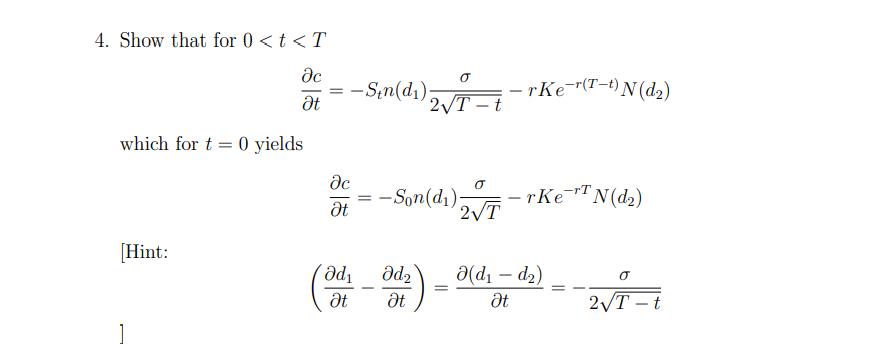

Suppose the time t price St of a non-dividend paying stock follows geometric Brownian motion, i.e.,...

Fantastic news! We've Found the answer you've been seeking!

Question:

![]()

![]()

Expert Answer:

Related Book For

Posted Date: