Stephen Goode, chief financial officer of F. Mayer Imports Pty. Ltd. (F. Mayer), was just about...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

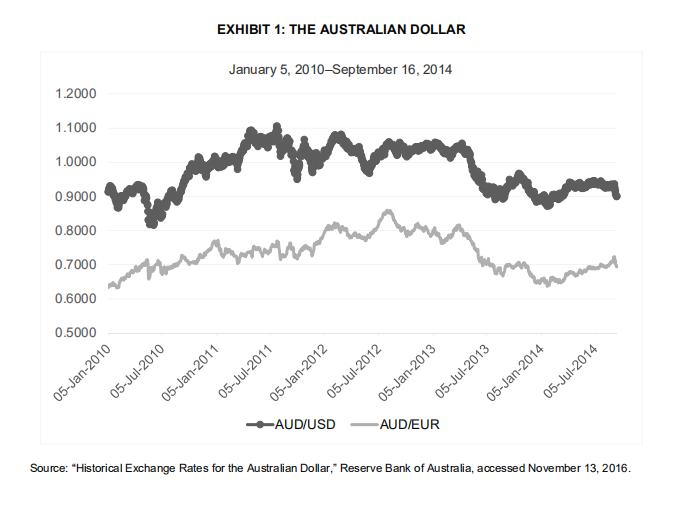

Stephen Goode, chief financial officer of F. Mayer Imports Pty. Ltd. (F. Mayer), was just about to leave his office on the night of September 16, 2014, when he heard the ping of an incoming e-mail. It was a proposal from his relationship bank in response to his request for foreign exchange hedging alternatives. With imports like Lurpak butter, Callebaut chocolate, and the widest range of European cheese in Australia, F. Mayer had around €70 million¹ worth of product procurement annually. The Australian dollar (AUD) had been losing its strength against the euro (EUR) over the last 18 months and had dropped from a high of AU$0.7027 in October 2013 to a low of AU$0.6369 in January 2014 as it struggled to return to its previous glorious days. With the AUD to EUR exchange (AUD/EUR) recently rebounding and edging back toward the company's annual wholesale budget rate of AUD/EUR 0.6900, Goode had a narrow window of opportunity to potentially protect his profit margins for the rest of that, and the following, financial year. He needed to decide if he should hedge and, if so, which hedging strategy to use to get the best possible outcome. COMPANY BACKGROUND F. Mayer a second-generation private family business in Australia-specialized in importing high-end European gourmet food products for distribution in the Australian markets. Starting out of a Darling Point flat, the company was established by the late Fred Mayer in 1957, initially importing Norwegian knitted pullover sweaters and ski wear. By 2014, the company offered the most extensive range of food delicacies and specialty products in Australia. Over 1,000 top-quality fine food products were distributed nationally on a daily basis to restaurants, supermarkets, wholesalers, hotels, resorts, delicatessens, private food outlets, manufacturers, shipping providers, and airline caterers. Among many well-known products, F. Mayer provided San Pellegrino sparkling water, Lurpak butter, Castello cheese, Il Pescatore smoked salmon, and Barilla pasta. Despite the global financial crisis in 2008, the company had been growing over the previous seven years at an average compound annual growth rate of more than 15 per cent. This reflected the growth in the sophistication of Australian taste buds and the continuous increase in food consumption. Profit margins were also enhanced due to a two-year sustained period of a strong AUD at between AUD/EUR 0.70 and 0.80 (see Exhibit 1). "FOODIE" CULTURE Dining out and appreciating higher-quality food had become part of Australian culture. Data from the Australian Bureau of Statistics indicated that household spending on dining out had increased by more than 55 per cent in real terms from 1984 to 2010. In terms of proportion, households were allocating about one- third of their weekly food budget to eating out in 2010 versus one-fifth in 1984. When not dining out, Australian households focused on creating their own gourmet three-course meals at home. The food industry overall had benefited from a rising "foodie" culture through the popularity of cooking shows such as Master Chef and My Kitchen Rules. Technology also played its part in enabling the use of many online directories and reviews of cooking recipes, and fashionable restaurants, cafes, and bars, which further propelled Australians' awareness of quality dining experiences and the trend toward high-quality gourmet food. The continuous demand by Australians for high-quality gourmet food was established. WHOLESALE MARKET STRUCTURE Competition in the food wholesaling industry, while moderate, was on an increasing trend. Downstream buyers focused on achieving the lowest possible price for a given product or brand in order to maximize their own profit margins. Large supermarket giants such as Coles Supermarkets and Woolworths Supermarkets exercised their significant bargaining power to keep prices fixed and low, passing on all pricing risks to wholesalers. As a result, aside from unique product offerings and ease of dealing, wholesale prices had become a major point of competition among wholesalers. Margin management was a key success factor for the wholesaling business. Wholesale prices for each imported food product were calculated and set based on an annual budgeted foreign exchange rate that reflected the wholesaler's view of the exchange rate for the year and would provide the wholesaler a minimum acceptable profit margin for the year. Depending on the buyer's bargaining power and trading relationships, the wholesaler would separately negotiate a fixed premium or discount on the set wholesale prices with the aim of achieving overall larger-than-budgeted profit margins for the company for the year. Any renegotiation of wholesale prices to large buyers, would take more than four months and substantial management time from both the buyer and seller to complete. The disruption often jeopardized the trading relationship. Therefore, renegotiations were kept to a minimum. Although the foreign exchange risk lay with the importer, this arrangement allowed the importer to benefit from any favourable foreign exchange movement. As a result, for import wholesalers such as F. Mayer, it was paramount to be able to set a competitive budget foreign exchange rate, but to purchase at a favourable foreign exchange rate. That allowed wholesalers not only to achieve higher-than-budgeted profit margins, but also to improve their competitive advantage in the market. As a result, the budget foreign currency rate was a key factor influencing wholesale prices and the company's competitive advantage. CURRENT HEDGING PRACTICE With the strong AUD of the previous four years, most importers in 2014 left their foreign currency exposure unhedged to reap the extra profit margin gains from the differential between the actual and budget exchange rates. If they could purchase imports with a stronger AUD than the budget exchange rate, the gain enhanced the gross margin and flowed directly to the bottom line. With the growth in import volumes from Europe, F. Mayer's euro risk exposures had also dramatically increased to over €70 million annually. In view of the increased risk, F. Mayer started using vanilla forward contracts foreign exchange contracts in 2011 to manage its euro exchange risk. However, there was no formal hedging policy in place and the decisions on when to hedge, how long to hedge, and how much to hedge were made daily by Goode and the business owner, based on their view of the AUD/EUR market and upcoming euro requirements. When they felt that the AUD/EUR was at its top end before retreating, they would buy some foreign exchange contracts of one-to-three-months' duration. Often, the AUD/EUR rose further after they hedged and, therefore, they felt that hedging was trimming off their profit margins rather than adding any value. On average, about 30-40 per cent of their total exposure had been hedged over the years through this sporadic hedging practice. Nonetheless, with the AUD/EUR consistently trading at over 0.7000 and as high as 0.8000 between 2010 and 2013, this sporadic hedging practice had resulted in higher-than-budget rates and higher profit margins throughout these years. GLOBAL FINANCIAL MARKETS The world's major central banks seemed to be divided on their major policy. Economists believed that by June 2015, the United States Federal Reserve could raise interest rates for the first time in nearly seven years; the U.S. unemployment rate was forecasted to be below 6 per cent and the inflation rate was edging closer to 2 per cent. On the other hand, the European Central Bank and the Bank of Japan were trying hard to battle recession with more monetary stimuli. This divergence in monetary policy between the world's major central banks could have major implications for global markets, which had already substantially increased in market risks. It was believed that the U.S. dollar would strengthen significantly against the euro and the yen. EUROPEAN CENTRAL BANK AND RISKS WITHIN EUROPE On September 4, 2014, the European Central Bank further reduced its benchmark interest rate by 10 basis points to a fresh record low of 0.05 per cent, and announced an asset-backed securities purchase program in the hope of unblocking lending and fighting deflation in the Eurozone. Mario Draghi, the president of the European Central Bank, expressed his concerns about Europe's economic situation in a press conference in Frankfurt: "Most, if not all, the data we got in August on gross domestic product and inflation showed that the recovery was losing momentum."² A lower AUD seemed to be the new norm. On September 15, 2014, the AUD was on the verge of slipping below US $0.90, with September producing the sharpest running decline since mid-2013. Warren Hogan, chief economist of Australia and New Zealand Banking Group (ANZ), commented in the Australian Financial Review on September 15, 2014, "The Australian dollar is moving in the right direction and it is getting back to a level we think is appropriate, which is in the mid to high US$0.80." Westpac senior currency strategist Sean Callow said to The Sydney Morning Herald on September 15, 2014, that "[i]t has been a real shock to lose 3¢ in a week." He added that until there was a reversal in commodity price weakness, the AUD "may not bounce." A lower AUD was welcomed by the Reserve Bank of Australia, as it hoped to stimulate broader economic activity and to help the export sectors, which had been impacted by the high currency. THE DECISION F. Mayer's budget rate for 2014 was AUD/EUR 0.6900. For the previous 12 months, the AUD/EUR had been trading at well below the 0.6900 range, which was starting to hurt F. Mayer's bottom line. If the AUD/EUR was to continue at a sub-budget 0.6900 level, the company would need to commence the renegotiation of a new wholesale price or risk further erosion in margins. However, a commencement of renegotiation might trigger many unwanted consequences, such as jeopardizing trading relationships and spreading market rumours about the company's lack of integrity in keeping wholesale prices, thus giving competitors the opportunity to disrupt and outprice. In the world of import competition, those with the lowest cost of imports had the competitive advantage of outpricing their peers. They therefore enjoyed the benefits of building new client relationships and cementing existing relationships. Thus, every percentage point advantage that F. Mayer could gain from the AUD/EUR would translate into profit margins and, of course, more market power to drive further sales. While the current hedging strategy had served the company well for the previous three years in a strong AUD environment, how would the company be affected if the AUD/EUR did not rebound above 0.7000? Or what if F. Mayer hedged at the current sub-0.6900 level and the AUD/EUR rebounded to over 0.7000 for the rest of the year? The company would lose all the margins and the ability to outprice competitors. Goode was wondering what to do in these potentially different global market conditions. Should he leave his euro procurement unhedged, given the worsening economic conditions in Europe? Should he hedge some or all of his exposure, using vanilla foreign exchange forward contracts? Or should he use other hedging strategies, which might provide him with the option to participate in the upside? Should he wait until the AUD/EUR rebounded higher, and opportunistically hedge with one-to-three-month forward exchange contracts like before? The currency screen was showing the AUD/EUR ticking at 0.6950 as Goode reviewed the relationship bank's e-mail proposal (see Exhibit 3). 1.2000 1.1000 1.0000 0.9000 0.8000 0.7000 0.6000 0.5000 05-Jan-2010 05-Jul-2010 EXHIBIT 1: THE AUSTRALIAN DOLLAR January 5, 2010-September 16, 2014 05-Jan-2011 05-Jul-2011 05-Jan-2012 05-Jul-2012 L -AUD/USD 05-Jan-2013 -AUD/EUR 05-Jul-2013 05-Jan-2014 mmi 05-Jul-2014 Source: "Historical Exchange Rates for the Australian Dollar," Reserve Bank of Australia, accessed November 13, 2016. EXHIBIT 2: MEDIA RELEASE Statement by Glenn Stevens, Governor, Reserve Bank of Australia: Monetary Policy Decision Number: 2014-15 Date: September 2, 2014 At its meeting today, the Board decided to leave the cash rate unchanged at 2.5 per cent. Growth in the global economy is continuing at a moderate pace. China's growth remains generally in line with policymakers' objectives, with weakening property markets a challenge in the near term. Commodity prices in historical terms remain high, but some of those important to Australia have declined this year. Financial conditions overall remain very accommodative. Long-term interest rates and risk spreads remain very low. Volatility in many financial prices is currently unusually low. Markets appear to be attaching a very low probability to any rise in global interest rates or other adverse event over the period ahead. In Australia, the most recent survey data indicate gradually improving business conditions and some recovery in household sentiment after a weaker period around mid year, suggesting moderate growth in the economy is occurring. Resources sector investment spending is starting to decline significantly. Investment intentions in some other sectors continue to improve, though these areas of capital spending are expected to see only moderate growth in the near term. Public spending is scheduled to be subdued. Overall, the Bank still expects growth to be a little below trend over the year ahead. The recorded rate of unemployment has increased recently, despite some improvement in most other indicators for the labour market this year. The Bank's assessment remains that the labour market has a degree of spare capacity and that it will probably be some time yet before unemployment declines consistently. Growth in wages has declined noticeably and is expected to remain relatively modest over the period ahead, which should keep inflation consistent with the target even with lower levels of the exchange rate. Monetary policy remains accommodative. Interest rates are very low and have continued to edge lower over recent months as competition to lend has increased. Investors continue to look for higher returns in response to low rates on safe instruments. Credit growth has picked up a little, including most recently to businesses. The increase in dwelling prices continues. The exchange rate, on the other hand, remains above most estimates of its fundamental value, particularly given the declines in key commodity prices. It is offering less assistance than would normally be expected in achieving balanced growth in the economy. Looking ahead, continued accommodative monetary policy should provide support to demand and help growth to strengthen over time. Inflation is expected to be consistent with the 2-3 per cent target over the next two years. In the Board's judgement, monetary policy is appropriately configured to foster sustainable growth in demand and inflation outcomes consistent with the target. On present indications, the most prudent course is likely to be a period of stability in interest rates. Source: Reserve Bank of Australia, "Statement by Glenn Stevens, Govemor: Monetary Policy Decision," press release, September 2, 2014, accessed February 22, 2017, www.rba.gov.au/media-releases/2014/mr-14-15.html. September 16, 2014 Hi Mr. Goode, On your request, please see the following indicative pricing on some AUD/EUR FX hedging solutions: All pricing is indicative and based off spot AUD/EUR 0.6980. The four (4) month FEC (Foreign Exchange Forward contract) is 0.6910 (spot of 0.6980 less 70 forward points). Solution 1-Purchase an AUD Put/EUR Call Option Expiry Date: Value Date: 2015-01-14 (four months) 2015-01-16 Strike 1:0.6910 (at-the-money fwd) Strike 2:0.6860 (50 pips out-of-the-money (OTM)) Premium 1 Premium 2: This solution gives you the right but not the obligation to buy EUR and sell AUD at the strike rate on the expiry date. On the expiry date, if the prevailing spot AUD/EUR is below the strike rate, then you will exercise the right to deal at the higher strike rate. Conversely, if the prevailing spot AUD/EUR rate is higher than the strike rate, then you will let the option lapse and buy EUR against the AUD in the spot market at the higher rate. I have provided you with two prices so you can see the relationship between premium and strike prices. 2.13% of AUD face value (~146 AUD/EUR pips) 1.81% of AUD face value (~124 AUD/EUR pips) Solution 2-AUD/EUR Collar Option-Buy an AUD Put/EUR Call and Sell an AUD Call/EUR Put-Zero Premium Expiry Date: Value Date: B Put Strike: S Call Strike: B Put Strike: S Call Strike: 2015-01-14 (four months) 2015-01-16 0.6860 (50 pips below the FEC) 0.6942 0.6810 (100 pips below the FEC) 0.6983 This solution locks you into a range whereby you have a worst-case rate (bought put strike) and the capacity to participate in favourable AUD/EUR movements up to the sold call strike. Ideally, the worst-case rate would be your budget rate. I have provided you with indicative pricing on two collar structures so that you can compare two different ranges. Remember, a collar structure is an alternative to an FEC; therefore, when assessing participation benefits, use the FEC rate as the benchmark, not the spot rate. Solution 3-AUD/EUR Knock-In Forward-Buy an AUD Put/EUR Call and Sell an AUD Call/EUR Put with Up-and-In Trigger-Zero Premium Expiry Date: 2015-01-14 (four months) Value Date: 2015-01-16 B Put Strike: S Call Strike: 0.6890 (20 pips below the FEC) 0.6890 with up-and-in knock-in trigger at 0.7140 With this structure, your worst-case rate is 0.6890 (20 pips below the FEC). When the option starts, you only have a bought AUD put option with a strike of 0.6890. However, if 0.7140 trades at any time between the option start and expiry date, then you are "knocked in" to a sold AUD call option with a strike of 0.6890. Having a bought AUD put and sold AUD call option with the same strike creates a synthetic forward. So, in layman's terms, this structure gives you a worst-case rate that is 20 pips worse than the FEC; however, you have the opportunity to participate in the AUD/EUR all the way to the trigger rate of 0.7140. If 0.7140 does trade during the life of the option, then you have to deal at the common strike rate of 0.6890. Source: Company documents. F. Mayer Imports: Hedging Foreign Currency Risk Due by 5/16 10pm F. Mayer Imports is an Australian wholesale food importer that imports high-end European gourmet food products for distribution in the Australian retail food markets (e.g., food supermarkets). Given the high volatility of the Australian Dollar Euro exchange rate (A$/€), F. Mayer's profit margins, competitive position, and market share are heavily affected by the difference in its target A$/ € exchange rate and the actual A$/ € exchange rate. F. Mayer estimates its wholesale prices for imported food products using an annual budget (target) A$/€ exchange rate based on its forecasts of European, Australian, and global economic and financial market conditions. The target A$/€ exchange rate protects F. Mayer's profit margin and its negotiated prices to retail food markets. The firm keeps any renegotiations of food prices with supermarkets to a minimum in case of an A$ depreciation against Euro to preserve its trading relations and market share. Since the A$/ € currency exchange rate risk is largely borne by F. Mayer, the firm must set a competitive budget A$/€ exchange rate to achieve higher-than- budgeted profit margin and improve its competitive market advantage. This task has become crucial in year 2014 as the AS has depreciated significantly against Euro from A$0.7027 in October 2013 to A$0.6369 in January 2014 (i.e., from A$1-€0.7027 to A$1-€0.6369). F. Mayer budget (target) A$/€ exchange rate for 2014 is A$0.6900 (A$1-€0.6900) and its 2014 total procurement commitment (currency exposure) is around €70 million. Obviously, F. Mayer does not have any bargaining power to negotiate its own A$/ € forward rate, so it has to accept quoted market forward rates as given. Also, F. Mayer has no in-house expertise to forecast the correct direction of possible future A$/€ exchange rate. F. Mayer must decide whether it should hedge its €70 million procurement commitment and, if yes, which of the four hedging strategies will protect its target A$0.6900 exchange rate and may also provide it a better-than-budgeted AS/€ exchange rate for 2014 (i.e., where it pays fewer A$ to buy €70 million than at A$0.6900). You should be to able to answer the above hedging questions if your case analysis addresses the following issues: 1. How effective is F. Mayer's current practice of having no established hedging program (or sporadic short-term hedging using 1-3 months contract in a strong AS environment)? The current practice may have elements of speculation than hedging as the firm makes a judgment call on the direction of A$/ € exchange rate when A$ has gained against Euro. 2. How large is F. Mayer's 2014 currency risk exposure (size of potential losses in A$) for its €70 million procurement commitment if the A$/€ exchange rate during 2014 is as volatile as during the previous 12 months (see Exhibit 1)? Stephen Goode, chief financial officer of F. Mayer Imports Pty. Ltd. (F. Mayer), was just about to leave his office on the night of September 16, 2014, when he heard the ping of an incoming e-mail. It was a proposal from his relationship bank in response to his request for foreign exchange hedging alternatives. With imports like Lurpak butter, Callebaut chocolate, and the widest range of European cheese in Australia, F. Mayer had around €70 million¹ worth of product procurement annually. The Australian dollar (AUD) had been losing its strength against the euro (EUR) over the last 18 months and had dropped from a high of AU$0.7027 in October 2013 to a low of AU$0.6369 in January 2014 as it struggled to return to its previous glorious days. With the AUD to EUR exchange (AUD/EUR) recently rebounding and edging back toward the company's annual wholesale budget rate of AUD/EUR 0.6900, Goode had a narrow window of opportunity to potentially protect his profit margins for the rest of that, and the following, financial year. He needed to decide if he should hedge and, if so, which hedging strategy to use to get the best possible outcome. COMPANY BACKGROUND F. Mayer a second-generation private family business in Australia-specialized in importing high-end European gourmet food products for distribution in the Australian markets. Starting out of a Darling Point flat, the company was established by the late Fred Mayer in 1957, initially importing Norwegian knitted pullover sweaters and ski wear. By 2014, the company offered the most extensive range of food delicacies and specialty products in Australia. Over 1,000 top-quality fine food products were distributed nationally on a daily basis to restaurants, supermarkets, wholesalers, hotels, resorts, delicatessens, private food outlets, manufacturers, shipping providers, and airline caterers. Among many well-known products, F. Mayer provided San Pellegrino sparkling water, Lurpak butter, Castello cheese, Il Pescatore smoked salmon, and Barilla pasta. Despite the global financial crisis in 2008, the company had been growing over the previous seven years at an average compound annual growth rate of more than 15 per cent. This reflected the growth in the sophistication of Australian taste buds and the continuous increase in food consumption. Profit margins were also enhanced due to a two-year sustained period of a strong AUD at between AUD/EUR 0.70 and 0.80 (see Exhibit 1). "FOODIE" CULTURE Dining out and appreciating higher-quality food had become part of Australian culture. Data from the Australian Bureau of Statistics indicated that household spending on dining out had increased by more than 55 per cent in real terms from 1984 to 2010. In terms of proportion, households were allocating about one- third of their weekly food budget to eating out in 2010 versus one-fifth in 1984. When not dining out, Australian households focused on creating their own gourmet three-course meals at home. The food industry overall had benefited from a rising "foodie" culture through the popularity of cooking shows such as Master Chef and My Kitchen Rules. Technology also played its part in enabling the use of many online directories and reviews of cooking recipes, and fashionable restaurants, cafes, and bars, which further propelled Australians' awareness of quality dining experiences and the trend toward high-quality gourmet food. The continuous demand by Australians for high-quality gourmet food was established. WHOLESALE MARKET STRUCTURE Competition in the food wholesaling industry, while moderate, was on an increasing trend. Downstream buyers focused on achieving the lowest possible price for a given product or brand in order to maximize their own profit margins. Large supermarket giants such as Coles Supermarkets and Woolworths Supermarkets exercised their significant bargaining power to keep prices fixed and low, passing on all pricing risks to wholesalers. As a result, aside from unique product offerings and ease of dealing, wholesale prices had become a major point of competition among wholesalers. Margin management was a key success factor for the wholesaling business. Wholesale prices for each imported food product were calculated and set based on an annual budgeted foreign exchange rate that reflected the wholesaler's view of the exchange rate for the year and would provide the wholesaler a minimum acceptable profit margin for the year. Depending on the buyer's bargaining power and trading relationships, the wholesaler would separately negotiate a fixed premium or discount on the set wholesale prices with the aim of achieving overall larger-than-budgeted profit margins for the company for the year. Any renegotiation of wholesale prices to large buyers, would take more than four months and substantial management time from both the buyer and seller to complete. The disruption often jeopardized the trading relationship. Therefore, renegotiations were kept to a minimum. Although the foreign exchange risk lay with the importer, this arrangement allowed the importer to benefit from any favourable foreign exchange movement. As a result, for import wholesalers such as F. Mayer, it was paramount to be able to set a competitive budget foreign exchange rate, but to purchase at a favourable foreign exchange rate. That allowed wholesalers not only to achieve higher-than-budgeted profit margins, but also to improve their competitive advantage in the market. As a result, the budget foreign currency rate was a key factor influencing wholesale prices and the company's competitive advantage. CURRENT HEDGING PRACTICE With the strong AUD of the previous four years, most importers in 2014 left their foreign currency exposure unhedged to reap the extra profit margin gains from the differential between the actual and budget exchange rates. If they could purchase imports with a stronger AUD than the budget exchange rate, the gain enhanced the gross margin and flowed directly to the bottom line. With the growth in import volumes from Europe, F. Mayer's euro risk exposures had also dramatically increased to over €70 million annually. In view of the increased risk, F. Mayer started using vanilla forward contracts foreign exchange contracts in 2011 to manage its euro exchange risk. However, there was no formal hedging policy in place and the decisions on when to hedge, how long to hedge, and how much to hedge were made daily by Goode and the business owner, based on their view of the AUD/EUR market and upcoming euro requirements. When they felt that the AUD/EUR was at its top end before retreating, they would buy some foreign exchange contracts of one-to-three-months' duration. Often, the AUD/EUR rose further after they hedged and, therefore, they felt that hedging was trimming off their profit margins rather than adding any value. On average, about 30-40 per cent of their total exposure had been hedged over the years through this sporadic hedging practice. Nonetheless, with the AUD/EUR consistently trading at over 0.7000 and as high as 0.8000 between 2010 and 2013, this sporadic hedging practice had resulted in higher-than-budget rates and higher profit margins throughout these years. GLOBAL FINANCIAL MARKETS The world's major central banks seemed to be divided on their major policy. Economists believed that by June 2015, the United States Federal Reserve could raise interest rates for the first time in nearly seven years; the U.S. unemployment rate was forecasted to be below 6 per cent and the inflation rate was edging closer to 2 per cent. On the other hand, the European Central Bank and the Bank of Japan were trying hard to battle recession with more monetary stimuli. This divergence in monetary policy between the world's major central banks could have major implications for global markets, which had already substantially increased in market risks. It was believed that the U.S. dollar would strengthen significantly against the euro and the yen. EUROPEAN CENTRAL BANK AND RISKS WITHIN EUROPE On September 4, 2014, the European Central Bank further reduced its benchmark interest rate by 10 basis points to a fresh record low of 0.05 per cent, and announced an asset-backed securities purchase program in the hope of unblocking lending and fighting deflation in the Eurozone. Mario Draghi, the president of the European Central Bank, expressed his concerns about Europe's economic situation in a press conference in Frankfurt: "Most, if not all, the data we got in August on gross domestic product and inflation showed that the recovery was losing momentum."² A lower AUD seemed to be the new norm. On September 15, 2014, the AUD was on the verge of slipping below US $0.90, with September producing the sharpest running decline since mid-2013. Warren Hogan, chief economist of Australia and New Zealand Banking Group (ANZ), commented in the Australian Financial Review on September 15, 2014, "The Australian dollar is moving in the right direction and it is getting back to a level we think is appropriate, which is in the mid to high US$0.80." Westpac senior currency strategist Sean Callow said to The Sydney Morning Herald on September 15, 2014, that "[i]t has been a real shock to lose 3¢ in a week." He added that until there was a reversal in commodity price weakness, the AUD "may not bounce." A lower AUD was welcomed by the Reserve Bank of Australia, as it hoped to stimulate broader economic activity and to help the export sectors, which had been impacted by the high currency. THE DECISION F. Mayer's budget rate for 2014 was AUD/EUR 0.6900. For the previous 12 months, the AUD/EUR had been trading at well below the 0.6900 range, which was starting to hurt F. Mayer's bottom line. If the AUD/EUR was to continue at a sub-budget 0.6900 level, the company would need to commence the renegotiation of a new wholesale price or risk further erosion in margins. However, a commencement of renegotiation might trigger many unwanted consequences, such as jeopardizing trading relationships and spreading market rumours about the company's lack of integrity in keeping wholesale prices, thus giving competitors the opportunity to disrupt and outprice. In the world of import competition, those with the lowest cost of imports had the competitive advantage of outpricing their peers. They therefore enjoyed the benefits of building new client relationships and cementing existing relationships. Thus, every percentage point advantage that F. Mayer could gain from the AUD/EUR would translate into profit margins and, of course, more market power to drive further sales. While the current hedging strategy had served the company well for the previous three years in a strong AUD environment, how would the company be affected if the AUD/EUR did not rebound above 0.7000? Or what if F. Mayer hedged at the current sub-0.6900 level and the AUD/EUR rebounded to over 0.7000 for the rest of the year? The company would lose all the margins and the ability to outprice competitors. Goode was wondering what to do in these potentially different global market conditions. Should he leave his euro procurement unhedged, given the worsening economic conditions in Europe? Should he hedge some or all of his exposure, using vanilla foreign exchange forward contracts? Or should he use other hedging strategies, which might provide him with the option to participate in the upside? Should he wait until the AUD/EUR rebounded higher, and opportunistically hedge with one-to-three-month forward exchange contracts like before? The currency screen was showing the AUD/EUR ticking at 0.6950 as Goode reviewed the relationship bank's e-mail proposal (see Exhibit 3). 1.2000 1.1000 1.0000 0.9000 0.8000 0.7000 0.6000 0.5000 05-Jan-2010 05-Jul-2010 EXHIBIT 1: THE AUSTRALIAN DOLLAR January 5, 2010-September 16, 2014 05-Jan-2011 05-Jul-2011 05-Jan-2012 05-Jul-2012 L -AUD/USD 05-Jan-2013 -AUD/EUR 05-Jul-2013 05-Jan-2014 mmi 05-Jul-2014 Source: "Historical Exchange Rates for the Australian Dollar," Reserve Bank of Australia, accessed November 13, 2016. EXHIBIT 2: MEDIA RELEASE Statement by Glenn Stevens, Governor, Reserve Bank of Australia: Monetary Policy Decision Number: 2014-15 Date: September 2, 2014 At its meeting today, the Board decided to leave the cash rate unchanged at 2.5 per cent. Growth in the global economy is continuing at a moderate pace. China's growth remains generally in line with policymakers' objectives, with weakening property markets a challenge in the near term. Commodity prices in historical terms remain high, but some of those important to Australia have declined this year. Financial conditions overall remain very accommodative. Long-term interest rates and risk spreads remain very low. Volatility in many financial prices is currently unusually low. Markets appear to be attaching a very low probability to any rise in global interest rates or other adverse event over the period ahead. In Australia, the most recent survey data indicate gradually improving business conditions and some recovery in household sentiment after a weaker period around mid year, suggesting moderate growth in the economy is occurring. Resources sector investment spending is starting to decline significantly. Investment intentions in some other sectors continue to improve, though these areas of capital spending are expected to see only moderate growth in the near term. Public spending is scheduled to be subdued. Overall, the Bank still expects growth to be a little below trend over the year ahead. The recorded rate of unemployment has increased recently, despite some improvement in most other indicators for the labour market this year. The Bank's assessment remains that the labour market has a degree of spare capacity and that it will probably be some time yet before unemployment declines consistently. Growth in wages has declined noticeably and is expected to remain relatively modest over the period ahead, which should keep inflation consistent with the target even with lower levels of the exchange rate. Monetary policy remains accommodative. Interest rates are very low and have continued to edge lower over recent months as competition to lend has increased. Investors continue to look for higher returns in response to low rates on safe instruments. Credit growth has picked up a little, including most recently to businesses. The increase in dwelling prices continues. The exchange rate, on the other hand, remains above most estimates of its fundamental value, particularly given the declines in key commodity prices. It is offering less assistance than would normally be expected in achieving balanced growth in the economy. Looking ahead, continued accommodative monetary policy should provide support to demand and help growth to strengthen over time. Inflation is expected to be consistent with the 2-3 per cent target over the next two years. In the Board's judgement, monetary policy is appropriately configured to foster sustainable growth in demand and inflation outcomes consistent with the target. On present indications, the most prudent course is likely to be a period of stability in interest rates. Source: Reserve Bank of Australia, "Statement by Glenn Stevens, Govemor: Monetary Policy Decision," press release, September 2, 2014, accessed February 22, 2017, www.rba.gov.au/media-releases/2014/mr-14-15.html. September 16, 2014 Hi Mr. Goode, On your request, please see the following indicative pricing on some AUD/EUR FX hedging solutions: All pricing is indicative and based off spot AUD/EUR 0.6980. The four (4) month FEC (Foreign Exchange Forward contract) is 0.6910 (spot of 0.6980 less 70 forward points). Solution 1-Purchase an AUD Put/EUR Call Option Expiry Date: Value Date: 2015-01-14 (four months) 2015-01-16 Strike 1:0.6910 (at-the-money fwd) Strike 2:0.6860 (50 pips out-of-the-money (OTM)) Premium 1 Premium 2: This solution gives you the right but not the obligation to buy EUR and sell AUD at the strike rate on the expiry date. On the expiry date, if the prevailing spot AUD/EUR is below the strike rate, then you will exercise the right to deal at the higher strike rate. Conversely, if the prevailing spot AUD/EUR rate is higher than the strike rate, then you will let the option lapse and buy EUR against the AUD in the spot market at the higher rate. I have provided you with two prices so you can see the relationship between premium and strike prices. 2.13% of AUD face value (~146 AUD/EUR pips) 1.81% of AUD face value (~124 AUD/EUR pips) Solution 2-AUD/EUR Collar Option-Buy an AUD Put/EUR Call and Sell an AUD Call/EUR Put-Zero Premium Expiry Date: Value Date: B Put Strike: S Call Strike: B Put Strike: S Call Strike: 2015-01-14 (four months) 2015-01-16 0.6860 (50 pips below the FEC) 0.6942 0.6810 (100 pips below the FEC) 0.6983 This solution locks you into a range whereby you have a worst-case rate (bought put strike) and the capacity to participate in favourable AUD/EUR movements up to the sold call strike. Ideally, the worst-case rate would be your budget rate. I have provided you with indicative pricing on two collar structures so that you can compare two different ranges. Remember, a collar structure is an alternative to an FEC; therefore, when assessing participation benefits, use the FEC rate as the benchmark, not the spot rate. Solution 3-AUD/EUR Knock-In Forward-Buy an AUD Put/EUR Call and Sell an AUD Call/EUR Put with Up-and-In Trigger-Zero Premium Expiry Date: 2015-01-14 (four months) Value Date: 2015-01-16 B Put Strike: S Call Strike: 0.6890 (20 pips below the FEC) 0.6890 with up-and-in knock-in trigger at 0.7140 With this structure, your worst-case rate is 0.6890 (20 pips below the FEC). When the option starts, you only have a bought AUD put option with a strike of 0.6890. However, if 0.7140 trades at any time between the option start and expiry date, then you are "knocked in" to a sold AUD call option with a strike of 0.6890. Having a bought AUD put and sold AUD call option with the same strike creates a synthetic forward. So, in layman's terms, this structure gives you a worst-case rate that is 20 pips worse than the FEC; however, you have the opportunity to participate in the AUD/EUR all the way to the trigger rate of 0.7140. If 0.7140 does trade during the life of the option, then you have to deal at the common strike rate of 0.6890. Source: Company documents. F. Mayer Imports: Hedging Foreign Currency Risk Due by 5/16 10pm F. Mayer Imports is an Australian wholesale food importer that imports high-end European gourmet food products for distribution in the Australian retail food markets (e.g., food supermarkets). Given the high volatility of the Australian Dollar Euro exchange rate (A$/€), F. Mayer's profit margins, competitive position, and market share are heavily affected by the difference in its target A$/ € exchange rate and the actual A$/ € exchange rate. F. Mayer estimates its wholesale prices for imported food products using an annual budget (target) A$/€ exchange rate based on its forecasts of European, Australian, and global economic and financial market conditions. The target A$/€ exchange rate protects F. Mayer's profit margin and its negotiated prices to retail food markets. The firm keeps any renegotiations of food prices with supermarkets to a minimum in case of an A$ depreciation against Euro to preserve its trading relations and market share. Since the A$/ € currency exchange rate risk is largely borne by F. Mayer, the firm must set a competitive budget A$/€ exchange rate to achieve higher-than- budgeted profit margin and improve its competitive market advantage. This task has become crucial in year 2014 as the AS has depreciated significantly against Euro from A$0.7027 in October 2013 to A$0.6369 in January 2014 (i.e., from A$1-€0.7027 to A$1-€0.6369). F. Mayer budget (target) A$/€ exchange rate for 2014 is A$0.6900 (A$1-€0.6900) and its 2014 total procurement commitment (currency exposure) is around €70 million. Obviously, F. Mayer does not have any bargaining power to negotiate its own A$/ € forward rate, so it has to accept quoted market forward rates as given. Also, F. Mayer has no in-house expertise to forecast the correct direction of possible future A$/€ exchange rate. F. Mayer must decide whether it should hedge its €70 million procurement commitment and, if yes, which of the four hedging strategies will protect its target A$0.6900 exchange rate and may also provide it a better-than-budgeted AS/€ exchange rate for 2014 (i.e., where it pays fewer A$ to buy €70 million than at A$0.6900). You should be to able to answer the above hedging questions if your case analysis addresses the following issues: 1. How effective is F. Mayer's current practice of having no established hedging program (or sporadic short-term hedging using 1-3 months contract in a strong AS environment)? The current practice may have elements of speculation than hedging as the firm makes a judgment call on the direction of A$/ € exchange rate when A$ has gained against Euro. 2. How large is F. Mayer's 2014 currency risk exposure (size of potential losses in A$) for its €70 million procurement commitment if the A$/€ exchange rate during 2014 is as volatile as during the previous 12 months (see Exhibit 1)?

Expert Answer:

Answer rating: 100% (QA)

To analyze F Mayers hedging situation we need to consider the effectiveness of its current practice and assess the size of its currency risk exposure ... View the full answer

Related Book For

Fraud examination

ISBN: 978-0538470841

4th edition

Authors: Steve Albrecht, Chad Albrecht, Conan Albrecht, Mark zimbelma

Posted Date:

Students also viewed these accounting questions

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

Ann Carter, Chief Financial Officer of Consolidated Electric Company (Con El), must make a recommendation to Con Els board of directors regarding the firms dividend policy. Con El owns two...

-

On a beautiful spring morning in 2015, Stephen Lowber, chief financial officer of Cutter and Buck, Inc., slowly arose from his bed, walked across the bedroom floor, and gazed out the window. It was a...

-

The following are the Ledger Balance (in thousands) extracted from the books of Vaishnavi Bank Ltd as on March 31, 2016. The bank's Profit and Loss Account for the year ended and Balance Sheet as at...

-

Presented below is the condensed balance sheet for Express, Inc. as of December 31, 2011. Express has decided that it needs to purchase a new crane for its operations. The new crane costs $900,000...

-

1. Graph in Excel showing the evolution of Australian Real GDP and Real Wages Growth since 2000 till June 2023. 2. Graphs in Excel for two other variables whose own evolution sheds light on that of...

-

A partial condenser operates as shown in Figure 10.36. Assuming that \(T_{0}=70^{\circ} \mathrm{F}\), calculate the following: (a) Condenser duty (b) Change in availability function (c) Lost work (d)...

-

Scotwood Industries, Inc., sells calcium chloride flake for use in ice melt products. Between July and September 2004, Scotwood delivered thirty-seven shipments of flake to Frank Miller & Sons, Inc....

-

For the circuit in Figure Q4, determine the following: a) R1 b) l c) l d) IRZ Vs 40 V XL2 m 75 R w 47 XL3 A m 45 R B w 68 XLI 100 tot Question 05: a) Find it through is in the circuit in Figure 5a....

-

On October 1, 20Y8, Jacinto Suarez and Tricia Fritz form a partnership. Suarez agrees to invest $25,000 in cash and inventory valued at $60,000. Fritz invests certain business assets at valuations...

-

Two major recessions have plagued the world this millennium. The Great Recession of 2008 was, at the time, the worst recession since the Great Depression of the 1930s. Many people lost their jobs and...

-

Frank and Helen are not married. Helen has a child (Mary) from a prior relationship. (The father of Mary is deceased.) Frank and Helen have been living together for several months. After an argument,...

-

Sarasota Corporation has 128,000 common shares outstanding with a carrying value of $22 per share. Sarasota declares a 2-for-1 stock split. (a) How many shares are outstanding after the split? Number...

-

Dividing partnership net loss Morgan Graff and Serigo Vargas formed a partnership in which the partnership agreement provided for salary allowances of $50,000 and $44,000, respectively. Determine the...

-

Raj was granted a student visa on 15 March 2020, to cease on 15 November 2023. His CoE is for a Master of Professional Accounting. He has passed only 2 subjects out of 12 so far, but he applied for a...

-

Cases: Case 1: A send message to D Case 2: B send message to A Questions: a) In the case 1; A sends a packet to D, the left switch will send the frame via which interface? b) What is the content of...

-

Company A had 30% debt and 70% equity (in market value terms). It had 1 million shares outstanding, and the stock traded at $35. It decides on a leveraged recapitalization by issuing an additional...

-

Distinguish between the work performed by public accountants and the work performed by accountants in commerce and industry and in not-for-profit organisations.

-

Sams Electronics Universe has discovered and investigated a kickback fraud perpetrated by its purchasing agent. The fraud lasted eight months and cost the company $2 million in excess inventory...

-

Mr. Oaks has worked as the CEO of Turley Bank for the last three years. This past year, the outside auditor discovered some fraudulent loan activity in which Mr. Oaks was circumventing internal...

-

(Multiple choice) 1. Financial statement fraud is usually committed by: a. Executives. b. Managers. c. Stockholders. d. Outsiders. e. Both a and b. 2. Which officer in a company is most likely to be...

-

What would be the most effective option to increase employee motivation to stay and reduce the driver turnover rate? Why do you believe this option will be effective?

-

How else might the manager have handled the situation to prevent potential issues, including a negative impact on the teams performance?

-

In what ways do you believe providing special work arrangements or accommodations for employees impacts employee motivation? How does it help? How does it hurt?

Study smarter with the SolutionInn App