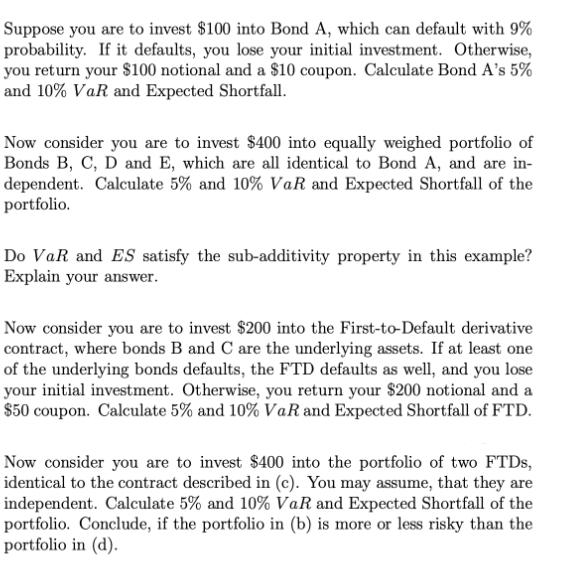

Suppose you are to invest $100 into Bond A, which can default with 9% probability. If...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a Bond As 5 VaR is 0 and its 10 VaR is 100 The expected shortfall can be calculated as follows Expec... View the full answer

Related Book For

Posted Date: