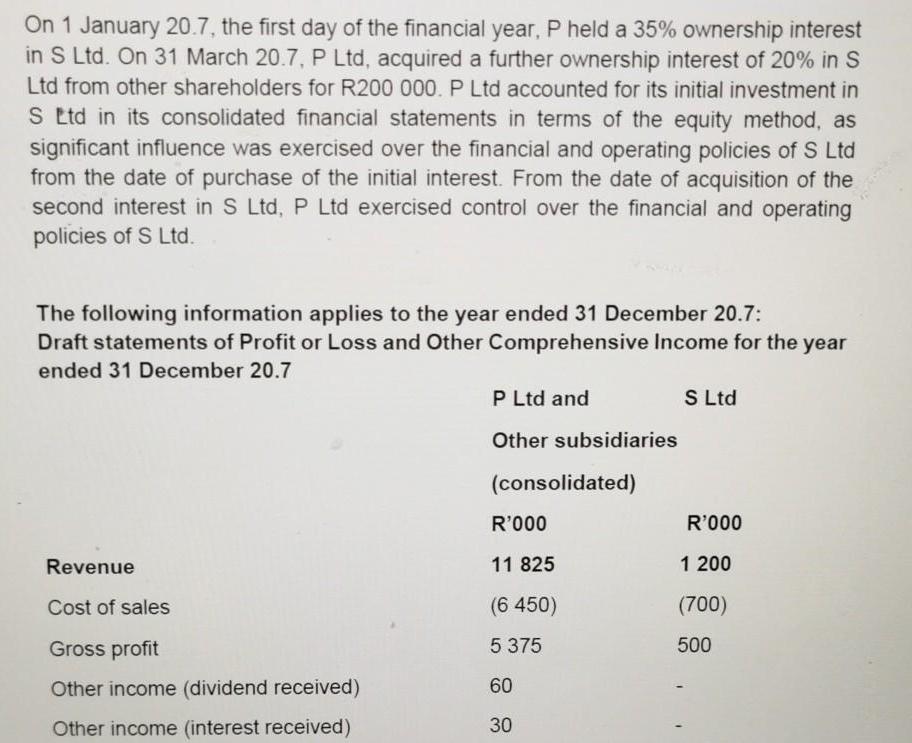

On 1 January 20.7, the first day of the financial year, P held a 35% ownership...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

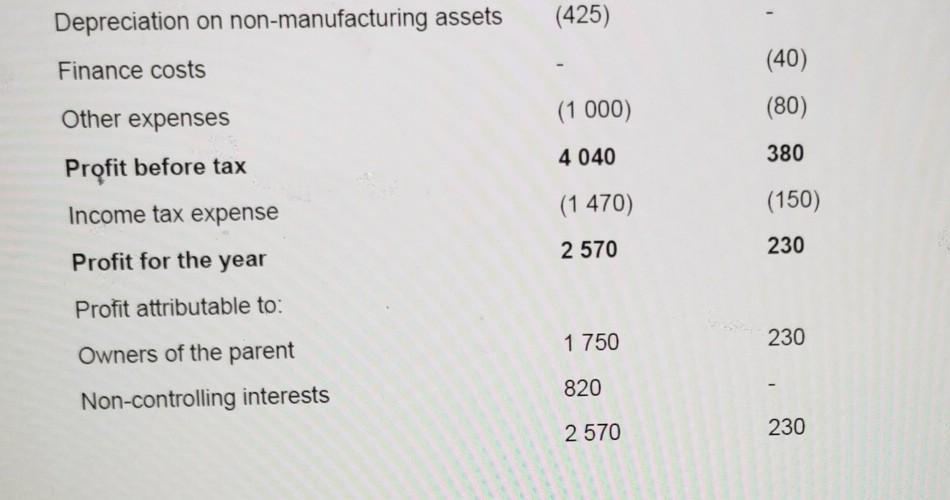

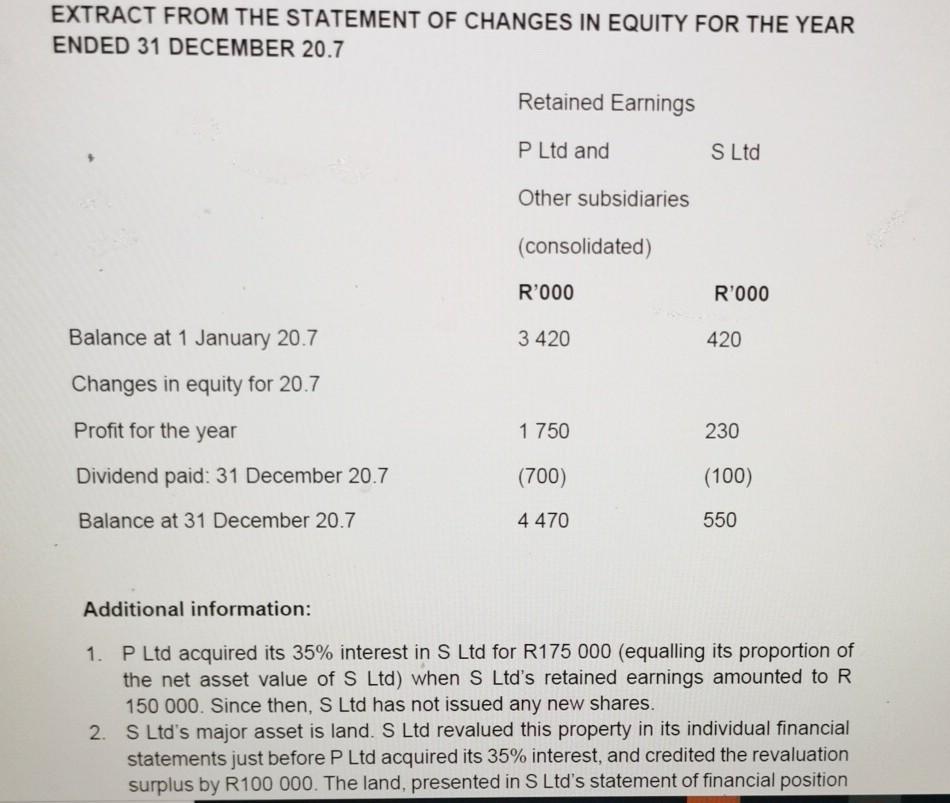

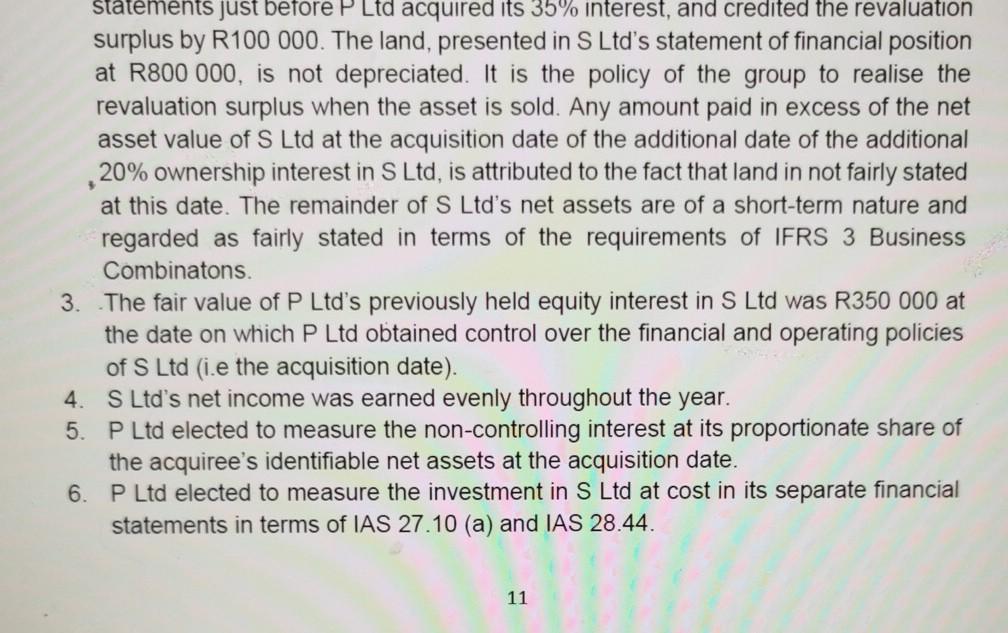

On 1 January 20.7, the first day of the financial year, P held a 35% ownership interest in S Ltd. On 31 March 20.7, P Ltd, acquired a further ownership interest of 20% in S Ltd from other shareholders for R200 000. P Ltd accounted for its initial investment in S ttd in its consolidated financial statements in terms of the equity method, as significant influence was exercised over the financial and operating policies of S Ltd from the date of purchase of the initial interest. From the date of acquisition of the second interest in S Ltd, P Ltd exercised control over the financial and operating policies of S Ltd. The following information applies to the year ended 31 December 20.7: Draft statements of Profit or Loss and Other Comprehensive Income for the year ended 31 December 20.7 S Ltd Revenue Cost of sales Gross profit Other income (dividend received) Other income (interest received) P Ltd and Other subsidiaries (consolidated) R'000 11 825 (6 450) 5 375 60 30 R'000 1 200 (700) 500 Depreciation on non-manufacturing assets (425) Finance costs Other expenses Profit before tax Income tax expense Profit for the year Profit attributable to: Owners of the parent Non-controlling interests (1000) 4 040 (1470) 2 570 1 750 820 2570 (40) (80) 380 (150) 230 230 230 EXTRACT FROM THE STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 31 DECEMBER 20.7 Balance at 1 January 20.7 Changes in equity for 20.7 Profit for the year Dividend paid: 31 December 20.7 Balance at 31 December 20.7 Retained Earnings P Ltd and Other subsidiaries (consolidated) R'000 3 420 1 750 (700) 4 470 S Ltd R'000 420 230 (100) 550 Additional information: 1. P Ltd acquired its 35% interest in S Ltd for R175 000 (equalling its proportion of the net asset value of S Ltd) when S Ltd's retained earnings amounted to R 150 000. Since then, S Ltd has not issued any new shares. 2. S Ltd's major asset is land. S Ltd revalued this property in its individual financial statements just before P Ltd acquired its 35% interest, and credited the revaluation surplus by R100 000. The land, presented in S Ltd's statement of financial position statements just before P Ltd acquired its 35% interest, and credited the revaluation surplus by R100 000. The land, presented in S Ltd's statement of financial position at R800 000, is not depreciated. It is the policy of the group to realise the revaluation surplus when the asset is sold. Any amount paid in excess of the net asset value of S Ltd at the acquisition date of the additional date of the additional 20% ownership interest in S Ltd, is attributed to the fact that land in not fairly stated at this date. The remainder of S Ltd's net assets are of a short-term nature and regarded as fairly stated in terms of the requirements of IFRS 3 Business Combinatons. 3. The fair value of P Ltd's previously held equity interest in S Ltd was R350 000 at the date on which P Ltd obtained control over the financial and operating policies of S Ltd (i.e the acquisition date). S Ltd's net income was earned evenly throughout the year. P Ltd elected to measure the non-controlling interest at its proportionate share of the acquiree's identifiable net assets at the acquisition date. 6. P Ltd elected to measure the investment in S Ltd at cost in its separate financial statements in terms of IAS 27.10 (a) and IAS 28.44. 4. 5. 11 October E... x 12 / 12 7. Assume that the opening balance of the non-controlling interest of P Ltd an other subsidiaries at 1 January 20.7 was R1 million. 8. A company tax rate of 30% applies and CGT is calculated at 50% thereof. Required Prepare the consolidated statement of profit or loss and other comprehensive income and the consolidated statement of changes in equity (column for share capital is not required) of the P Ltd Group for the year ended 31 December 20.7. On 1 January 20.7, the first day of the financial year, P held a 35% ownership interest in S Ltd. On 31 March 20.7, P Ltd, acquired a further ownership interest of 20% in S Ltd from other shareholders for R200 000. P Ltd accounted for its initial investment in S ttd in its consolidated financial statements in terms of the equity method, as significant influence was exercised over the financial and operating policies of S Ltd from the date of purchase of the initial interest. From the date of acquisition of the second interest in S Ltd, P Ltd exercised control over the financial and operating policies of S Ltd. The following information applies to the year ended 31 December 20.7: Draft statements of Profit or Loss and Other Comprehensive Income for the year ended 31 December 20.7 S Ltd Revenue Cost of sales Gross profit Other income (dividend received) Other income (interest received) P Ltd and Other subsidiaries (consolidated) R'000 11 825 (6 450) 5 375 60 30 R'000 1 200 (700) 500 Depreciation on non-manufacturing assets (425) Finance costs Other expenses Profit before tax Income tax expense Profit for the year Profit attributable to: Owners of the parent Non-controlling interests (1000) 4 040 (1470) 2 570 1 750 820 2570 (40) (80) 380 (150) 230 230 230 EXTRACT FROM THE STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 31 DECEMBER 20.7 Balance at 1 January 20.7 Changes in equity for 20.7 Profit for the year Dividend paid: 31 December 20.7 Balance at 31 December 20.7 Retained Earnings P Ltd and Other subsidiaries (consolidated) R'000 3 420 1 750 (700) 4 470 S Ltd R'000 420 230 (100) 550 Additional information: 1. P Ltd acquired its 35% interest in S Ltd for R175 000 (equalling its proportion of the net asset value of S Ltd) when S Ltd's retained earnings amounted to R 150 000. Since then, S Ltd has not issued any new shares. 2. S Ltd's major asset is land. S Ltd revalued this property in its individual financial statements just before P Ltd acquired its 35% interest, and credited the revaluation surplus by R100 000. The land, presented in S Ltd's statement of financial position statements just before P Ltd acquired its 35% interest, and credited the revaluation surplus by R100 000. The land, presented in S Ltd's statement of financial position at R800 000, is not depreciated. It is the policy of the group to realise the revaluation surplus when the asset is sold. Any amount paid in excess of the net asset value of S Ltd at the acquisition date of the additional date of the additional 20% ownership interest in S Ltd, is attributed to the fact that land in not fairly stated at this date. The remainder of S Ltd's net assets are of a short-term nature and regarded as fairly stated in terms of the requirements of IFRS 3 Business Combinatons. 3. The fair value of P Ltd's previously held equity interest in S Ltd was R350 000 at the date on which P Ltd obtained control over the financial and operating policies of S Ltd (i.e the acquisition date). S Ltd's net income was earned evenly throughout the year. P Ltd elected to measure the non-controlling interest at its proportionate share of the acquiree's identifiable net assets at the acquisition date. 6. P Ltd elected to measure the investment in S Ltd at cost in its separate financial statements in terms of IAS 27.10 (a) and IAS 28.44. 4. 5. 11 October E... x 12 / 12 7. Assume that the opening balance of the non-controlling interest of P Ltd an other subsidiaries at 1 January 20.7 was R1 million. 8. A company tax rate of 30% applies and CGT is calculated at 50% thereof. Required Prepare the consolidated statement of profit or loss and other comprehensive income and the consolidated statement of changes in equity (column for share capital is not required) of the P Ltd Group for the year ended 31 December 20.7.

Expert Answer:

Answer rating: 100% (QA)

According R200000 assume to question 20 in S Ltd there is St March 31 ... View the full answer

Related Book For

Essentials of Accounting for Governmental and Not-for-Profit Organizations

ISBN: 978-0073527055

10th Edition

Authors: Paul A. Copley

Posted Date:

Students also viewed these accounting questions

-

On January 1, 2012, the first day of its fiscal year, the City of Carter received notification that a federal grant in the amount of $650,000 was approved. The grant was restricted for the payment of...

-

On January 1, 2017, the first day of its fiscal year, Carter City received notification that a federal grant in the amount of $560,000 was approved. The grant was restricted for the payment of wages...

-

On January 1, the first day of the fiscal year, a company issues a $500,000, 5%, 10-year bond that pays semiannual interest of $12,500 ($500,000 5% year), receiving cash of $500,000. Journalize...

-

What are the premises for successful paleostress analysis?

-

If some countries clearly adopt the country- of-origin approach for legal issues of e-commerce, online retailers might relocate to operate from those countries. Why?

-

Suppose that you are working with Rick and Carla when a new systems request comes in. SWLs vice president of marketing, Amy Neal, wants to change the catalog mailing program and provide a reward for...

-

Which method of evaluating capital investment proposals reduces their expected future net cash flows to present values and compares the total present values to the amount of the investment?

-

The Pedal Pusher Bicycle Shop operates 7 days per week, closing only on Christmas Day. The shop pays $300 for a particular bicycle purchased from the manufacturer. The annual holding cost per bicycle...

-

Colgate-Palmolive: Cleopatra Case Study From the perspective of Steve Boyd, evaluate both the qualitative and quantitative data to decide whether achieving the target market share of 4.5% is feasible...

-

The soil mass in Figure P9-13 is loaded by a force transmitted through a circular footing as shown. Determine the stresses in the soil. Compare the values of r using an axisymmetric model with the ...

-

(ii) The market consists of the following stocks. Their prices and number of shares are as follows: Stock Price Number of Shares Outstanding A $10 100,000 B 20 10,000 C 30 200,000 D 40 50,000 (a)...

-

Discuss the five types of internal controls and give an example of each one.

-

How does the body effect change the small-signal equivalent circuit of the MOSFET?

-

Sketch a simple common-source amplifier circuit and discuss the general ac circuit characteristics (voltage gain and output resistance).

-

Specify the matters that must be proved by a plaintiff to the satisfaction of the court before a claim for negligence can succeed.

-

How does an audit checklist differ from the audit program?

-

1 - Why is governmental regulation important for the UAS industry? 2 - Should UAV pilots be rated in manned aircraft? 3 - Should observers be required for UAV operations? 4 - What are some operations...

-

Thalina Mineral Works is one of the worlds leading producers of cultured pearls. The companys condensed statement of cash flows for the years 20182020 follows. Required Comment on Thalina Mineral...

-

Using the annual report obtained for Exercise 11, answer the following questions. a. Look at the Statement of Revenues, Expenditures, and Changes in Fund Balances for the governmental funds. List the...

-

What are the required financial statements of the U.S. government?

-

The City of South Dundee budget for the fiscal year ended June 30, 2012, included an appropriation for the police department in the amount of $16,000,000. During the month of July 2011, the following...

-

For the graph of Figure 1.9, verify that \(A^{m}\) is not entirely non-zero for any \(m 3 2 Figure 1.9 - Paths of length 4 exist between each pair of vertices

-

Show that a connected directed graph is quasi-connected. Show that an undirected graph is quasi-connected if and only if it is connected.

-

Find all connected components of the graph below. 11 12 16

Study smarter with the SolutionInn App