Suppose that you have $10,000 to invest on the market. You are considering two strategies: (i) Invest

Question:

Suppose that you have $10,000 to invest on the market. You are considering two strategies:

(i) Invest in the S&P 500 (say by buying an ETF such as SPY or VTI or by putting it into a mutual fund such as FXAIX.).

(ii) Buying at-the-money S&P 500 options (SPX options).

You begin your investment on March 31, 2022 when the S&P 500 was at $4,530. At-the-money options (i.e. with strike K = $4530) are available with a Black-Scholes volatility of = 21% with an expiration of T = 3 months.

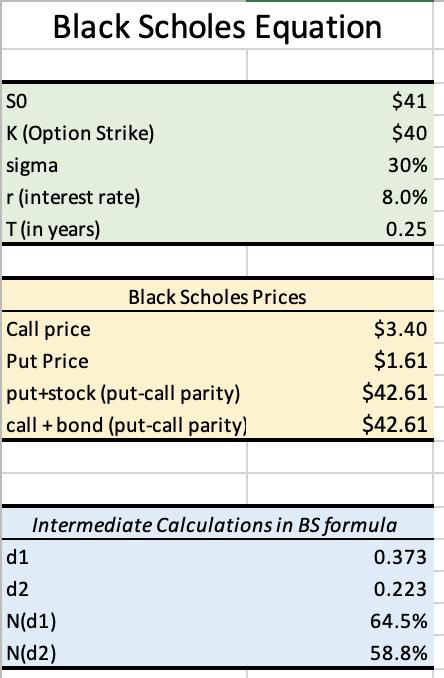

(a) Using the provided data, find the Black-Scholes model price of the at-the-money 3-month option. Take r = 0:50% as the risk-free rate.

b) Suppose that in 3-month, the S&P 500 is at $4900. What is the return for strategy (i)? What is the return for strategy (ii)?

c) Repeat (b) assuming that the S&P 500 ends up at $4700.

d) Repeat (b) assuming that the S&P 500 ends up at $4530.

Expert Answer:

To calculate the returns for each strategy we need to determine the final value of the investment un... View the full answer

Essentials Of Corporate Finance

ISBN: 9780073382463

7th Edition

Authors: Stephen Ross, Randolph Westerfield, Bradford Jordan