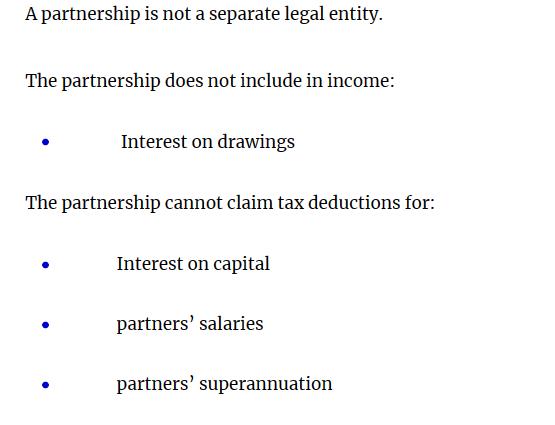

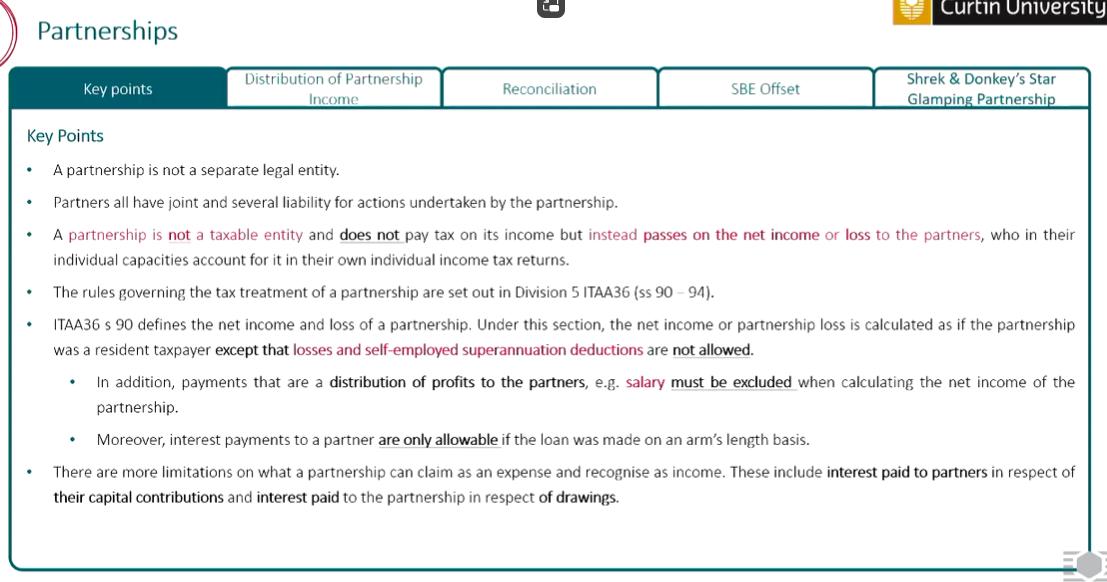

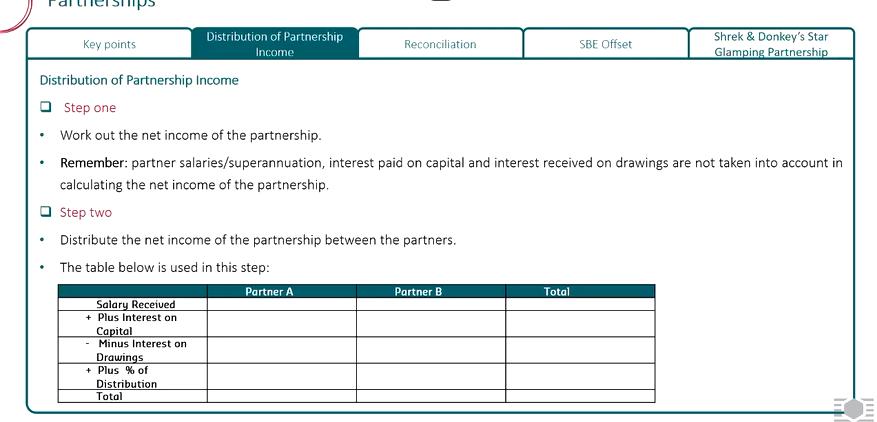

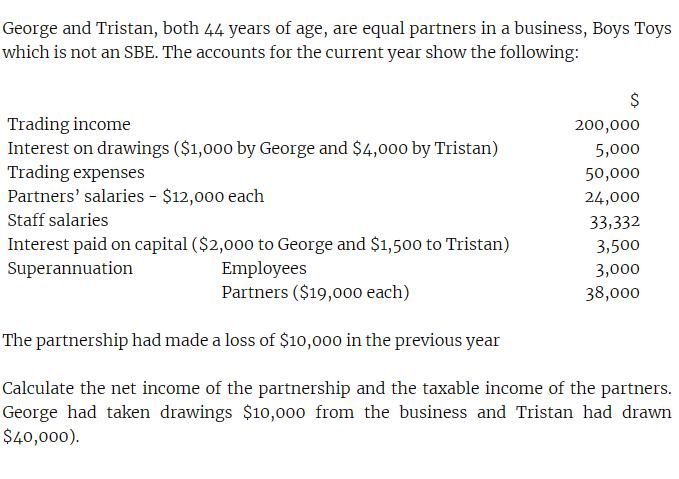

A partnership is not a separate legal entity. The partnership does not include in income: Interest...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Solution In Australia partnerships are governed by the Partnership Act 1892 NSW and the Income Tax A... View the full answer

Related Book For

Smith and Roberson Business Law

ISBN: 978-0538473637

15th Edition

Authors: Richard A. Mann, Barry S. Roberts

Posted Date: