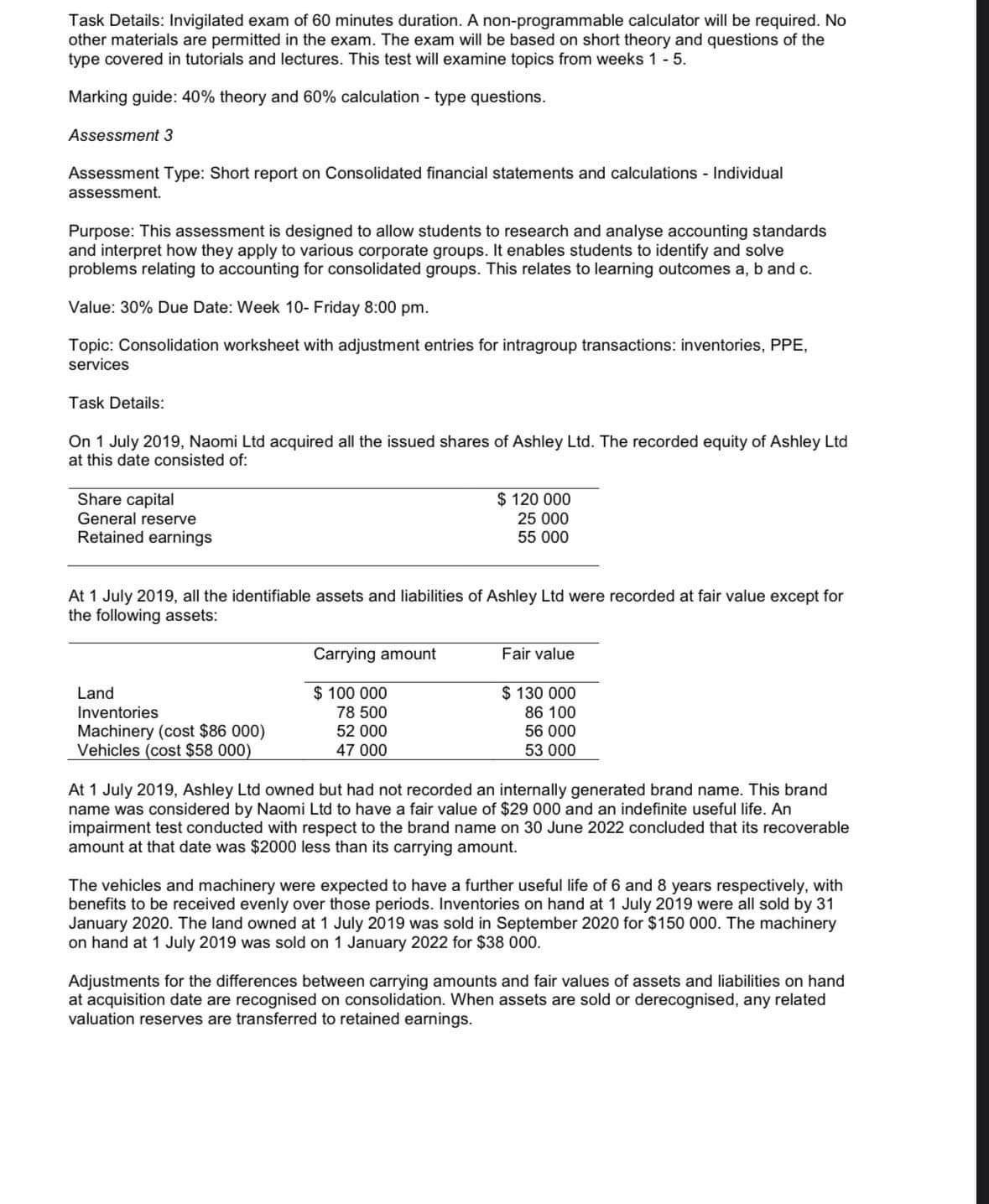

Task Details: Invigilated exam of 60 minutes duration. A non-programmable calculator will be required. No other...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

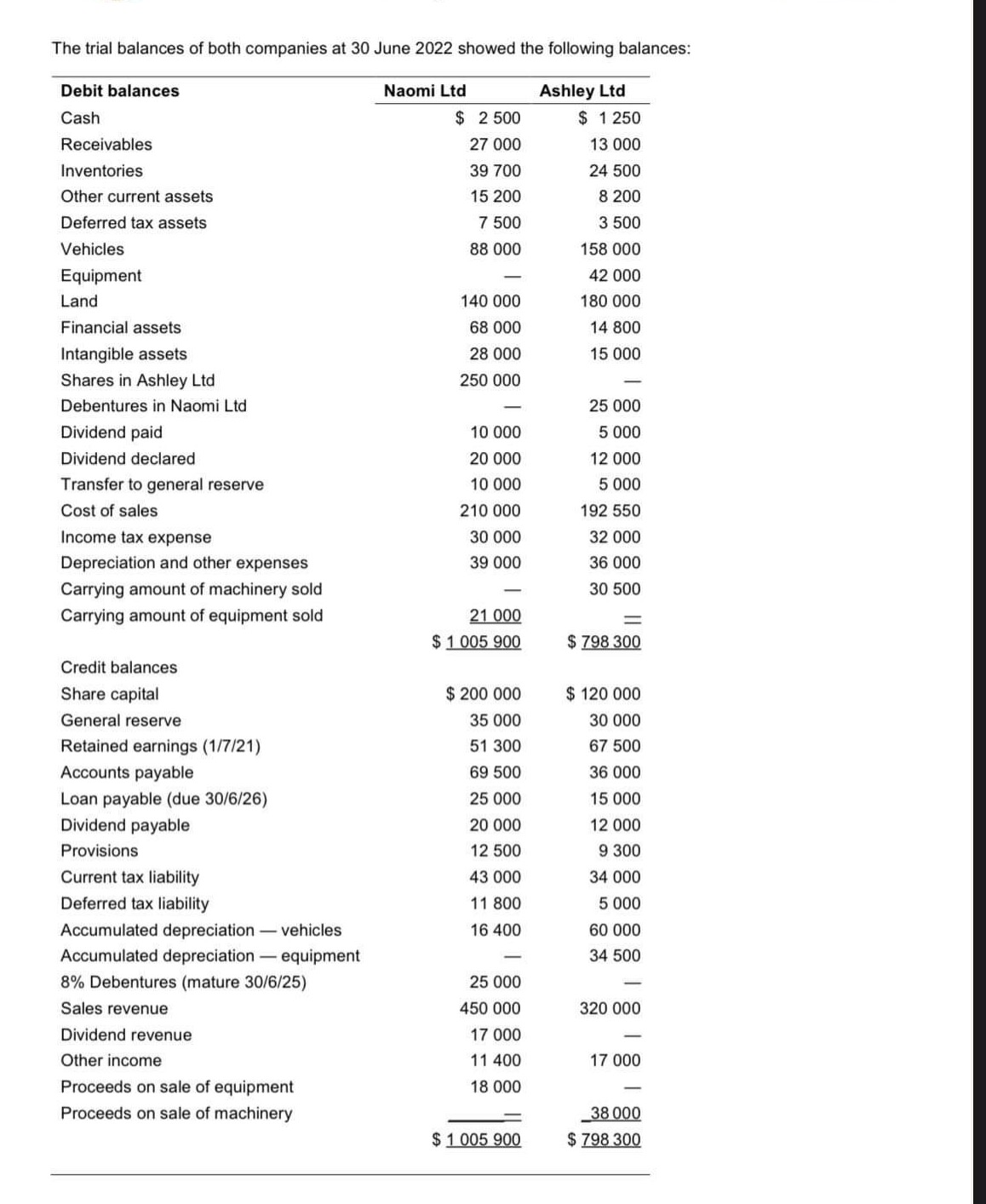

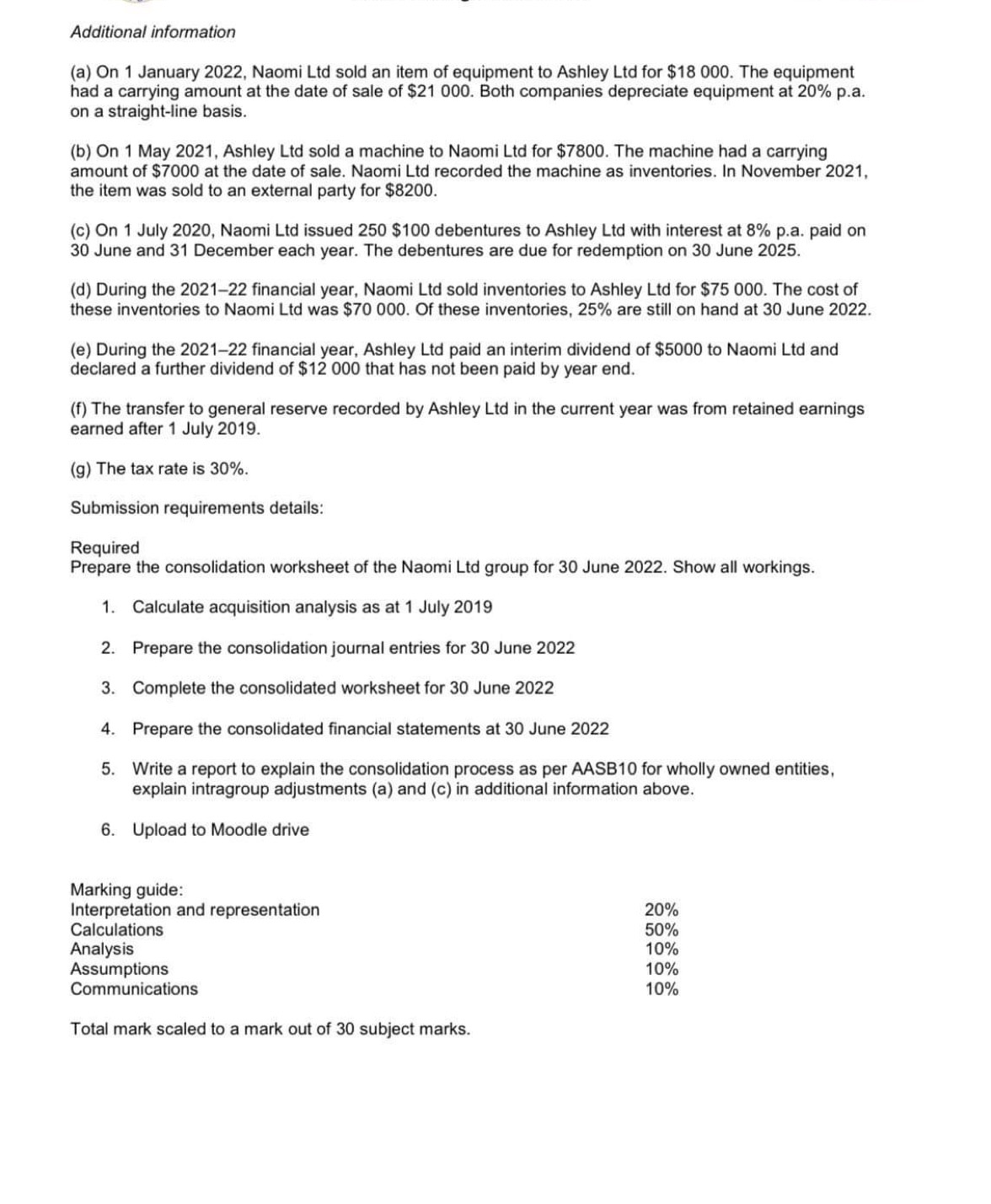

Task Details: Invigilated exam of 60 minutes duration. A non-programmable calculator will be required. No other materials are permitted in the exam. The exam will be based on short theory and questions of the type covered in tutorials and lectures. This test will examine topics from weeks 1 - 5. Marking guide: 40% theory and 60% calculation - type questions. Assessment 3 Assessment Type: Short report on Consolidated financial statements and calculations - Individual assessment. Purpose: This assessment is designed to allow students to research and analyse accounting standards and interpret how they apply to various corporate groups. It enables students to identify and solve problems relating to accounting for consolidated groups. This relates to learning outcomes a, b and c. Value: 30% Due Date: Week 10- Friday 8:00 pm. Topic: Consolidation worksheet with adjustment entries for intragroup transactions: inventories, PPE, services Task Details: On 1 July 2019, Naomi Ltd acquired all the issued shares of Ashley Ltd. The recorded equity of Ashley Ltd at this date consisted of: Share capital General reserve Retained earnings $ 120 000 25 000 55 000 At 1 July 2019, all the identifiable assets and liabilities of Ashley Ltd were recorded at fair value except for the following assets: Carrying amount Fair value Land Inventories $ 100 000 $ 130 000 78 500 86 100 Machinery (cost $86 000) 52 000 Vehicles (cost $58 000) 47 000 56 000 53 000 At 1 July 2019, Ashley Ltd owned but had not recorded an internally generated brand name. This brand name was considered by Naomi Ltd to have a fair value of $29 000 and an indefinite useful life. An impairment test conducted with respect to the brand name on 30 June 2022 concluded that its recoverable amount at that date was $2000 less than its carrying amount. The vehicles and machinery were expected to have a further useful life of 6 and 8 years respectively, with benefits to be received evenly over those periods. Inventories on hand at 1 July 2019 were all sold by 31 January 2020. The land owned at 1 July 2019 was sold in September 2020 for $150 000. The machinery on hand at 1 July 2019 was sold on 1 January 2022 for $38 000. Adjustments for the differences between carrying amounts and fair values of assets and liabilities on hand at acquisition date are recognised on consolidation. When assets are sold or derecognised, any related valuation reserves are transferred to retained earnings. The trial balances of both companies at 30 June 2022 showed the following balances: Debit balances Cash Receivables Inventories Other current assets Deferred tax assets Vehicles Equipment Naomi Ltd $ 2500 Ashley Ltd $ 1 250 27 000 13 000 39 700 24 500 15 200 8 200 7 500 3 500 88 000 158 000 42 000 Land 140 000 180 000 Financial assets 68 000 14 800 Intangible assets 28 000 15 000 Shares in Ashley Ltd 250 000 Debentures in Naomi Ltd 25 000 Dividend paid 10 000 5 000 Dividend declared 20 000 12 000 Transfer to general reserve 10 000 5 000 Cost of sales 210 000 192 550 Income tax expense 30 000 32 000 Depreciation and other expenses 39 000 36 000 Carrying amount of machinery sold Carrying amount of equipment sold Credit balances 30 500 21 000 = $ 1 005 900 $ 798 300 Share capital $ 200 000 $ 120 000 General reserve 35 000 30 000 Retained earnings (1/7/21) 51 300 67 500 Accounts payable 69 500 36 000 Loan payable (due 30/6/26) 25 000 15 000 Dividend payable 20 000 12 000 Provisions 12 500 9 300 Current tax liability 43 000 34 000 Deferred tax liability 11 800 5 000 Accumulated depreciation-vehicles 16 400 60 000 Accumulated depreciation-equipment - 34 500 8% Debentures (mature 30/6/25) 25 000 Sales revenue 450 000 320 000 Dividend revenue 17 000 Other income 11 400 17 000 Proceeds on sale of equipment 18 000 Proceeds on sale of machinery 38 000 $ 1.005 900 $798 300 Additional information (a) On 1 January 2022, Naomi Ltd sold an item of equipment to Ashley Ltd for $18 000. The equipment had a carrying amount at the date of sale of $21 000. Both companies depreciate equipment at 20% p.a. on a straight-line basis. (b) On 1 May 2021, Ashley Ltd sold a machine to Naomi Ltd for $7800. The machine had a carrying amount of $7000 at the date of sale. Naomi Ltd recorded the machine as inventories. In November 2021, the item was sold to an external party for $8200. (c) On 1 July 2020, Naomi Ltd issued 250 $100 debentures to Ashley Ltd with interest at 8% p.a. paid on 30 June and 31 December each year. The debentures are due for redemption on 30 June 2025. (d) During the 2021-22 financial year, Naomi Ltd sold inventories to Ashley Ltd for $75 000. The cost of these inventories to Naomi Ltd was $70 000. Of these inventories, 25% are still on hand at 30 June 2022. (e) During the 2021-22 financial year, Ashley Ltd paid an interim dividend of $5000 to Naomi Ltd and declared a further dividend of $12 000 that has not been paid by year end. (f) The transfer to general reserve recorded by Ashley Ltd in the current year was from retained earnings earned after 1 July 2019. (g) The tax rate is 30%. Submission requirements details: Required Prepare the consolidation worksheet of the Naomi Ltd group for 30 June 2022. Show all workings. 1. Calculate acquisition analysis as at 1 July 2019 2. Prepare the consolidation journal entries for 30 June 2022 3. Complete the consolidated worksheet for 30 June 2022 4. Prepare the consolidated financial statements at 30 June 2022 5. Write a report to explain the consolidation process as per AASB10 for wholly owned entities, explain intragroup adjustments (a) and (c) in additional information above. 6. Upload to Moodle drive Marking guide: Interpretation and representation Calculations Analysis Assumptions Communications Total mark scaled to a mark out of 30 subject marks. 20% 50% 10% 10% 10% Task Details: Invigilated exam of 60 minutes duration. A non-programmable calculator will be required. No other materials are permitted in the exam. The exam will be based on short theory and questions of the type covered in tutorials and lectures. This test will examine topics from weeks 1 - 5. Marking guide: 40% theory and 60% calculation - type questions. Assessment 3 Assessment Type: Short report on Consolidated financial statements and calculations - Individual assessment. Purpose: This assessment is designed to allow students to research and analyse accounting standards and interpret how they apply to various corporate groups. It enables students to identify and solve problems relating to accounting for consolidated groups. This relates to learning outcomes a, b and c. Value: 30% Due Date: Week 10- Friday 8:00 pm. Topic: Consolidation worksheet with adjustment entries for intragroup transactions: inventories, PPE, services Task Details: On 1 July 2019, Naomi Ltd acquired all the issued shares of Ashley Ltd. The recorded equity of Ashley Ltd at this date consisted of: Share capital General reserve Retained earnings $ 120 000 25 000 55 000 At 1 July 2019, all the identifiable assets and liabilities of Ashley Ltd were recorded at fair value except for the following assets: Carrying amount Fair value Land Inventories $ 100 000 $ 130 000 78 500 86 100 Machinery (cost $86 000) 52 000 Vehicles (cost $58 000) 47 000 56 000 53 000 At 1 July 2019, Ashley Ltd owned but had not recorded an internally generated brand name. This brand name was considered by Naomi Ltd to have a fair value of $29 000 and an indefinite useful life. An impairment test conducted with respect to the brand name on 30 June 2022 concluded that its recoverable amount at that date was $2000 less than its carrying amount. The vehicles and machinery were expected to have a further useful life of 6 and 8 years respectively, with benefits to be received evenly over those periods. Inventories on hand at 1 July 2019 were all sold by 31 January 2020. The land owned at 1 July 2019 was sold in September 2020 for $150 000. The machinery on hand at 1 July 2019 was sold on 1 January 2022 for $38 000. Adjustments for the differences between carrying amounts and fair values of assets and liabilities on hand at acquisition date are recognised on consolidation. When assets are sold or derecognised, any related valuation reserves are transferred to retained earnings. The trial balances of both companies at 30 June 2022 showed the following balances: Debit balances Cash Receivables Inventories Other current assets Deferred tax assets Vehicles Equipment Naomi Ltd $ 2500 Ashley Ltd $ 1 250 27 000 13 000 39 700 24 500 15 200 8 200 7 500 3 500 88 000 158 000 42 000 Land 140 000 180 000 Financial assets 68 000 14 800 Intangible assets 28 000 15 000 Shares in Ashley Ltd 250 000 Debentures in Naomi Ltd 25 000 Dividend paid 10 000 5 000 Dividend declared 20 000 12 000 Transfer to general reserve 10 000 5 000 Cost of sales 210 000 192 550 Income tax expense 30 000 32 000 Depreciation and other expenses 39 000 36 000 Carrying amount of machinery sold Carrying amount of equipment sold Credit balances 30 500 21 000 = $ 1 005 900 $ 798 300 Share capital $ 200 000 $ 120 000 General reserve 35 000 30 000 Retained earnings (1/7/21) 51 300 67 500 Accounts payable 69 500 36 000 Loan payable (due 30/6/26) 25 000 15 000 Dividend payable 20 000 12 000 Provisions 12 500 9 300 Current tax liability 43 000 34 000 Deferred tax liability 11 800 5 000 Accumulated depreciation-vehicles 16 400 60 000 Accumulated depreciation-equipment - 34 500 8% Debentures (mature 30/6/25) 25 000 Sales revenue 450 000 320 000 Dividend revenue 17 000 Other income 11 400 17 000 Proceeds on sale of equipment 18 000 Proceeds on sale of machinery 38 000 $ 1.005 900 $798 300 Additional information (a) On 1 January 2022, Naomi Ltd sold an item of equipment to Ashley Ltd for $18 000. The equipment had a carrying amount at the date of sale of $21 000. Both companies depreciate equipment at 20% p.a. on a straight-line basis. (b) On 1 May 2021, Ashley Ltd sold a machine to Naomi Ltd for $7800. The machine had a carrying amount of $7000 at the date of sale. Naomi Ltd recorded the machine as inventories. In November 2021, the item was sold to an external party for $8200. (c) On 1 July 2020, Naomi Ltd issued 250 $100 debentures to Ashley Ltd with interest at 8% p.a. paid on 30 June and 31 December each year. The debentures are due for redemption on 30 June 2025. (d) During the 2021-22 financial year, Naomi Ltd sold inventories to Ashley Ltd for $75 000. The cost of these inventories to Naomi Ltd was $70 000. Of these inventories, 25% are still on hand at 30 June 2022. (e) During the 2021-22 financial year, Ashley Ltd paid an interim dividend of $5000 to Naomi Ltd and declared a further dividend of $12 000 that has not been paid by year end. (f) The transfer to general reserve recorded by Ashley Ltd in the current year was from retained earnings earned after 1 July 2019. (g) The tax rate is 30%. Submission requirements details: Required Prepare the consolidation worksheet of the Naomi Ltd group for 30 June 2022. Show all workings. 1. Calculate acquisition analysis as at 1 July 2019 2. Prepare the consolidation journal entries for 30 June 2022 3. Complete the consolidated worksheet for 30 June 2022 4. Prepare the consolidated financial statements at 30 June 2022 5. Write a report to explain the consolidation process as per AASB10 for wholly owned entities, explain intragroup adjustments (a) and (c) in additional information above. 6. Upload to Moodle drive Marking guide: Interpretation and representation Calculations Analysis Assumptions Communications Total mark scaled to a mark out of 30 subject marks. 20% 50% 10% 10% 10%

Expert Answer:

Answer rating: 100% (QA)

Assessment Type Short report on Consolidated financial statements and calculations Individual assessment Value 30 Due Date Week 10 Friday 800 pm Topic ... View the full answer

Related Book For

Applied Regression Analysis and Other Multivariable Methods

ISBN: 978-1285051086

5th edition

Authors: David G. Kleinbaum, Lawrence L. Kupper, Azhar Nizam, Eli S. Rosenberg

Posted Date:

Students also viewed these accounting questions

-

Read the case study "Southwest Airlines," found in Part 2 of your textbook. Review the "Guide to Case Analysis" found on pp. CA1 - CA11 of your textbook. (This guide follows the last case in the...

-

Discuss the impact of commissions in organizations growth?

-

The capital retention approach determines the amount of life insurance needed by first determining what level of annual income the insured wishes to provide for the family.

-

From t = 0 to t = 5.00 min, a man stands still, and from t = 5.00 min to t = 10.0 min, he walks briskly in a straight line at a constant speed of 2.20 m/s. What are (a) His average velocity vavg and...

-

Consider figure P8.43. Let the inertia of the block on the table be \(M\) and that of the hanging bock be \(M / 4\). If the coefficient of kinetic friction between the table and the block is 0.2 ,...

-

For each lettered space in the following table, determine the appropriate dollar amount: Total Quantity of Fixed Average Output, Cost Fixed Total Variable Variable Cost Total CostMarginal...

-

1. In figure, two identical particles each of mass m are tied together with an inextensible string. This is pulled at its centre with a constant force F. If the whole system lies on a smooth...

-

Paisley Corporation operates in an industry that has a high rate of bad debt. The year-end balance reported in the balance sheet for the Allowance for Doubtful Accounts will be based on the aging...

-

In accordance with the assignment technique, discuss the various control techniques that will be used with this specific design. Develop a hypothetical research scenario that would necessitate the...

-

Discuss the various control techniques that will be used with this specific design. Develop a hypothetical research scenario that would necessitate the use of an A-B-A Design. The research will be...

-

Discuss the major threats to validity associated with this design and type of research (experimental). How will these threats be addressed, based on the discussion of the control techniques in the...

-

Develop the appropriate primary research question to be associated with this design. Develop a hypothetical research scenario that would necessitate the use of an A-B-A Design. The research will be...

-

Identify the assignment technique to be used. Develop a hypothetical research scenario that would necessitate the use of a 2 x 2 Factorial Design. The research will be considered non experimental.

-

Big Rock Candy Mountain Mining Co. Income Statements For the Years 2019 and 2020 2020 2019 Sales $412,500 $398,600 Cost of Goods 318,786 315,300 Gross Profit 93,714 83,300 Depreciation 29,800 29,652...

-

At 31 December 20X9, the end of the annual reporting period, the accounts of Huron Company showed the following: a. Sales revenue for 20X9, $ 2,950,000, of which one- quarter was on credit. b....

-

A five-year follow-up study was carried out to assess the relationship of diet and weight to the incidence of stomach cancer in 40- to 50-year-old males in a certain metropolitan area. Let K- denote...

-

A random sample of 52 persons attending a certain diet clinic was found to have lost (over a three-week period) an average of 30 pounds, with a sample standard deviation of 11. For these data, a 99%...

-

For the data from Problem 2 in this chapter, address the following questions, using the information provided in the accompanying SAS output. a. State the regression model that incorporates the...

-

A company issues $1,000,000 face value of 10-year bonds on January 1, 2015 when the market interest rate on bonds of comparable risk and terms is 5%. Th e bonds pay 6% interest annually on December...

-

Midland Brands issues three-year bonds dated January 1, 2015 with a face value of $5,000,000. Th e market interest rate on bonds of comparable risk and term is 3%. If the bonds pay 2.5% annually on...

-

A company redeems \($1\),000,000 face value bonds with a carrying value of \($990\),000. If the call price is 104 the company will: A . reduce bonds payable by \($1\),000,000. B . recognize a loss on...

Study smarter with the SolutionInn App