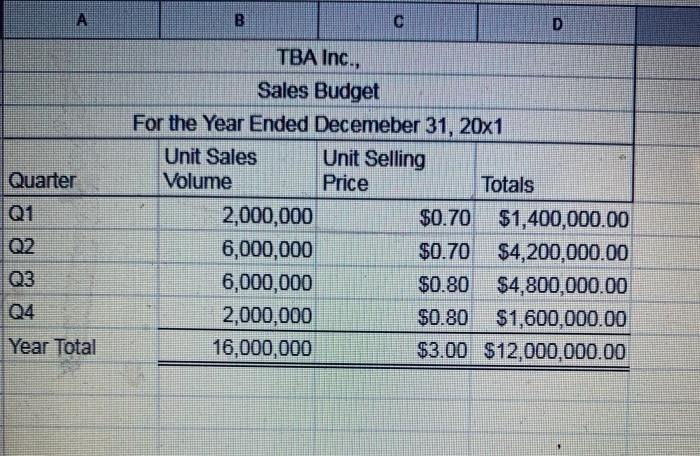

TBA, Inc., manufactures and sells concrete blocks for residential and commercial buildings. TBA expects to sell the

Question:

TBA, Inc., manufactures and sells concrete blocks for residential and commercial buildings. TBA expects to sell the following in 20x1:

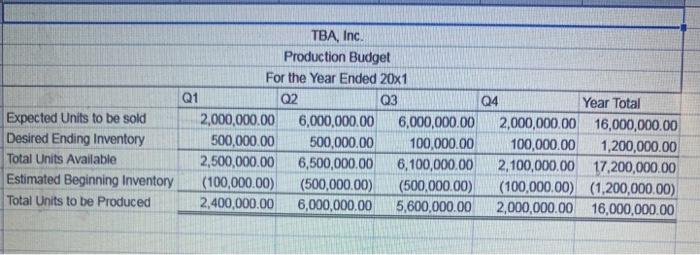

TBA expects the following unit sales and desired to end inventory in 20x1:

Inventory on both January 1, 20x1, and January 1, 20x2, is expected to be 100,000 blocks.

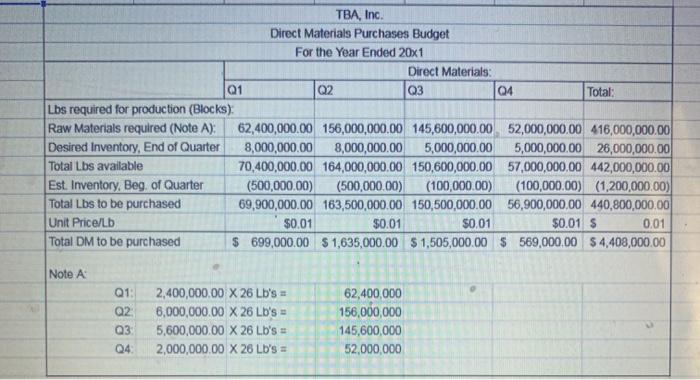

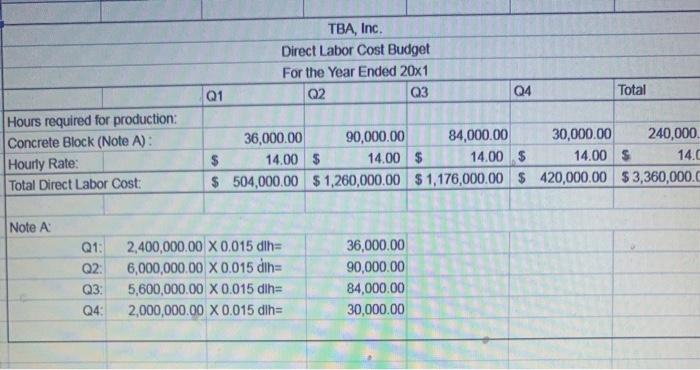

Each block requires 26 pounds of raw materials (a mixture of cement, sand, gravel, shale, pumice, and water). TBA's raw materials inventory policy is to have 5 million pounds in ending inventory for the third and fourth quarters and 8 million pounds in ending inventory for the first and second quarters. Thus, desired direct materials inventory on both January 1, 20x1, and January 1, 20x2, is 5,000,000 pounds of materials. Each pound of raw materials costs $0.01.

Each block requires 0.015 direct labor hours; direct labor is paid $14 per direct labor hour.

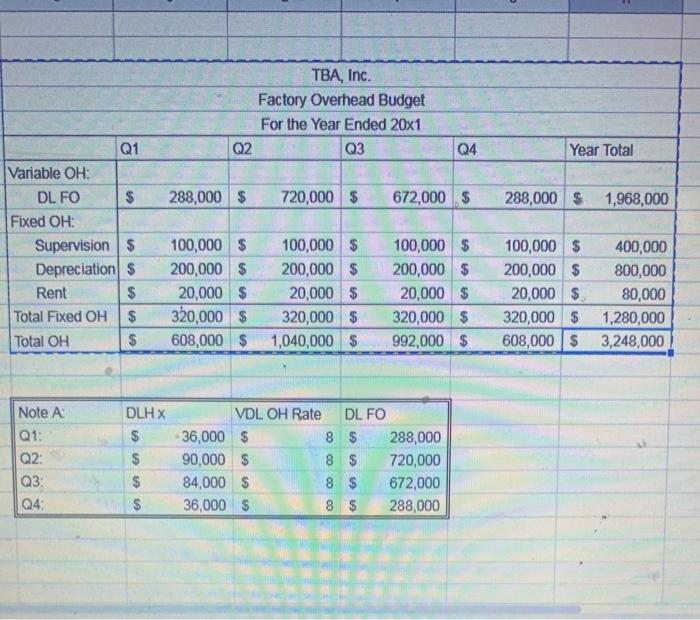

Variable overhead is $8 per direct labor hour. Fixed overhead is budgeted at $320,000 per quarter ($100,000 for supervision, $200,000 for depreciation, and $20,000 for rent).

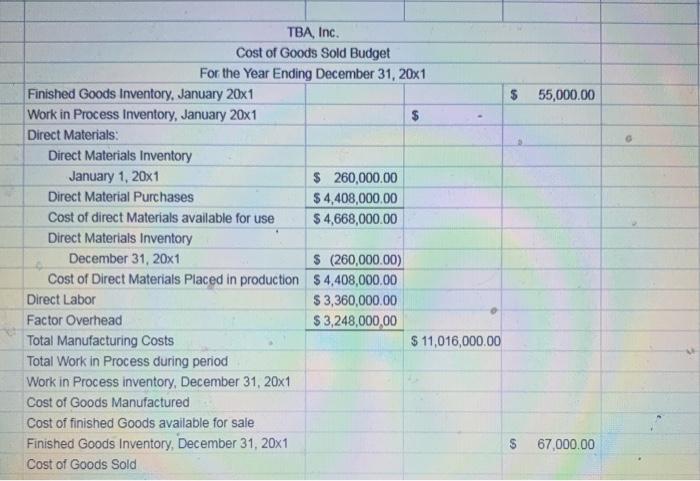

TBA also provided the information that the beginning finished goods inventory is $55,000, and the ending finished goods inventory budget for ABT for the year $67,000.

TBA's only variable marketing expense is a $0.05 commission per unit (block) sold. Fixed marketing expenses for each quarter include the following:

Advertising expense is $10,000 in Quarters 1, 3, and 4. However, at the beginning of the summer building season, TBA increases advertising; in Quarter 2, advertising expense is $15,000.

TBA has no variable administrative expense. Fixed administrative expenses for each quarter include the following:

Income taxes are paid at the rate of 30 percent of operating income.

Of the sales on account, 70 percent are collected in the quarter of sale; the remaining 30 percent are collected in the quarter following the sale. Total sales for the fourth quarter of 20x0 totaled $2,000,000.

All materials are purchased on the account; 80 percent of purchases are paid for in the quarter of purchase. The remaining 20 percent are paid in the following quarter. The purchases for the fourth quarter of 20x0 were $500,000.

TBA requires a $100,000 minimum cash balance for the end of each quarter. On December 31, 20x0, the cash balance was $120,000.

Money can be borrowed and repaid in multiples of $100,000. Interest is 12 percent per year. Interest payments are made only for the amount of the principal being repaid. All borrowing takes place at the beginning of a quarter, and all repayment takes place at the end of a quarter.

Budgeted depreciation is $200,000 per quarter for overhead, $5,000 for marketing expenses, and $12,000 for administrative expenses. (Remember that depreciation is not a cash expense and must be deleted from total expenses before the cash budget is prepared.)

The capital budget for 20x1 revealed plans to purchase additional equipment for $600,000 in the first quarter. The acquisition will be financed with operating cash, supplementing it with short-term loans as necessary.

Corporate income taxes of $20,700 will be paid at the end of the fourth quarter.

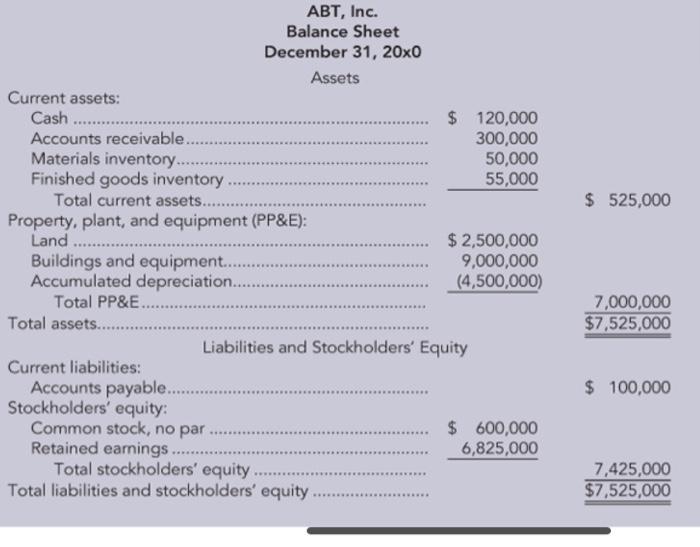

The balance sheet for the beginning of the year is given:

REQUIREMENTS (to be completed using Excel)

9 Construct a budgeted income statement for the coming year.

10. Construct a cash receipts budget for each quarter of the coming year.

11. Construct a cash payments budget for each quarter of the coming year.

12. Prepare a cash budget for each quarter of the coming year.

13. Prepare the Budgeted Balance Sheet for the coming year

Expert Answer:

124 TBA Inc Selling Adminstrative Expense Budget For the Year Ended December 3120X2 125 12... View the full answer

Foundations of Financial Management

ISBN: 978-1259194078

15th edition

Authors: Stanley Block, Geoffrey Hirt, Bartley Danielsen