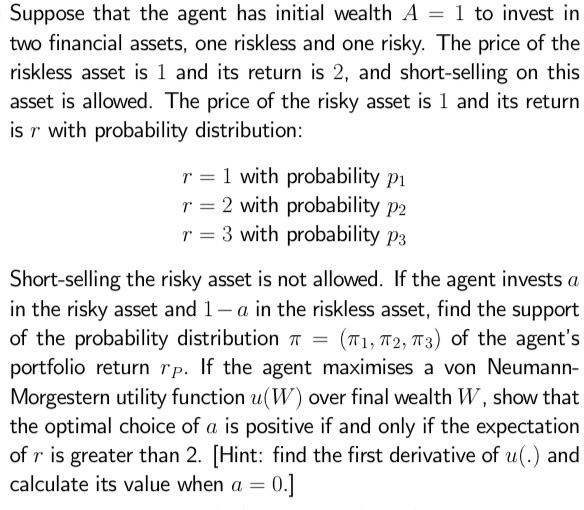

Suppose that the agent has initial wealth A = 1 to invest in two financial assets,...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

To find the support of the probability distribution T1 T2 T3 of the agents portfolio return rp we need to consider the different possible outcomes bas... View the full answer

Related Book For

Posted Date: