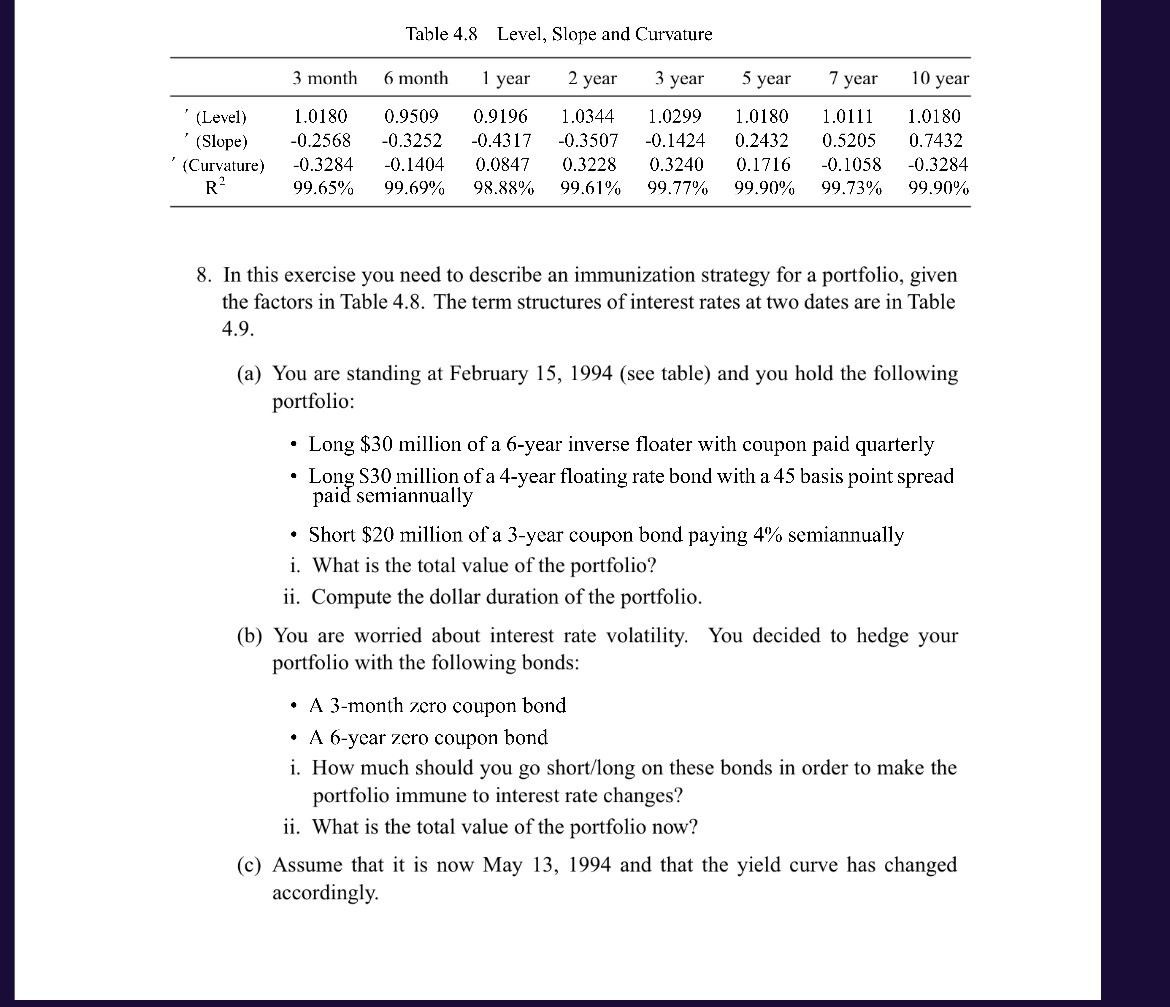

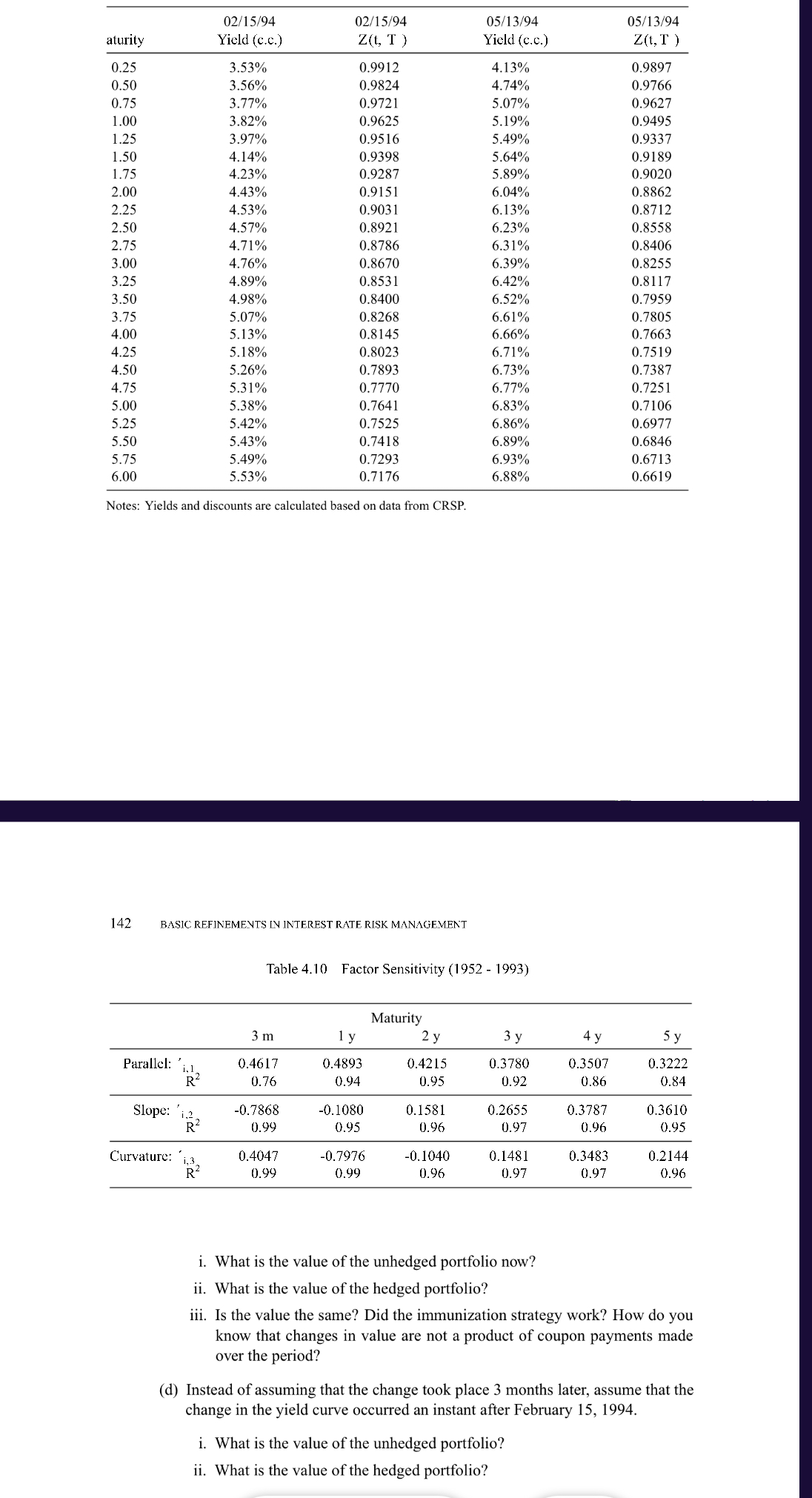

Table 4.8 Level, Slope and Curvature 3 month 6 month 1 year 2 year 7 year...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

To answer the question we need to follow the steps outlined in the problem a i The total value of the portfolio is the sum of the market values of the individual positions 30 million 1 003532 09912 29... View the full answer

Related Book For

Fixed Income Securities Valuation Risk and Risk Management

ISBN: 978-0470109106

1st edition

Authors: Pietro Veronesi

Posted Date: