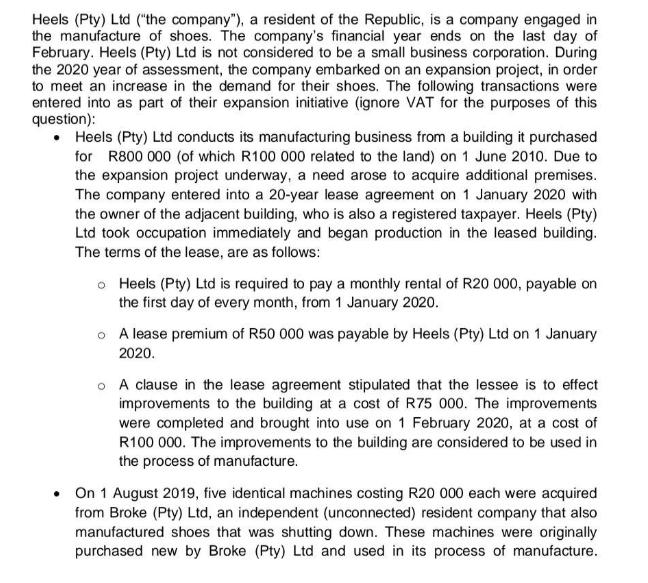

Heels (Pty) Ltd (the company), a resident of the Republic, is a company engaged in the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

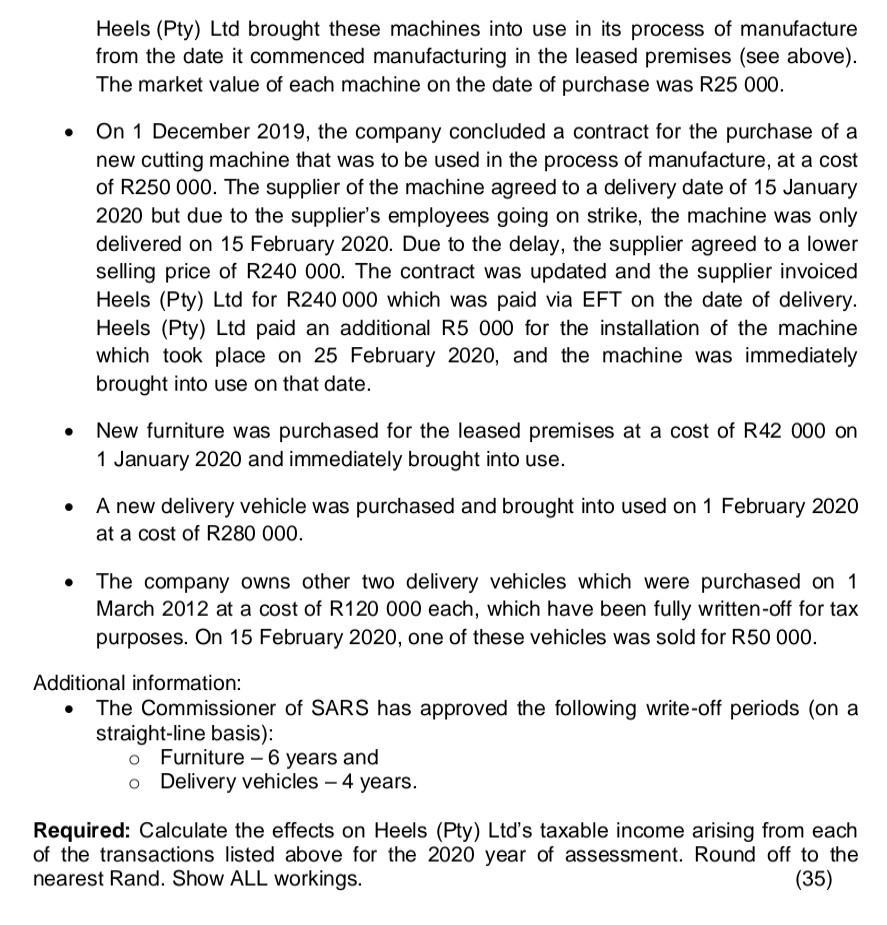

Heels (Pty) Ltd ("the company"), a resident of the Republic, is a company engaged in the manufacture of shoes. The company's financial year ends on the last day of February. Heels (Pty) Ltd is not considered to be a small business corporation. During the 2020 year of assessment, the company embarked on an expansion project, in order to meet an increase in the demand for their shoes. The following transactions were entered into as part of their expansion initiative (ignore VAT for the purposes of this question): • Heels (Pty) Ltd conducts its manufacturing business from a building it purchased for R800 000 (of which R100 000 related to the land) on 1 June 2010. Due to the expansion project underway, a need arose to acquire additional premises. The company entered into a 20-year lease agreement on 1 January 2020 with the owner of the adjacent building, who is also a registered taxpayer. Heels (Pty) Ltd took occupation immediately and began production in the leased building. The terms of the lease, are as follows: o Heels (Pty) Ltd is required to pay a monthly rental of R20 000, payable on the first day of every month, from 1 January 2020. o A lease premium of R50 000 was payable by Heels (Pty) Ltd on 1 January 2020. O A clause in the lease agreement stipulated that the lessee is to effect improvements to the building at a cost of R75 000. The improvements were completed and brought into use on 1 February 2020, at a cost of R100 000. The improvements to the building are considered to be used in the process of manufacture. On 1 August 2019, five identical machines costing R20 000 each were acquired from Broke (Pty) Ltd, an independent (unconnected) resident company that also manufactured shoes that was shutting down. These machines were originally purchased new by Broke (Pty) Ltd and used in its process of manufacture. Heels (Pty) Ltd brought these machines into use in its process of manufacture from the date it commenced manufacturing in the leased premises (see above). The market value of each machine on the date of purchase was R25 000. On 1 December 2019, the company concluded a contract for the purchase of a new cutting machine that was to be used in the process of manufacture, at a cost of R250 000. The supplier of the machine agreed to a delivery date of 15 January 2020 but due to the supplier's employees going on strike, the machine was only delivered on 15 February 2020. Due to the delay, the supplier agreed to a lower selling price of R240 000. The contract was updated and the supplier invoiced Heels (Pty) Ltd for R240 000 which was paid via EFT on the date of delivery. Heels (Pty) Ltd paid an additional R5 000 for the installation of the machine which took place on 25 February 2020, and the machine was immediately brought into use on that date. New furniture was purchased for the leased premises at a cost of R42 000 on 1 January 2020 and immediately brought into use. A new delivery vehicle was purchased and brought into used on 1 February 2020 at a cost of R280 000. The company owns other two delivery vehicles which were purchased on 1 March 2012 at a cost of R120 000 each, which have been fully written-off for tax purposes. On 15 February 2020, one of these vehicles was sold for R50 000. Additional information: The Commissioner of SARS has approved the following write-off periods (on a straight-line basis): o Furniture – 6 years and o Delivery vehicles - 4 years. Required: Calculate the effects on Heels (Pty) Ltd's taxable income arising from each of the transactions listed above for the 2020 year of assessment. Round off to the nearest Rand. Show ALL workings. (35) Heels (Pty) Ltd ("the company"), a resident of the Republic, is a company engaged in the manufacture of shoes. The company's financial year ends on the last day of February. Heels (Pty) Ltd is not considered to be a small business corporation. During the 2020 year of assessment, the company embarked on an expansion project, in order to meet an increase in the demand for their shoes. The following transactions were entered into as part of their expansion initiative (ignore VAT for the purposes of this question): • Heels (Pty) Ltd conducts its manufacturing business from a building it purchased for R800 000 (of which R100 000 related to the land) on 1 June 2010. Due to the expansion project underway, a need arose to acquire additional premises. The company entered into a 20-year lease agreement on 1 January 2020 with the owner of the adjacent building, who is also a registered taxpayer. Heels (Pty) Ltd took occupation immediately and began production in the leased building. The terms of the lease, are as follows: o Heels (Pty) Ltd is required to pay a monthly rental of R20 000, payable on the first day of every month, from 1 January 2020. o A lease premium of R50 000 was payable by Heels (Pty) Ltd on 1 January 2020. O A clause in the lease agreement stipulated that the lessee is to effect improvements to the building at a cost of R75 000. The improvements were completed and brought into use on 1 February 2020, at a cost of R100 000. The improvements to the building are considered to be used in the process of manufacture. On 1 August 2019, five identical machines costing R20 000 each were acquired from Broke (Pty) Ltd, an independent (unconnected) resident company that also manufactured shoes that was shutting down. These machines were originally purchased new by Broke (Pty) Ltd and used in its process of manufacture. Heels (Pty) Ltd brought these machines into use in its process of manufacture from the date it commenced manufacturing in the leased premises (see above). The market value of each machine on the date of purchase was R25 000. On 1 December 2019, the company concluded a contract for the purchase of a new cutting machine that was to be used in the process of manufacture, at a cost of R250 000. The supplier of the machine agreed to a delivery date of 15 January 2020 but due to the supplier's employees going on strike, the machine was only delivered on 15 February 2020. Due to the delay, the supplier agreed to a lower selling price of R240 000. The contract was updated and the supplier invoiced Heels (Pty) Ltd for R240 000 which was paid via EFT on the date of delivery. Heels (Pty) Ltd paid an additional R5 000 for the installation of the machine which took place on 25 February 2020, and the machine was immediately brought into use on that date. New furniture was purchased for the leased premises at a cost of R42 000 on 1 January 2020 and immediately brought into use. A new delivery vehicle was purchased and brought into used on 1 February 2020 at a cost of R280 000. The company owns other two delivery vehicles which were purchased on 1 March 2012 at a cost of R120 000 each, which have been fully written-off for tax purposes. On 15 February 2020, one of these vehicles was sold for R50 000. Additional information: The Commissioner of SARS has approved the following write-off periods (on a straight-line basis): o Furniture – 6 years and o Delivery vehicles - 4 years. Required: Calculate the effects on Heels (Pty) Ltd's taxable income arising from each of the transactions listed above for the 2020 year of assessment. Round off to the nearest Rand. Show ALL workings. (35)

Expert Answer:

Related Book For

Business Its Legal Ethical and Global Environment

ISBN: 978-1337103572

11th edition

Authors: Marianne M. Jennings

Posted Date:

Students also viewed these accounting questions

-

The side chain of tryptophan is not considered to be basic, despite the fact that it possesses a nitrogen atom with a lone pair. Explain.

-

(c) 12.4 1. Jakesis a sole trader. His financial year ends on 30 September each year. He drew up the following trial balance When it was totalled it was found that totals of two sides did not agree,...

-

Day Corp. entered into a finance lease agreement with Night Leasing Ltd. on January 1, 2016. Day Corp. agreed to pay Night annual payments of $24,154 on December 31 for the next three years to lease...

-

Following the 2017 General Election and change of government, the Labour-led coalition government established a Tax Working Group (TWG) to consider the overall structure, balance and fairness of the...

-

Assume that effective forecasting requires a combination of technique, system support, and administration. Your supervisor in your consumer products firm has requested that you identify some...

-

The capacitances of the four capacitors shown in Figure are given in terms of a certain quantity C. (a) It C = 50F, what is the equivalent capacitance between points A and B? (b) Repeat for points A...

-

The accounts of Highland Consulting, Inc., follow with their normal balances at August 31, 2010. The accounts are listed in no particular order. Requirements 1. Prepare the companys trial balance at...

-

Child Corporation joined the Thrust consolidated group in year 1. At the time it joined the group, Child held a $2 million NOL carryforward. On a consolidated basis, the members of Thrust generated...

-

What is the difference between future value and present value? What data do you need to future value or present value calculation?What are various ways to calculate the time value of money in...

-

Problem 2: A single-piece bicycle crank is shown below under the following loading scenario: the rider is pedaling forward by applying a vertical force Fp = 500 N on the left pedal and no force on...

-

A local pawn shop has 10 items for sale. The prices of the items (in dollars) are given below. 23, 28, 41, 51, 61, 72, 85, 86, 88, 92 For the above data, find: (2 points each) a. The range (round to...

-

Determine the attached wide I-bar HE100Bpermissible torque Tsall when permittedshear stress ?sall = 115 MPa. What isthen permissible distortion ?allowable (?/m)G = 80 GPa 100 mm 100

-

In 1965, the United States was at war with North Vietnam. Many people protested against it. Inspired, several students in Des Moines, Iowa planned a protest. They decided to wear black armbands with...

-

Write a javascript program to display the grade of a student 1) Text 1-Student Name 2) Text 2-Student Id 3) Text 3 - Mark 4) Button - When you click the button display the grade in Paragraph (apply...

-

Your customer Gods Blessing Enterprise Ltd is negotiating with Joe Bloggs Ltd of UK for the supply of Cars to Lectures and Medical Doctors valued at 150,000,000. The terms of payment are 60 days...

-

Given the frequency distribution for the data, Age Frequency Relative Frequency Cumulative Relative Frequency [20,29] 0.0333 [30,39] 0.3 0.3667 [40,49] [50,59] 0.5334 [60,69] 0.8001 [70,79] 0.9668...

-

To determine the issue price of a term bond, the present value of the principal and interest payments must be found using the stated interest rate.true or false

-

President Lee Coone has asked you to continue planning for an integrated corporate NDAS network. Ultimately, this network will link all the offices with the Tampa head office and become the...

-

Rhodes tripped over a hospital cord while visiting a patient in the Detroit Medical Center. She fell and was injured. She filed suit against the hospital for negligence in the condition of its...

-

William H. Sullivan, Jr. gained control of the New England Patriots Football Club (Patriots) by forming a separate corporation (New Patriots) and merging it with the old one. Plaintiffs are a class...

-

Wendy Komac was hired by Gordon Food Service as a salesperson. During the course of her employment, Gordon held sales contests such as the Winners Circle competition, which rewarded the salesperson...

-

Mary Todd is uncertain about several relationships pertaining to audit sampling. As Mary's supervisor, explain the application of audit sampling to (1) GAAS and (2) the components of audit risk.

-

a. Distinguish between sampling risk and nonsampling risk. b. Explain the types of sampling risk that may occur in auditing and their potential effects on the audit.

-

Warren Boyd, a beginning staff accountant, believes that audit sampling applies only to tests of controls, but may be used with all auditing procedures relating to tests of controls. Is Warren...

Study smarter with the SolutionInn App