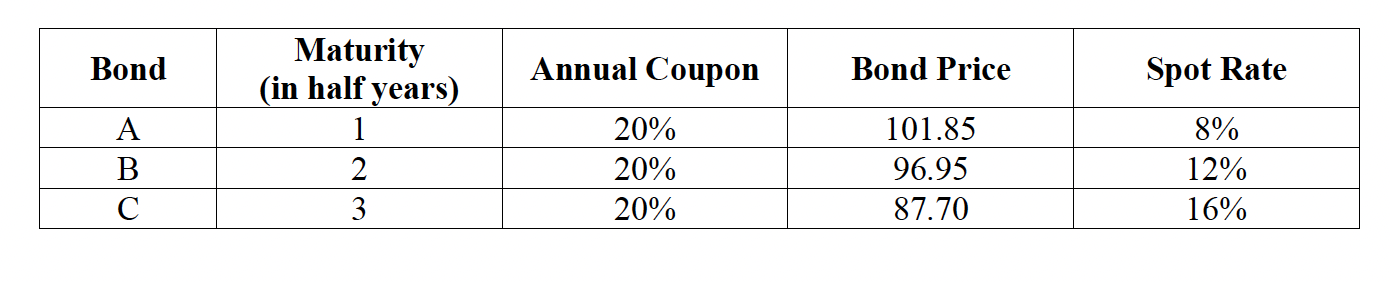

Suppose there is a 1.5y STRIPS (i.e., no coupons) trading at $60 with the par value of

Fantastic news! We've Found the answer you've been seeking!

Question:

- Suppose there is a 1.5y STRIPS (i.e., no coupons) trading at $60 with the par value of $100. Determine if there is an arbitrage opportunity. If so, what would be your arbitrage strategy?

- For every unit of the STRIP, how many units of Bond A, B, and C do you need to buy or short?

- What would be the price of the replicating portfolio?

Expert Answer:

Posted Date: