Round all of your answers to the nearest cent when appropriate to do so. Some questions...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

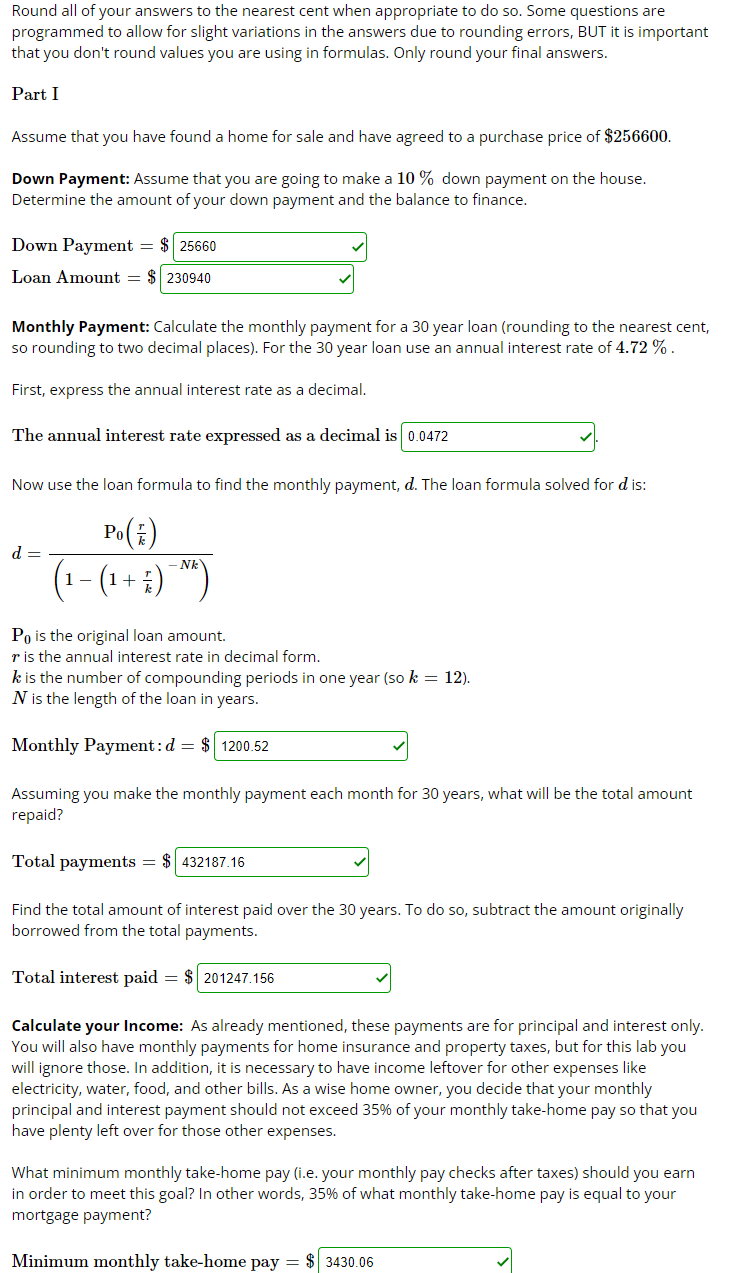

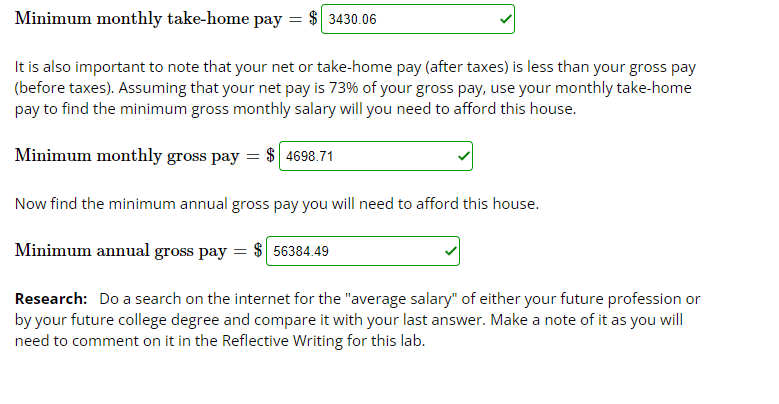

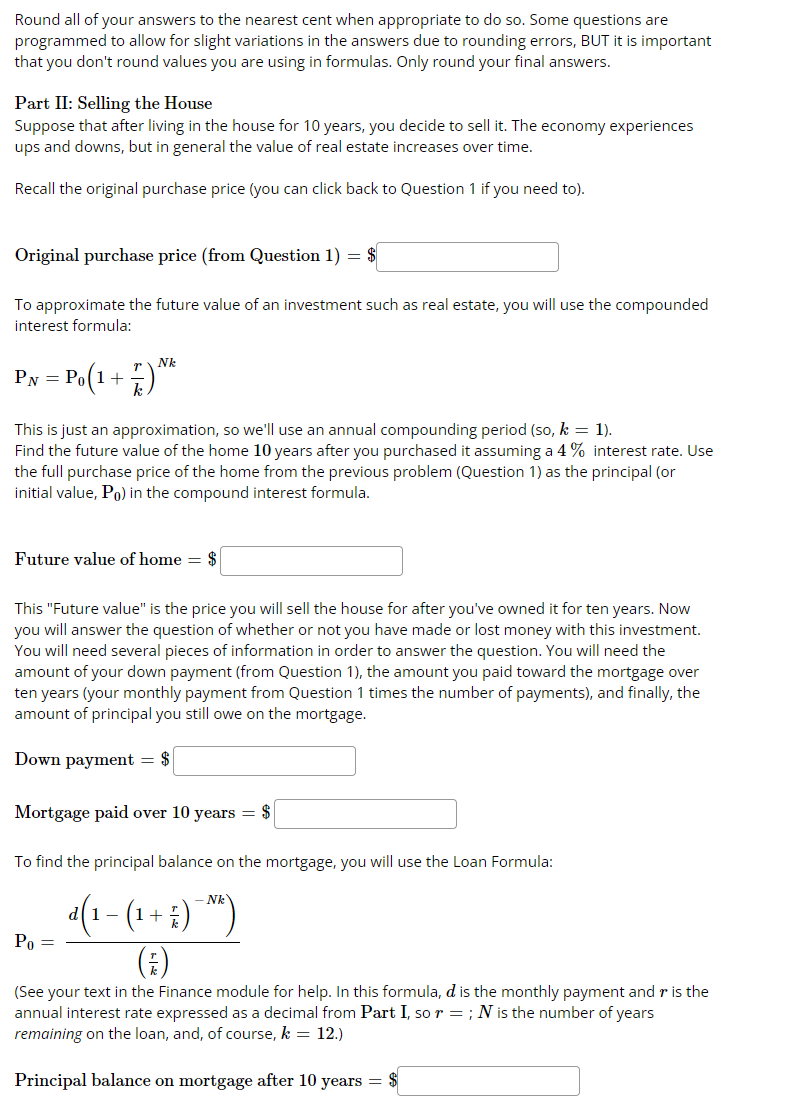

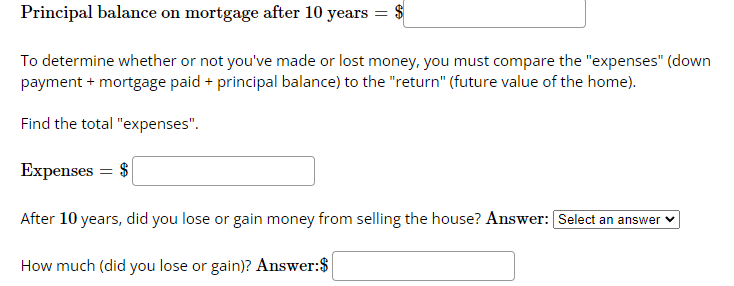

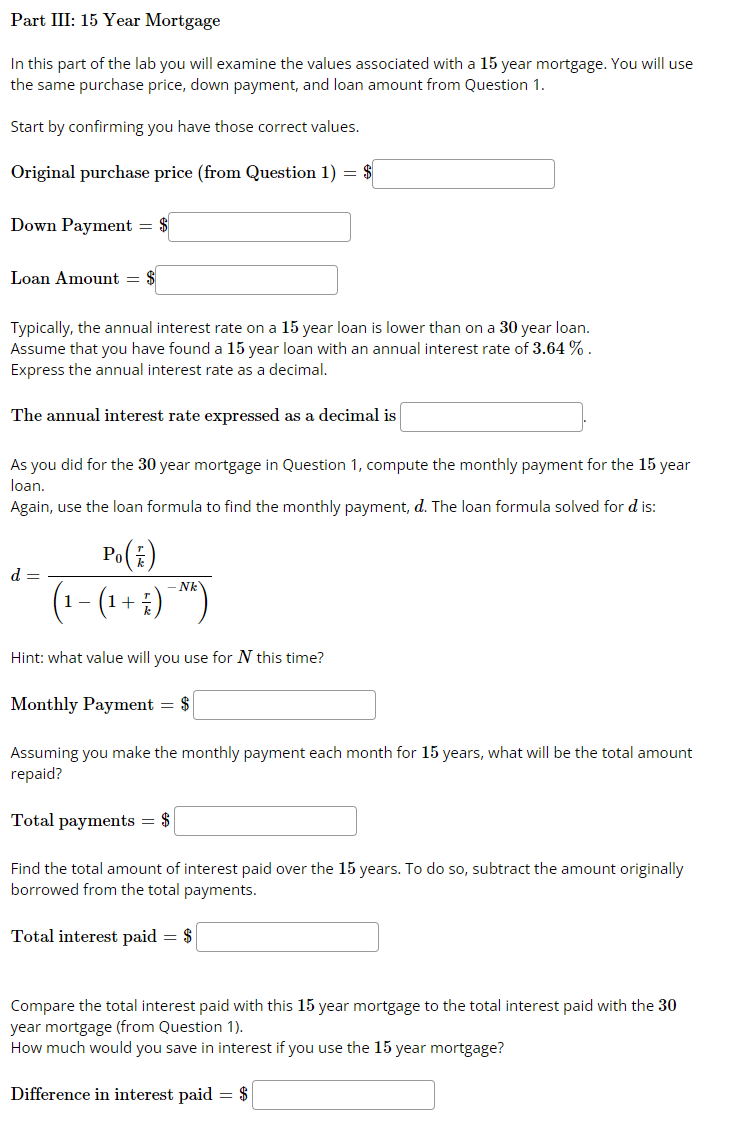

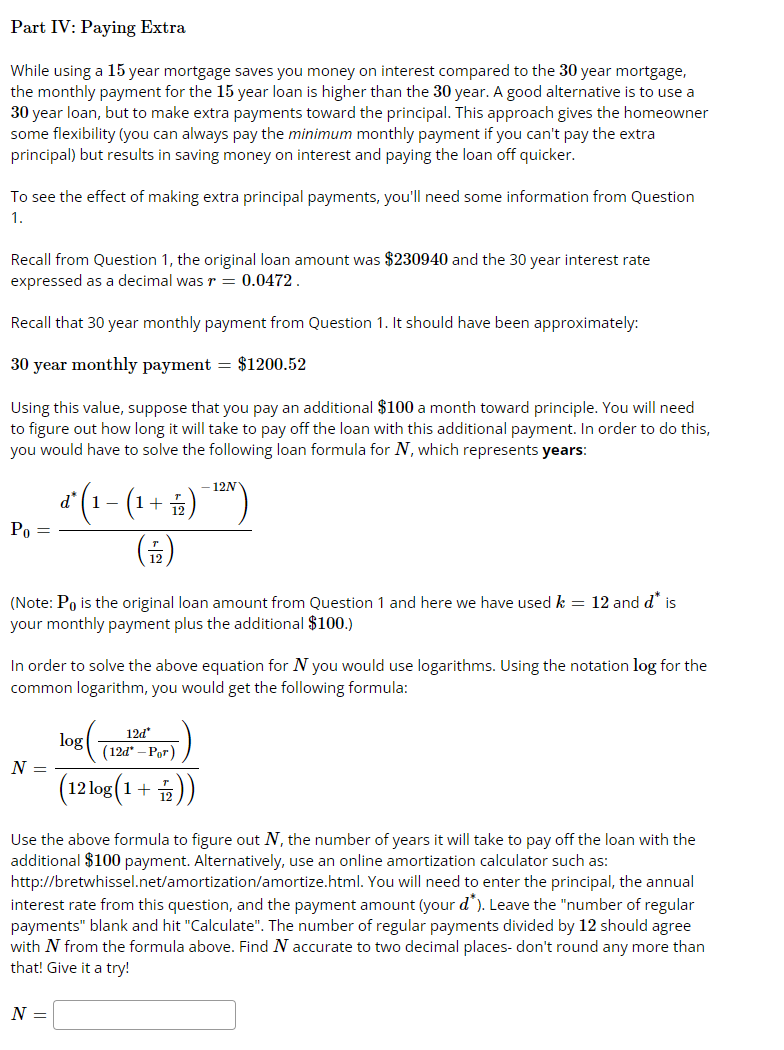

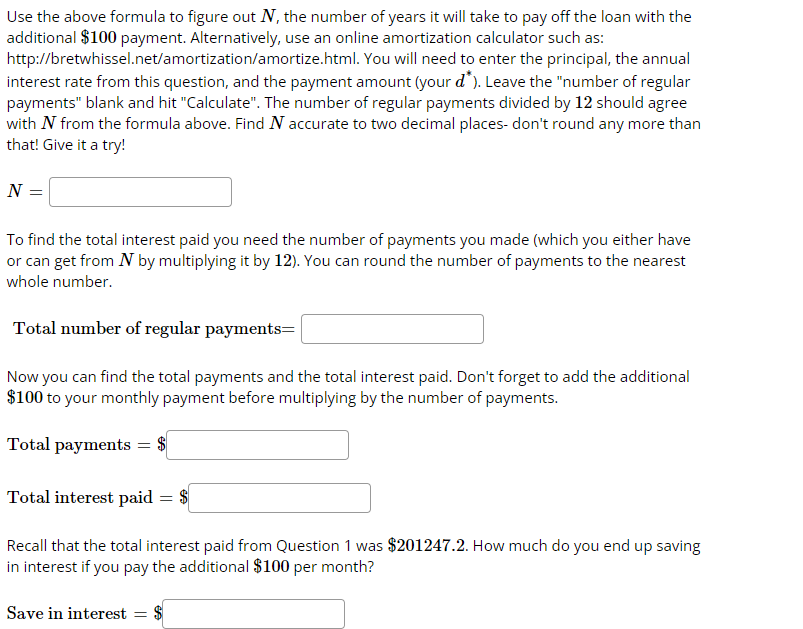

Round all of your answers to the nearest cent when appropriate to do so. Some questions are programmed to allow for slight variations in the answers due to rounding errors, BUT it is important that you don't round values you are using in formulas. Only round your final answers. Part I Assume that you have found a home for sale and have agreed to a purchase price of $256600. Down Payment: Assume that you are going to make a 10% down payment on the house. Determine the amount of your down payment and the balance to finance. Down Payment = $ 25660 Loan Amount = $ 230940 Monthly Payment: Calculate the monthly payment for a 30 year loan (rounding to the nearest cent, so rounding to two decimal places). For the 30 year loan use an annual interest rate of 4.72 %. First, express the annual interest rate as a decimal. The annual interest rate expressed as a decimal is 0.0472 Now use the loan formula to find the monthly payment, d. The loan formula solved for dis: d Po() (1-(1+)) Po is the original loan amount. r is the annual interest rate in decimal form. k is the number of compounding periods in one year (so k = 12). N is the length of the loan in years. Monthly Payment: d = $1200.52 Assuming you make the monthly payment each month for 30 years, what will be the total amount repaid? Total payments = $ 432187.16 Find the total amount of interest paid over the 30 years. To do so, subtract the amount originally borrowed from the total payments. Total interest paid = $ 201247.156 Calculate your Income: As already mentioned, these payments are for principal and interest only. You will also have monthly payments for home insurance and property taxes, but for this lab you will ignore those. In addition, it is necessary to have income leftover for other expenses like electricity, water, food, and other bills. As a wise home owner, you decide that your monthly principal and interest payment should not exceed 35% of your monthly take-home pay so that you have plenty left over for those other expenses. What minimum monthly take-home pay (i.e. your monthly pay checks after taxes) should you earn in order to meet this goal? In other words, 35% of what monthly take-home pay is equal to your mortgage payment? Minimum monthly take-home pay = $3430.06 Minimum monthly take-home pay = $3430.06 It is also important to note that your net or take-home pay (after taxes) is less than your gross pay (before taxes). Assuming that your net pay is 73% of your gross pay, use your monthly take-home pay to find the minimum gross monthly salary will you need to afford this house. Minimum monthly gross pay = $ 4698.71 Now find the minimum annual gross pay you will need to afford this house. Minimum annual gross pay = $ 56384.49 Research: Do a search on the internet for the "average salary" of either your future profession or by your future college degree and compare it with your last answer. Make a note of it as you will need to comment on it in the Reflective Writing for this lab. Round all of your answers to the nearest cent when appropriate to do so. Some questions are programmed to allow for slight variations in the answers due to rounding errors, BUT it is important that you don't round values you are using in formulas. Only round your final answers. Part II: Selling the House Suppose that after living in the house for 10 years, you decide to sell it. The economy experiences ups and downs, but in general the value of real estate increases over time. Recall the original purchase price (you can click back to Question 1 if you need to). Original purchase price (from Question 1) = $ To approximate the future value of an investment such as real estate, you will use the compounded interest formula: Nk PN = Po(1 + Po(1+) This is just an approximation, so we'll use an annual compounding period (so, k = 1). Find the future value of the home 10 years after you purchased it assuming a 4% interest rate. Use the full purchase price of the home from the previous problem (Question 1) as the principal (or initial value, Po) in the compound interest formula. Future value of home = $ This "Future value" is the price you will sell the house for after you've owned it for ten years. Now you will answer the question of whether or not you have made or lost money with this investment. You will need several pieces of information in order to answer the question. You will need the amount of your down payment (from Question 1), the amount you paid toward the mortgage over ten years (your monthly payment from Question 1 times the number of payments), and finally, the amount of principal you still owe on the mortgage. Down payment = $ Mortgage paid over 10 years = $ To find the principal balance on the mortgage, you will use the Loan Formula: Po= = - d(1 (1 + ) (1+)*) () (See your text in the Finance module for help. In this formula, d is the monthly payment and r is the annual interest rate expressed as a decimal from Part I, so r = ; N is the number of years remaining on the loan, and, of course, k = 12.) Principal balance on mortgage after 10 years = $ Principal balance on mortgage after 10 years = To determine whether or not you've made or lost money, you must compare the "expenses" (down payment + mortgage paid + principal balance) to the "return" (future value of the home). Find the total "expenses". Expenses = $ After 10 years, did you lose or gain money from selling the house? Answer: Select an answer How much (did you lose or gain)? Answer:$ Part III: 15 Year Mortgage In this part of the lab you will examine the values associated with a 15 year mortgage. You will use the same purchase price, down payment, and loan amount from Question 1. Start by confirming you have those correct values. Original purchase price (from Question 1) = $ Down Payment = $ Loan Amount $ Typically, the annual interest rate on a 15 year loan is lower than on a 30 year loan. Assume that you have found a 15 year loan with an annual interest rate of 3.64%. Express the annual interest rate as a decimal. The annual interest rate expressed as a decimal is As you did for the 30 year mortgage in Question 1, compute the monthly payment for the 15 year loan. Again, use the loan formula to find the monthly payment, d. The loan formula solved for d is: d = 1 Po W(S) - (1 + 2)-N) Hint: what value will you use for N this time? Monthly Payment = $ Assuming you make the monthly payment each month for 15 years, what will be the total amount repaid? Total payments = $ Find the total amount of interest paid over the 15 years. To do so, subtract the amount originally borrowed from the total payments. Total interest paid = $ Compare the total interest paid with this 15 year mortgage to the total interest paid with the 30 year mortgage (from Question 1). How much would you save in interest if you use the 15 year mortgage? Difference in interest paid = $ Part IV: Paying Extra While using a 15 year mortgage saves you money on interest compared to the 30 year mortgage, the monthly payment for the 15 year loan is higher than the 30 year. A good alternative is to use a 30 year loan, but to make extra payments toward the principal. This approach gives the homeowner some flexibility (you can always pay the minimum monthly payment if you can't pay the extra principal) but results in saving money on interest and paying the loan off quicker. To see the effect of making extra principal payments, you'll need some information from Question 1. Recall from Question 1, the original loan amount was $230940 and the 30 year interest rate expressed as a decimal was r = 0.0472. Recall that 30 year monthly payment from Question 1. It should have been approximately: 30 year monthly payment = $1200.52 Using this value, suppose that you pay an additional $100 a month toward principle. You will need to figure out how long it will take to pay off the loan with this additional payment. In order to do this, you would have to solve the following loan formula for N, which represents years: = 2(3-(0-1)) d + 12 (Note: Po is the original loan amount from Question 1 and here we have used k = 12 and d* is your monthly payment plus the additional $100.) In order to solve the above equation for N you would use logarithms. Using the notation log for the common logarithm, you would get the following formula: N = log 12d* (12d* -Por) (12 log(1+)) Use the above formula to figure out N, the number of years it will take to pay off the loan with the additional $100 payment. Alternatively, use an online amortization calculator such as: http://bretwhissel.net/amortization/amortize.html. You will need to enter the principal, the annual interest rate from this question, and the payment amount (your d*). Leave the "number of regular payments" blank and hit "Calculate". The number of regular payments divided by 12 should agree with N from the formula above. Find N accurate to two decimal places- don't round any more than that! Give it a try! N = Use the above formula to figure out N, the number of years it will take to pay off the loan with the additional $100 payment. Alternatively, use an online amortization calculator such as: http://bretwhissel.net/amortization/amortize.html. You will need to enter the principal, the annual interest rate from this question, and the payment amount (your d*). Leave the "number of regular payments" blank and hit "Calculate". The number of regular payments divided by 12 should agree with N from the formula above. Find N accurate to two decimal places- don't round any more than that! Give it a try! N = To find the total interest paid you need the number of payments you made (which you either have or can get from N by multiplying it by 12). You can round the number of payments to the nearest whole number. Total number of regular payments= Now you can find the total payments and the total interest paid. Don't forget to add the additional $100 to your monthly payment before multiplying by the number of payments. Total payments = $ Total interest paid: = $ Recall that the total interest paid from Question 1 was $201247.2. How much do you end up saving in interest if you pay the additional $100 per month? Save in interest = $ Round all of your answers to the nearest cent when appropriate to do so. Some questions are programmed to allow for slight variations in the answers due to rounding errors, BUT it is important that you don't round values you are using in formulas. Only round your final answers. Part I Assume that you have found a home for sale and have agreed to a purchase price of $256600. Down Payment: Assume that you are going to make a 10% down payment on the house. Determine the amount of your down payment and the balance to finance. Down Payment = $ 25660 Loan Amount = $ 230940 Monthly Payment: Calculate the monthly payment for a 30 year loan (rounding to the nearest cent, so rounding to two decimal places). For the 30 year loan use an annual interest rate of 4.72 %. First, express the annual interest rate as a decimal. The annual interest rate expressed as a decimal is 0.0472 Now use the loan formula to find the monthly payment, d. The loan formula solved for dis: d Po() (1-(1+)) Po is the original loan amount. r is the annual interest rate in decimal form. k is the number of compounding periods in one year (so k = 12). N is the length of the loan in years. Monthly Payment: d = $1200.52 Assuming you make the monthly payment each month for 30 years, what will be the total amount repaid? Total payments = $ 432187.16 Find the total amount of interest paid over the 30 years. To do so, subtract the amount originally borrowed from the total payments. Total interest paid = $ 201247.156 Calculate your Income: As already mentioned, these payments are for principal and interest only. You will also have monthly payments for home insurance and property taxes, but for this lab you will ignore those. In addition, it is necessary to have income leftover for other expenses like electricity, water, food, and other bills. As a wise home owner, you decide that your monthly principal and interest payment should not exceed 35% of your monthly take-home pay so that you have plenty left over for those other expenses. What minimum monthly take-home pay (i.e. your monthly pay checks after taxes) should you earn in order to meet this goal? In other words, 35% of what monthly take-home pay is equal to your mortgage payment? Minimum monthly take-home pay = $3430.06 Minimum monthly take-home pay = $3430.06 It is also important to note that your net or take-home pay (after taxes) is less than your gross pay (before taxes). Assuming that your net pay is 73% of your gross pay, use your monthly take-home pay to find the minimum gross monthly salary will you need to afford this house. Minimum monthly gross pay = $ 4698.71 Now find the minimum annual gross pay you will need to afford this house. Minimum annual gross pay = $ 56384.49 Research: Do a search on the internet for the "average salary" of either your future profession or by your future college degree and compare it with your last answer. Make a note of it as you will need to comment on it in the Reflective Writing for this lab. Round all of your answers to the nearest cent when appropriate to do so. Some questions are programmed to allow for slight variations in the answers due to rounding errors, BUT it is important that you don't round values you are using in formulas. Only round your final answers. Part II: Selling the House Suppose that after living in the house for 10 years, you decide to sell it. The economy experiences ups and downs, but in general the value of real estate increases over time. Recall the original purchase price (you can click back to Question 1 if you need to). Original purchase price (from Question 1) = $ To approximate the future value of an investment such as real estate, you will use the compounded interest formula: Nk PN = Po(1 + Po(1+) This is just an approximation, so we'll use an annual compounding period (so, k = 1). Find the future value of the home 10 years after you purchased it assuming a 4% interest rate. Use the full purchase price of the home from the previous problem (Question 1) as the principal (or initial value, Po) in the compound interest formula. Future value of home = $ This "Future value" is the price you will sell the house for after you've owned it for ten years. Now you will answer the question of whether or not you have made or lost money with this investment. You will need several pieces of information in order to answer the question. You will need the amount of your down payment (from Question 1), the amount you paid toward the mortgage over ten years (your monthly payment from Question 1 times the number of payments), and finally, the amount of principal you still owe on the mortgage. Down payment = $ Mortgage paid over 10 years = $ To find the principal balance on the mortgage, you will use the Loan Formula: Po= = - d(1 (1 + ) (1+)*) () (See your text in the Finance module for help. In this formula, d is the monthly payment and r is the annual interest rate expressed as a decimal from Part I, so r = ; N is the number of years remaining on the loan, and, of course, k = 12.) Principal balance on mortgage after 10 years = $ Principal balance on mortgage after 10 years = To determine whether or not you've made or lost money, you must compare the "expenses" (down payment + mortgage paid + principal balance) to the "return" (future value of the home). Find the total "expenses". Expenses = $ After 10 years, did you lose or gain money from selling the house? Answer: Select an answer How much (did you lose or gain)? Answer:$ Part III: 15 Year Mortgage In this part of the lab you will examine the values associated with a 15 year mortgage. You will use the same purchase price, down payment, and loan amount from Question 1. Start by confirming you have those correct values. Original purchase price (from Question 1) = $ Down Payment = $ Loan Amount $ Typically, the annual interest rate on a 15 year loan is lower than on a 30 year loan. Assume that you have found a 15 year loan with an annual interest rate of 3.64%. Express the annual interest rate as a decimal. The annual interest rate expressed as a decimal is As you did for the 30 year mortgage in Question 1, compute the monthly payment for the 15 year loan. Again, use the loan formula to find the monthly payment, d. The loan formula solved for d is: d = 1 Po W(S) - (1 + 2)-N) Hint: what value will you use for N this time? Monthly Payment = $ Assuming you make the monthly payment each month for 15 years, what will be the total amount repaid? Total payments = $ Find the total amount of interest paid over the 15 years. To do so, subtract the amount originally borrowed from the total payments. Total interest paid = $ Compare the total interest paid with this 15 year mortgage to the total interest paid with the 30 year mortgage (from Question 1). How much would you save in interest if you use the 15 year mortgage? Difference in interest paid = $ Part IV: Paying Extra While using a 15 year mortgage saves you money on interest compared to the 30 year mortgage, the monthly payment for the 15 year loan is higher than the 30 year. A good alternative is to use a 30 year loan, but to make extra payments toward the principal. This approach gives the homeowner some flexibility (you can always pay the minimum monthly payment if you can't pay the extra principal) but results in saving money on interest and paying the loan off quicker. To see the effect of making extra principal payments, you'll need some information from Question 1. Recall from Question 1, the original loan amount was $230940 and the 30 year interest rate expressed as a decimal was r = 0.0472. Recall that 30 year monthly payment from Question 1. It should have been approximately: 30 year monthly payment = $1200.52 Using this value, suppose that you pay an additional $100 a month toward principle. You will need to figure out how long it will take to pay off the loan with this additional payment. In order to do this, you would have to solve the following loan formula for N, which represents years: = 2(3-(0-1)) d + 12 (Note: Po is the original loan amount from Question 1 and here we have used k = 12 and d* is your monthly payment plus the additional $100.) In order to solve the above equation for N you would use logarithms. Using the notation log for the common logarithm, you would get the following formula: N = log 12d* (12d* -Por) (12 log(1+)) Use the above formula to figure out N, the number of years it will take to pay off the loan with the additional $100 payment. Alternatively, use an online amortization calculator such as: http://bretwhissel.net/amortization/amortize.html. You will need to enter the principal, the annual interest rate from this question, and the payment amount (your d*). Leave the "number of regular payments" blank and hit "Calculate". The number of regular payments divided by 12 should agree with N from the formula above. Find N accurate to two decimal places- don't round any more than that! Give it a try! N = Use the above formula to figure out N, the number of years it will take to pay off the loan with the additional $100 payment. Alternatively, use an online amortization calculator such as: http://bretwhissel.net/amortization/amortize.html. You will need to enter the principal, the annual interest rate from this question, and the payment amount (your d*). Leave the "number of regular payments" blank and hit "Calculate". The number of regular payments divided by 12 should agree with N from the formula above. Find N accurate to two decimal places- don't round any more than that! Give it a try! N = To find the total interest paid you need the number of payments you made (which you either have or can get from N by multiplying it by 12). You can round the number of payments to the nearest whole number. Total number of regular payments= Now you can find the total payments and the total interest paid. Don't forget to add the additional $100 to your monthly payment before multiplying by the number of payments. Total payments = $ Total interest paid: = $ Recall that the total interest paid from Question 1 was $201247.2. How much do you end up saving in interest if you pay the additional $100 per month? Save in interest = $

Expert Answer:

Related Book For

Horngrens Financial and Managerial Accounting

ISBN: 978-0133866292

5th edition

Authors: Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura

Posted Date:

Students also viewed these mathematics questions

-

For each problem, show your work steps. A correct answer with no work shown gets half credit (which means you fail the assignment). An incorrect answer with no work receives 0 credit. With time value...

-

Bloomberg Intelligence listed 50 companies to watch in 2018 (www .bloomberg.com/features/companies-to-watch-2018). Twelve of the companies are listed here with their total assets and 12-month sales....

-

Community Charities has a standing agreement with Empire State Bank. The agreement allows Community Charities to overdraw its cash balance at the bank when donations are running low. In the past,...

-

If $1000 is invested for x years at 10%, compounded continuously, the future value that results is S = 1000e 0.10x What amount will result in 5 years?

-

Refer to the statements for Google in Appendix A. For the year ended December 31, 2015, what was its debt-to-equity ratio? What does this ratio tell us? Data From Statement Google In Appendix A...

-

Large frauds can often be detected by performing financial statement analysis. Although such analysis can raise areas of concern, not all red flags are the result of fraudulent activities. Reasonable...

-

It is argued that decisions made in relatively risk-free environments are not optimal or not efficient. If this assertion is true, can we declare that the decision-making environment constrained by...

-

[10 pts] Consider a company with n > 0 workers. A worker is a famous-solo- worker if she or he is known by every other worker, but knows none of them. You are the boss and you want to check if there...

-

Recently the Legislative Council has changed the way Council minutes are prepared. Instead of noting what individual made a specific comment, the speaker is anonymized. A separate annex might...

-

How does the concept of "set points" in homeostatic regulation account for individual variation and adaptation to changing environmental conditions?

-

e...How do negative feedback loops contribute to the maintenance of homeostasis, and what molecular mechanisms underlie their regulation?

-

What advances in systems biology and computational modeling have enhanced our understanding of the complexity and robustness of homeostatic networks in biological systems ?

-

The Case of the Troubled Casino The Upper Midwest of the United States has lagged behind the economic recovery enjoyed by much of the rest of the nation. With an economy built largely on the steel,...

-

Melissa recently paid $530 for round-trip airfare to San Francisco to attend a business conference for three days. Melissa also paid the following expenses: $585 fee to register for the conference,...

-

Draw two scatterplots, one for which r = 1 and a second for which r = 21.

-

Compute ending merchandise inventory and cost of goods sold for Cambridge using the FIFO inventory costing method. The periodic inventory records of Cambridge Prosthetics indicate the following for...

-

On December 31, Peterson Company estimates that it will pay its employees a 3% bonus on $62,000 of net income after deducting the bonus. The bonus will be paid on January 15 of the next year....

-

Dearwood Properties bought three lots in a subdivision for a lump-sum price. An independent appraiser valued the lots as follows: Lot Appraised Value 1..........$ 45,000 2.......... 292,500...

-

Wagons and Wheels Ltd is a farm machinery dealership. In recent years, the company has experienced unsatisfactory profit results because of declining sales in the area. At the suggestion of the...

-

Quick Brekkie Ltd is evaluating three comparable investments. Summary data for the three investments, each of which would be paid for in current dollars, are listed below. Required Rank the three...

-

Phone Screens and Computer Screens are two divisions operated as investment centres of Siciliano Ltd. Management wants to know which of the two earned the highest return on investment for the year...

Study smarter with the SolutionInn App