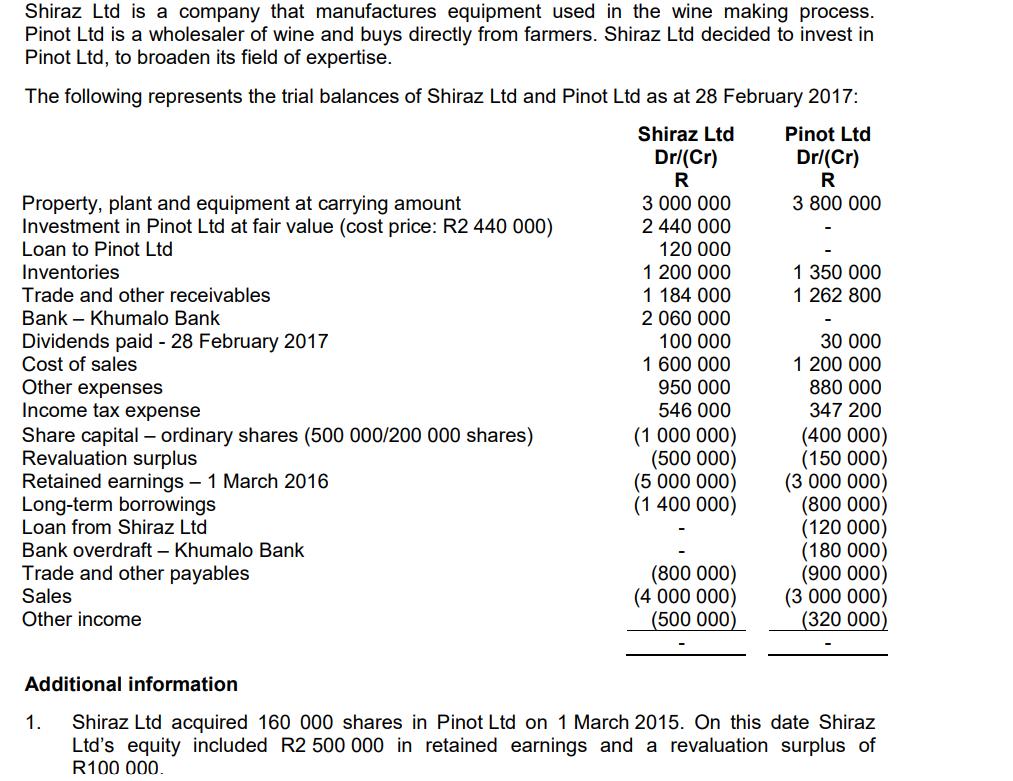

Shiraz Ltd is a company that manufactures equipment used in the wine making process. Pinot Ltd...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

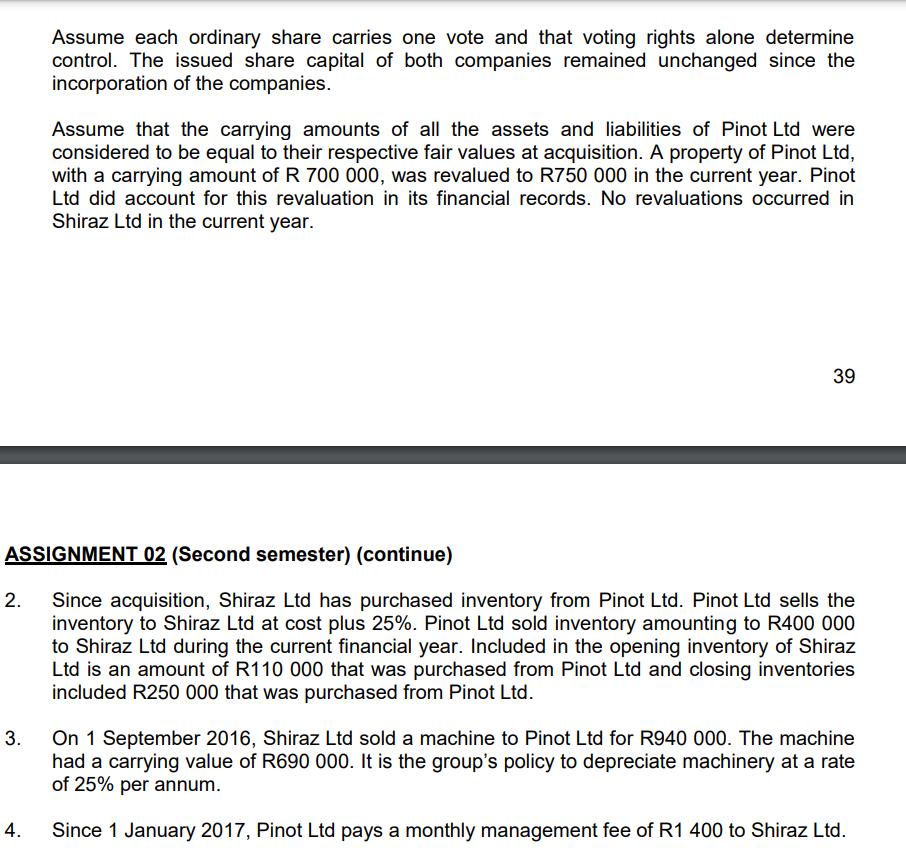

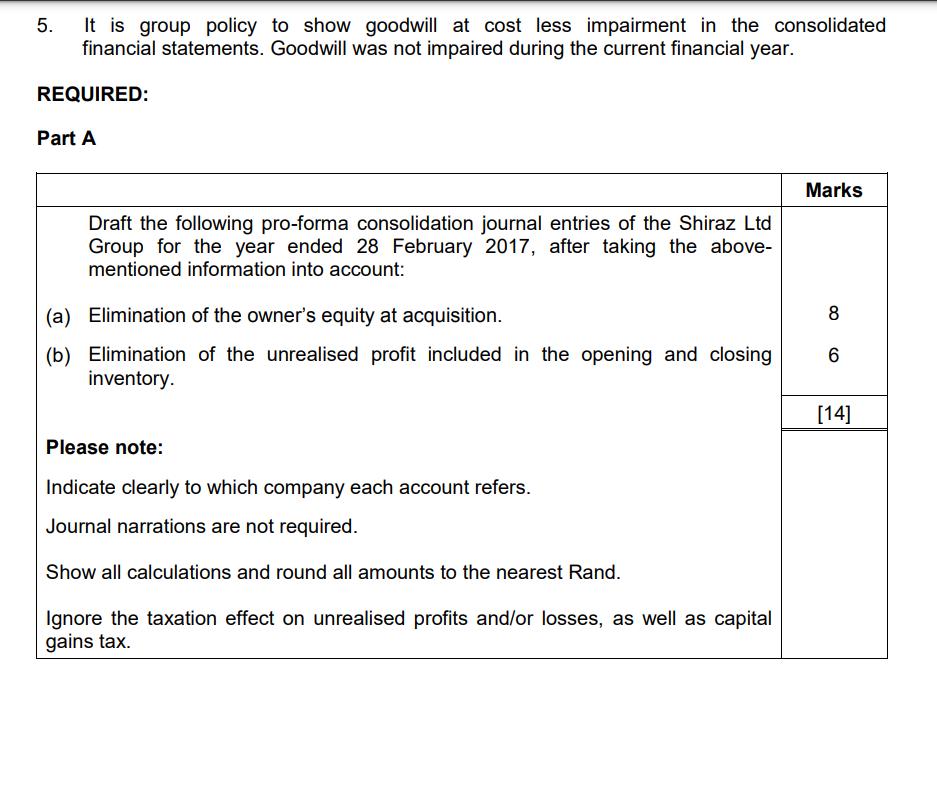

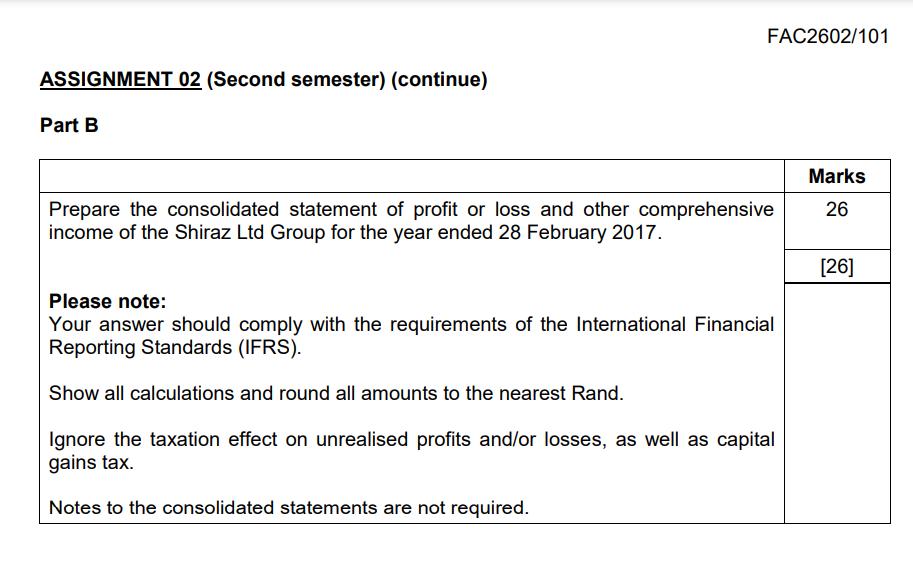

Shiraz Ltd is a company that manufactures equipment used in the wine making process. Pinot Ltd is a wholesaler of wine and buys directly from farmers. Shiraz Ltd decided to invest in Pinot Ltd, to broaden its field of expertise. The following represents the trial balances of Shiraz Ltd and Pinot Ltd as at 28 February 2017: Shiraz Ltd Dr/(Cr) R 3 000 000 2 440 000 120 000 1 200 000 1 184 000 2 060 000 100 000 1 600 000 950 000 546 000 (1 000 000) (500 000) (5 000 000) (1 400 000) Property, plant and equipment at carrying amount Investment in Pinot Ltd at fair value (cost price: R2 440 000) Loan to Pinot Ltd Inventories Trade and other receivables Bank - Khumalo Bank Dividends paid - 28 February 2017 Cost of sales Other expenses Income tax expense Share capital - ordinary shares (500 000/200 000 shares) Revaluation surplus Retained earnings - 1 March 2016 Long-term borrowings Loan from Shiraz Ltd Bank overdraft - Khumalo Bank Trade and other payables Sales Other income Additional information 1. (800 000) (4 000 000) (500 000) Pinot Ltd Dr/(Cr) R 3 800 000 1 350 000 1 262 800 30 000 1 200 000 880 000 347 200 (400 000) (150 000) (3 000 000) (800 000) (120 000) (180 000) (900 000) (3 000 000) (320 000) Shiraz Ltd acquired 160 000 shares in Pinot Ltd on 1 March 2015. On this date Shiraz Ltd's equity included R2 500 000 in retained earnings and a revaluation surplus of R100 000. 2. 3. Assume each ordinary share carries one vote and that voting rights alone determine control. The issued share capital of both companies remained unchanged since the incorporation of the companies. ASSIGNMENT 02 (Second semester) (continue) Since acquisition, Shiraz Ltd has purchased inventory from Pinot Ltd. Pinot Ltd sells the inventory to Shiraz Ltd at cost plus 25%. Pinot Ltd sold inventory amounting to R400 000 to Shiraz Ltd during the current financial year. Included in the opening inventory of Shiraz Ltd is an amount of R110 000 that was purchased from Pinot Ltd and closing inventories included R250 000 that was purchased from Pinot Ltd. 4. Assume that the carrying amounts of all the assets and liabilities of Pinot Ltd were considered to be equal to their respective fair values at acquisition. A property of Pinot Ltd, with a carrying amount of R 700 000, was revalued to R750 000 in the current year. Pinot Ltd did account for this revaluation in its financial records. No revaluations occurred in Shiraz Ltd in the current year. 39 On 1 September 2016, Shiraz Ltd sold a machine to Pinot Ltd for R940 000. The machine had a carrying value of R690 000. It is the group's policy to depreciate machinery at a rate of 25% per annum. Since 1 January 2017, Pinot Ltd pays a monthly management fee of R1 400 to Shiraz Ltd. 5. It is group policy to show goodwill at cost less impairment in the consolidated financial statements. Goodwill was not impaired during the current financial year. REQUIRED: Part A Draft the following pro-forma consolidation journal entries of the Shiraz Ltd Group for the year ended 28 February 2017, after taking the above- mentioned information into account: (a) Elimination of the owner's equity at acquisition. (b) Elimination of the unrealised profit included in the opening and closing inventory. Please note: Indicate clearly to which company each account refers. Journal narrations are not required. Show all calculations and round all amounts to the nearest Rand. Ignore the taxation effect on unrealised profits and/or losses, as well as capital gains tax. Marks 8 6 [14] ASSIGNMENT 02 (Second semester) (continue) Part B FAC2602/101 Prepare the consolidated statement of profit or loss and other comprehensive income of the Shiraz Ltd Group for the year ended 28 February 2017. Please note: Your answer should comply with the requirements of the International Financial Reporting Standards (IFRS). Show all calculations and round all amounts to the nearest Rand. Ignore the taxation effect on unrealised profits and/or losses, as well as capital gains tax. Notes to the consolidated statements are not required. Marks 26 [26] Shiraz Ltd is a company that manufactures equipment used in the wine making process. Pinot Ltd is a wholesaler of wine and buys directly from farmers. Shiraz Ltd decided to invest in Pinot Ltd, to broaden its field of expertise. The following represents the trial balances of Shiraz Ltd and Pinot Ltd as at 28 February 2017: Shiraz Ltd Dr/(Cr) R 3 000 000 2 440 000 120 000 1 200 000 1 184 000 2 060 000 100 000 1 600 000 950 000 546 000 (1 000 000) (500 000) (5 000 000) (1 400 000) Property, plant and equipment at carrying amount Investment in Pinot Ltd at fair value (cost price: R2 440 000) Loan to Pinot Ltd Inventories Trade and other receivables Bank - Khumalo Bank Dividends paid - 28 February 2017 Cost of sales Other expenses Income tax expense Share capital - ordinary shares (500 000/200 000 shares) Revaluation surplus Retained earnings - 1 March 2016 Long-term borrowings Loan from Shiraz Ltd Bank overdraft - Khumalo Bank Trade and other payables Sales Other income Additional information 1. (800 000) (4 000 000) (500 000) Pinot Ltd Dr/(Cr) R 3 800 000 1 350 000 1 262 800 30 000 1 200 000 880 000 347 200 (400 000) (150 000) (3 000 000) (800 000) (120 000) (180 000) (900 000) (3 000 000) (320 000) Shiraz Ltd acquired 160 000 shares in Pinot Ltd on 1 March 2015. On this date Shiraz Ltd's equity included R2 500 000 in retained earnings and a revaluation surplus of R100 000. 2. 3. Assume each ordinary share carries one vote and that voting rights alone determine control. The issued share capital of both companies remained unchanged since the incorporation of the companies. ASSIGNMENT 02 (Second semester) (continue) Since acquisition, Shiraz Ltd has purchased inventory from Pinot Ltd. Pinot Ltd sells the inventory to Shiraz Ltd at cost plus 25%. Pinot Ltd sold inventory amounting to R400 000 to Shiraz Ltd during the current financial year. Included in the opening inventory of Shiraz Ltd is an amount of R110 000 that was purchased from Pinot Ltd and closing inventories included R250 000 that was purchased from Pinot Ltd. 4. Assume that the carrying amounts of all the assets and liabilities of Pinot Ltd were considered to be equal to their respective fair values at acquisition. A property of Pinot Ltd, with a carrying amount of R 700 000, was revalued to R750 000 in the current year. Pinot Ltd did account for this revaluation in its financial records. No revaluations occurred in Shiraz Ltd in the current year. 39 On 1 September 2016, Shiraz Ltd sold a machine to Pinot Ltd for R940 000. The machine had a carrying value of R690 000. It is the group's policy to depreciate machinery at a rate of 25% per annum. Since 1 January 2017, Pinot Ltd pays a monthly management fee of R1 400 to Shiraz Ltd. 5. It is group policy to show goodwill at cost less impairment in the consolidated financial statements. Goodwill was not impaired during the current financial year. REQUIRED: Part A Draft the following pro-forma consolidation journal entries of the Shiraz Ltd Group for the year ended 28 February 2017, after taking the above- mentioned information into account: (a) Elimination of the owner's equity at acquisition. (b) Elimination of the unrealised profit included in the opening and closing inventory. Please note: Indicate clearly to which company each account refers. Journal narrations are not required. Show all calculations and round all amounts to the nearest Rand. Ignore the taxation effect on unrealised profits and/or losses, as well as capital gains tax. Marks 8 6 [14] ASSIGNMENT 02 (Second semester) (continue) Part B FAC2602/101 Prepare the consolidated statement of profit or loss and other comprehensive income of the Shiraz Ltd Group for the year ended 28 February 2017. Please note: Your answer should comply with the requirements of the International Financial Reporting Standards (IFRS). Show all calculations and round all amounts to the nearest Rand. Ignore the taxation effect on unrealised profits and/or losses, as well as capital gains tax. Notes to the consolidated statements are not required. Marks 26 [26]

Expert Answer:

Answer rating: 100% (QA)

Part a Elimination of owners equity at acquisition Debit Share Capital Pinot Ltd R400000 Debit Retained earnings Pinot Ltd R 2500000 Debit Revaluation ... View the full answer

Related Book For

Applying International Financial Reporting Standards

ISBN: 978-0730302124

3rd edition

Authors: Keith Alfredson, Ken Leo, Ruth Picker, Paul Pacter, Jennie Radford Victoria Wise

Posted Date:

Students also viewed these accounting questions

-

Techmed Ltd is a company that manufactures and sells medical equipment to hospitals and has a 31 March year-end. Due to a demand for magnetic resonance imaging (MRI) scanners and computed tomography...

-

A company that manufactures recreational pedal boats has approached Mike Cichanowski to ask if he would be interested in using Current Designs rotomold expertise and equipment to produce some of the...

-

A company that manufactures air-operated drain valve assemblies budgeted $74,000 per year to pay for plastic components over a 5-year period. If the company spent only $42,000 in year 1, what uniform...

-

Explain how to determine the maximum or minimum value of a quadratic function.

-

Adria Lopez expects second quarter 2014 sales of her new line of computer furniture to be the same as the first quarters sales (reported below) without any changes in strategy. Monthly sales averaged...

-

If q(x) is an arbitrary polynomial in Pn' it follows from Exercise 60(b) that q (x) = c0p0(x) + . . . + cnpn(x).....................(1) for some scalars c0, . . . , cn. (a) Show that ci = q (ai) for...

-

At December 31, 2017, Eric Corporation had two notes payable outstanding (notes 1 and 2). At December 31, 2018, Eric also had two notes payable outstanding (notes 3 and 4). These notes are described...

-

Bakery Products, Inc., is divided into five departments, Mixing, Blending, Finishing, Factory Office, and Building Maintenance. The first three departments are engaged in production work. Factory...

-

Pilot projects require _ _ _ _ _ _ _ _ in order for employees to understand how the practices in a pilot project apply to them even though they are in a completely different functional area. Question...

-

The data for the number employed at several famous IT companies is maintained in the COMPANY table. Write a query to print the /Ds of the companies that have more than 10000 employees, in ascending...

-

8. List at least 3 advantages and 3 disadvantages of a corporation.

-

The following summary transactions occurred during the year for Marigold. Cash received from: Collections from customers $400,000 Interest on notes receivable 16,000 Collection of notes receivable...

-

Calculating financial ratios: Using the financial statements provided and the material you have studied, calculate the following financial ratios (ratios). Be sure to detail the procedure and result...

-

Read this article " 'Peloton to Stop Making Bikes Itself " do additional research and respond to these questions: What does Peloton make? What is their Business Strategy? Why did demand boom during...

-

For example, many employers have tuition reimbursement programs and the first 5,250 of any ER-paid tuition is excluded from taxable income. However, any amount paid by the employer in excess of 5,250...

-

On July 1, 2023, Crane Corp., which uses IFRS, signs a 4-year, non-cancellable lease agreement to lease a equipment from Blossom Ltd. The following information concerns the lease agreement. 1. The...

-

By default, it is not possible to multiply a single value by an int16 value. Write a function that accepts a single argument and an int16 argument and multiplies them together, returning the...

-

In a system with light damping (c < cc), the period of vibration is commonly defined as the time interval d = 2/d corresponding to two successive points where the displacement-time curve touches one...

-

What is the main principle of tax-effect accounting as outlined in IAS 12?

-

Does the separate identification of profit and other components of comprehensive income provide a meaningful distinction between the effects of different types of non-owner transactions and events?

-

What is the difference between the first-in, first-out method and the weighted average method of assigning cost?

-

Show how Figure 14-8 could be modified to use a temperature swing instead of a pressure swing. What might be advantages and disadvantages of doing this? Solid Bed PH Turbo- expander PL SCF Compressor...

-

The simulated countercurrent process for leaching is shown in Figure 14-6. Convert this figure to the appropriate nomenclature for washing. BI 0 Step N F A Extract Solvent 2 Load E D 1. Dump Step N +...

-

Would you expect stage efficiencies to be higher or lower in leaching than in supercritical extraction? Explain.

Study smarter with the SolutionInn App