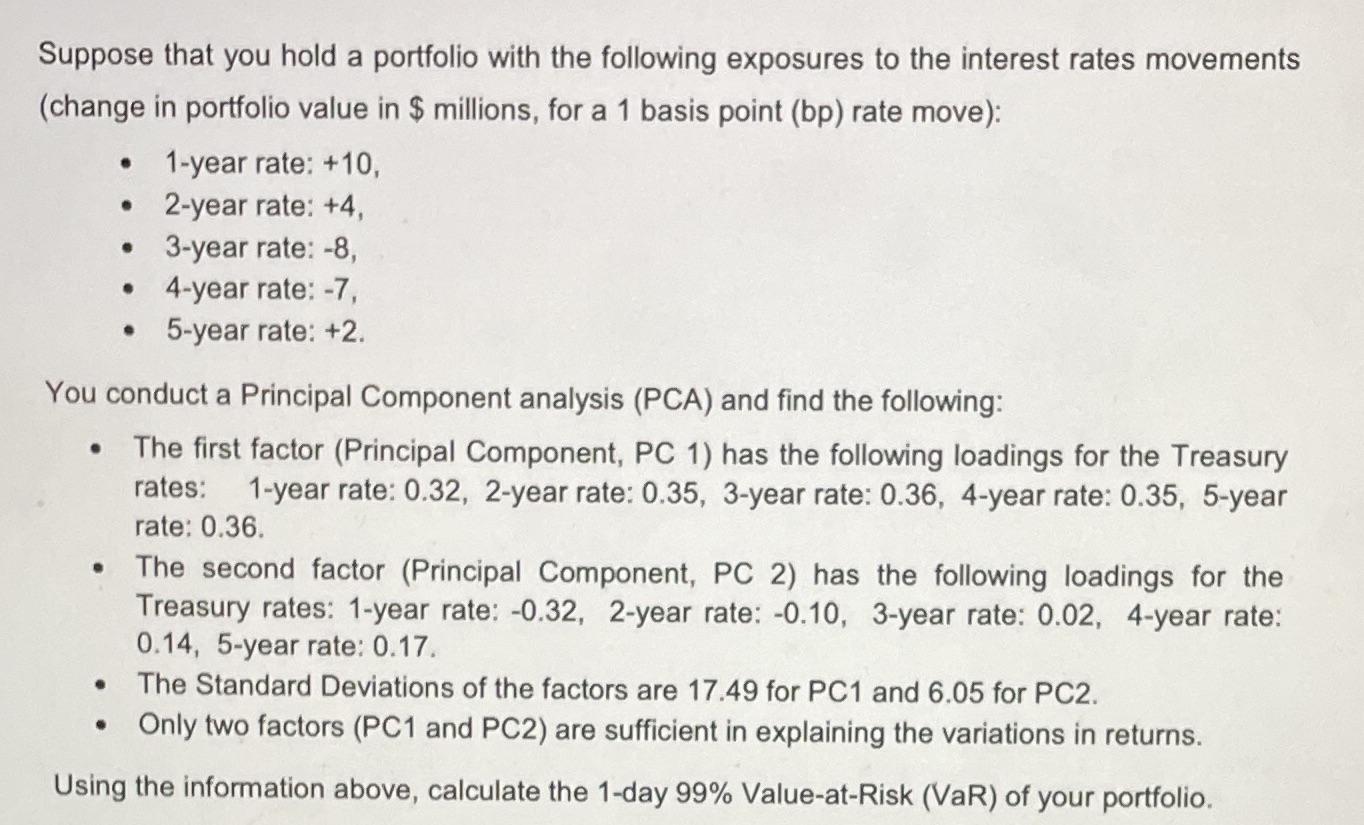

Suppose that you hold a portfolio with the following exposures to the interest rates movements (change...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

To calculate the VaR of the portfolio using the information provided we need to follow these steps C... View the full answer

Related Book For

International Financial Management

ISBN: 978-0078034657

6th Edition

Authors: Cheol S. Eun, Bruce G.Resnick

Posted Date: