The credit crisis that began in 2007 served as the trigger for one of the most serious

Question:

The credit crisis that began in 2007 served as the trigger for one of the most serious recessions since the Great Depression. We all know that numerous companies were severely impacted by the recession, especially those whose businesses are especially cyclical (e.g., automobile, steel, etc.). What is less well known is that many state and local governments (municipalities) have also been seriously impacted by the recession. Declining economic activity tends to simultaneously reduce tax revenues and increase expenditures as more citizens are forced to rely on the social safety net.

In the early 1990s, some well-regarded financial engineers proposed that cyclically impacted corporations and municipalities could hedge their "macroeconomic risks" by engaging in macroeconomic derivatives (such as swaps or options). A macroeconomic swap would be a swap in which one leg pays a fixed rate of interest and the other leg pays a floating rate of interest tied to some "macroeconomic index" (such as the growth rate of GDP or an inflation rate such as the CPI). Macroeconomic derivatives are often embedded in other instruments. For example, the U.S. Treasury department's TIPS (Treasury Inflation Protected Securities) contain embedded inflation swaps. In the early 2000s, Goldman Sachs and Deutsche Bank teamed up to offer macroeconomic derivatives (which they called economic derivatives) to their clients. These were structured in much the same way the financial engineers had suggested ten years earlier.

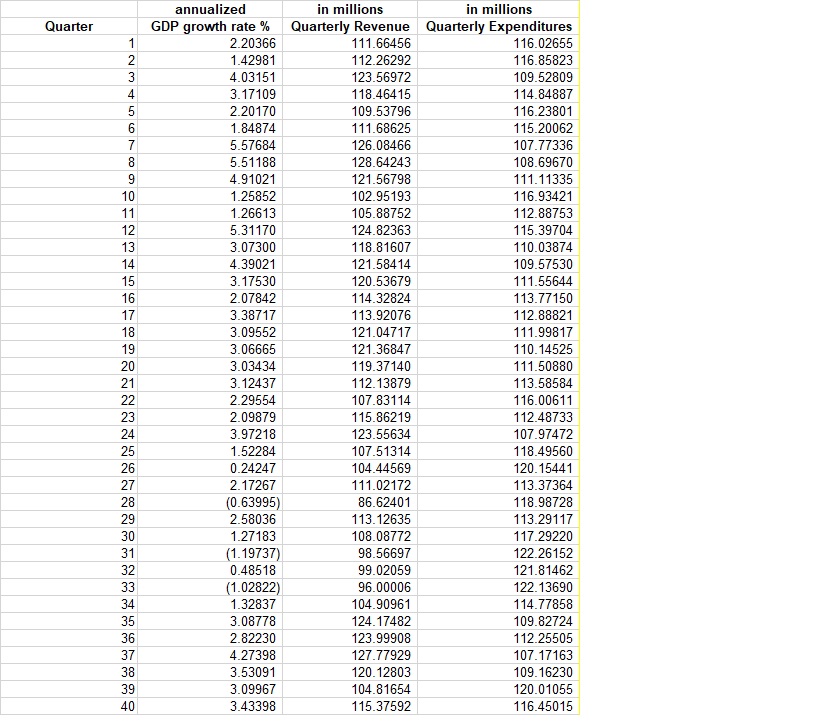

Now suppose that you run a risk management consultancy firm and you have been hired by a mid-sized municipality to help them avoid future economically-induced fiscal crises. Specifically, the municipality wants to determine to what extent their cash flows are impacted by changes in regional inflation-adjusted GDP growth rates and then to hedge that risk. To help them, you have obtained quarterly inflation-adjusted regional GDP data from Bureau of Economic Analysis (BEA). BEA reports that for the past 40 quarters real GDP for the region has grown at about 2 percent on an annualized basis. You have also obtained, from your client (the municipality), inflation-adjusted revenue and expenditure data for the past 40 calendar quarters (not annualized). You need to determine by how much a change in annualized GDP quarterly growth rates will impact the municipality's quarterly net cash flows. Net cash flow is defined as the difference between the municipality's gross revenue and gross expenditures. This data is in the spreadsheet.

You should:

Formulate a linear model and decide which is the independent variable and which is the dependent variable (i.e., GDP growth and Net Cash Flow

Expert Answer:

Fundamentals of Multinational Finance

ISBN: 978-0205989751

5th edition

Authors: Michael H. Moffett, Arthur I. Stonehill , David K. Eiteman