000 in.) is pulled in tension until fracture occurs. The diameter at the point of...

-

State the purpose of a reporting system.

-

When calculating a firms return on shareholders equity (ROE), some investment professionals modify the ROE ratio by subtracting any dividends paid by the firm to its preferred stock shareholders as...

-

Hilo Corporation applies fixed overhead at the rate of $3.30 per unit. Budgeted fixed overhead was $407,160. This month 128,000 units were produced, and actual overhead was $390,660. Required What...

-

Continue 100000 $ Eliminate (Decrease) Sales $ 0 $ -100000 Variable costs Cost of goods sold 60000 0 60000 Operating expenses 30000 i 0 30000 Total variable 90000 0 90000 Contribution margin Fixed...

-

Two soil samples were subjected to pressure cell (Tempe Cell, Fredlund SWCC Device) to determine the SWCC of the soils. Data obtained from the experimental work are given in the following table...

-

Explain the positive and negative aspects of speculation in financial markets.

-

what is a reason for using just one rate , a long term yield as the average cost of debt financing for a firm that has multiple issues of debt wtih varyiny maturities?

-

What recommendations can help her organize ideas in planning stage old writing step?

-

Based on analysis, deck-building business is best Only consider what is an added cost and different from current business, if shifting things from current business to new then do not include

-

How does risk management practices help organisations to prepare for unexpected events, help with financial planning, assist in effective utilisation and allocation of funds, improve profitability,...

-

Problem#2 A laboratory provides the following solids analysis for a wastewater sample: TS = 290 mg/L; TDS = 37 mg/L; FSS = 38 mg/L. a) How you can measure the following parameters: (9 pt.) Fixed...

-

Global.asax is used for: a. declare application variables O b. all other answers are wrong O c. declare global variables O d. handle application events

-

what spanning tree does the Spanning Tree One Step function find when the order of edges is: (a) \(\{\{5,6\},\{4,5\},\{3,4\},\{2,6\},\{2,5\}\),...

-

Prove that a connected, undirected graph \(G\) is a tree if and only if for each edge \(\{u, v\} \in G, G-\{u, v\}\) is not connected.

-

Suppose that \(G=(V, E)\) is a connected graph and \(\{u, v\} \in E\) is an edge in some cycle. Show that the graph \(G^{\prime}=(V, E)-\{u, v\}\) is connected. (This fact was used in the proof of...

Study smarter with the SolutionInn App