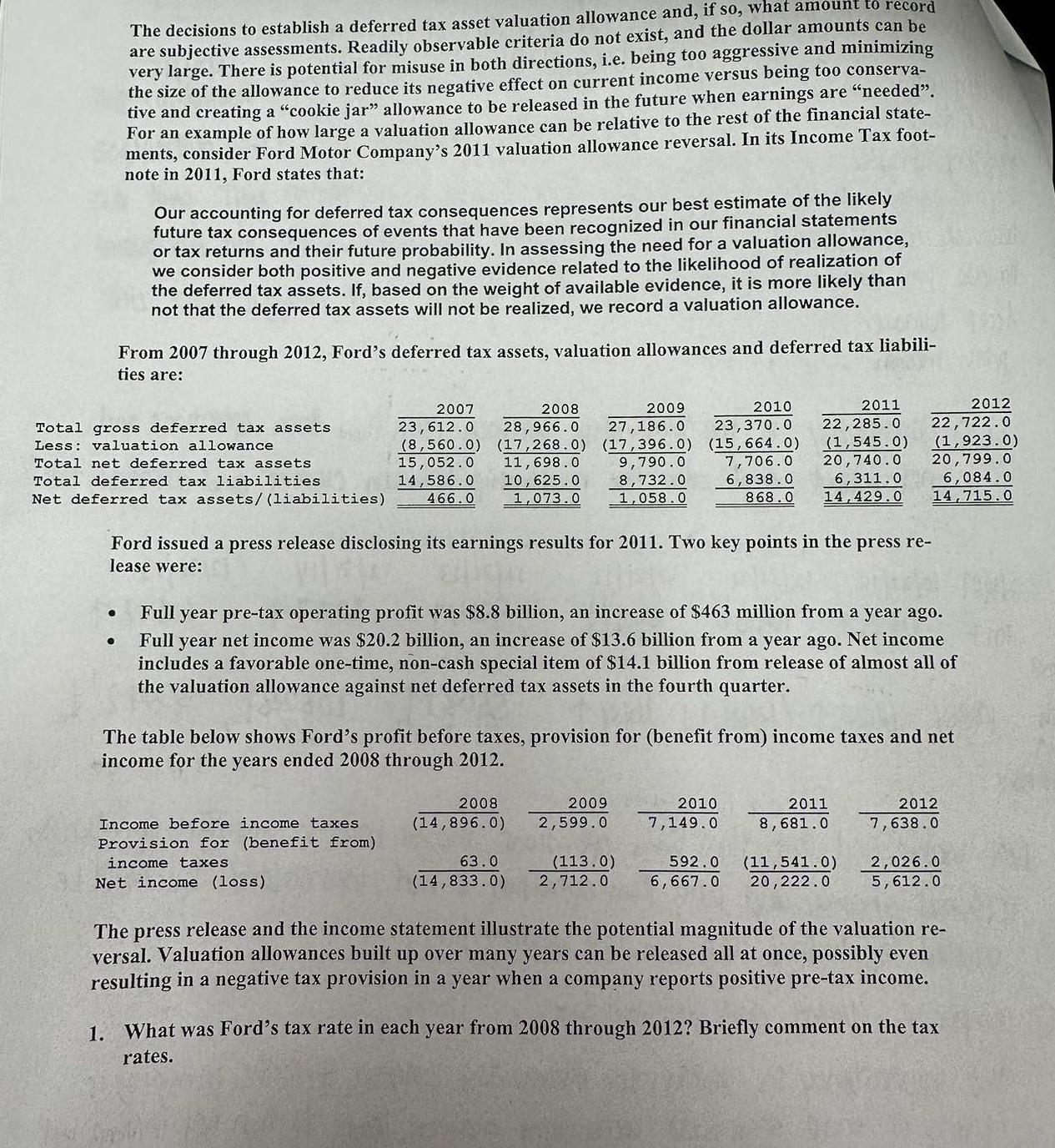

The decisions to establish a deferred tax asset valuation allowance and, if so, what amount to...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

The decisions to establish a deferred tax asset valuation allowance and, if so, what amount to record are subjective assessments. Readily observable criteria do not exist, and the dollar amounts can be very large. There is potential for misuse in both directions, i.e. being too aggressive and minimizing the size of the allowance to reduce its negative effect on current income versus being too conserva- tive and creating a "cookie jar" allowance to be released in the future when earnings are "needed". For an example of how large a valuation allowance can be relative to the rest of the financial state- ments, consider Ford Motor Company's 2011 valuation allowance reversal. In its Income Tax foot- note in 2011, Ford states that: Our accounting for deferred tax consequences represents our best estimate of the likely future tax consequences of events that have been recognized in our financial statements or tax returns and their future probability. In assessing the need for a valuation allowance, we consider both positive and negative evidence related to the likelihood of realization of the deferred tax assets. If, based on the weight of available evidence, it is more likely than not that the deferred tax assets will not be realized, we record a valuation allowance. From 2007 through 2012, Ford's deferred tax assets, valuation allowances and deferred tax liabili- ties are: 2007 Total gross deferred tax assets Less: valuation allowance Total net deferred tax assets Total deferred tax liabilities 23,612.0 2008 28,966.0 2009 2010 27,186.0 23,370.0 2011 22,285.0 2012 22,722.0 (8,560.0 (17,268.0) (17,396.0) (15,664.0) (1,545.0) (1,923.0) 15,052.0 11,698.0 9,790.0 7,706.0 20,740.0 20,799.0 14,586.0 Net deferred tax assets/ (liabilities) 466.0 10,625.0 1,073.0 8,732.0 6,838.0 6,311.0 6,084.0 1,058.0 868.0 14,429.0 14,715.0 Ford issued a press release disclosing its earnings results for 2011. Two key points in the press re- lease were: Full year pre-tax operating profit was $8.8 billion, an increase of $463 million from a year ago. Full year net income was $20.2 billion, an increase of $13.6 billion from a year ago. Net income includes a favorable one-time, non-cash special item of $14.1 billion from release of almost all of the valuation allowance against net deferred tax assets in the fourth quarter. The table below shows Ford's profit before taxes, provision for (benefit from) income taxes and net income for the years ended 2008 through 2012. Income before income taxes. Provision for (benefit from) 2008 (14,896.0) 2009 2,599.0 2010 7,149.0 2011 8,681.0 2012 7,638.0 income taxes Net income (loss) 63.0 (14,833.0) (113.0) 2,712.0 592.0 6,667.0 (11,541.0) 20,222.0 2,026.0 5,612.0 The press release and the income statement illustrate the potential magnitude of the valuation re- versal. Valuation allowances built up over many years can be released all at once, possibly even resulting in a negative tax provision in a year when a company reports positive pre-tax income. 1. What was Ford's tax rate in each year from 2008 through 2012? Briefly comment on the tax rates. The decisions to establish a deferred tax asset valuation allowance and, if so, what amount to record are subjective assessments. Readily observable criteria do not exist, and the dollar amounts can be very large. There is potential for misuse in both directions, i.e. being too aggressive and minimizing the size of the allowance to reduce its negative effect on current income versus being too conserva- tive and creating a "cookie jar" allowance to be released in the future when earnings are "needed". For an example of how large a valuation allowance can be relative to the rest of the financial state- ments, consider Ford Motor Company's 2011 valuation allowance reversal. In its Income Tax foot- note in 2011, Ford states that: Our accounting for deferred tax consequences represents our best estimate of the likely future tax consequences of events that have been recognized in our financial statements or tax returns and their future probability. In assessing the need for a valuation allowance, we consider both positive and negative evidence related to the likelihood of realization of the deferred tax assets. If, based on the weight of available evidence, it is more likely than not that the deferred tax assets will not be realized, we record a valuation allowance. From 2007 through 2012, Ford's deferred tax assets, valuation allowances and deferred tax liabili- ties are: 2007 Total gross deferred tax assets Less: valuation allowance Total net deferred tax assets Total deferred tax liabilities 23,612.0 2008 28,966.0 2009 2010 27,186.0 23,370.0 2011 22,285.0 2012 22,722.0 (8,560.0 (17,268.0) (17,396.0) (15,664.0) (1,545.0) (1,923.0) 15,052.0 11,698.0 9,790.0 7,706.0 20,740.0 20,799.0 14,586.0 Net deferred tax assets/ (liabilities) 466.0 10,625.0 1,073.0 8,732.0 6,838.0 6,311.0 6,084.0 1,058.0 868.0 14,429.0 14,715.0 Ford issued a press release disclosing its earnings results for 2011. Two key points in the press re- lease were: Full year pre-tax operating profit was $8.8 billion, an increase of $463 million from a year ago. Full year net income was $20.2 billion, an increase of $13.6 billion from a year ago. Net income includes a favorable one-time, non-cash special item of $14.1 billion from release of almost all of the valuation allowance against net deferred tax assets in the fourth quarter. The table below shows Ford's profit before taxes, provision for (benefit from) income taxes and net income for the years ended 2008 through 2012. Income before income taxes. Provision for (benefit from) 2008 (14,896.0) 2009 2,599.0 2010 7,149.0 2011 8,681.0 2012 7,638.0 income taxes Net income (loss) 63.0 (14,833.0) (113.0) 2,712.0 592.0 6,667.0 (11,541.0) 20,222.0 2,026.0 5,612.0 The press release and the income statement illustrate the potential magnitude of the valuation re- versal. Valuation allowances built up over many years can be released all at once, possibly even resulting in a negative tax provision in a year when a company reports positive pre-tax income. 1. What was Ford's tax rate in each year from 2008 through 2012? Briefly comment on the tax rates.

Expert Answer:

Related Book For

Financial Reporting Financial Statement Analysis and Valuation a strategic perspective

ISBN: 978-1337614689

9th edition

Authors: James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Posted Date:

Students also viewed these accounting questions

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

China Petroleum and Chemical Corporation China Petroleum and Chemical Corporation (CPCC) is one of a growing number of Chinese companies that has cross-listed its stock on foreign stock exchanges. To...

-

The following data have been extracted from the financial statements of Prentiss, Inc., a calendar-year merchandising corporation: Total sales for 2018 were $1,200,000 and for 2017 were $1,100,000....

-

The stable allotropic form of phosphorus is P4, in which each P atom is bonded to three other P atoms. Draw a Lewis structure of this molecule and describe its geometry. At high temperatures, P4...

-

What factors would cause an acquirer to include deferred tax assets and liabilities in the net identifiable assets acquired?

-

You use a rope of length \(\ell\) to tie the front of a \(1500-\mathrm{kg}\) truck to the rear of a \(1000-\mathrm{kg}\) car and then use an identical rope of length \(\ell\) to tie the front of the...

-

Izabela Jach opened a medical office under the name Izabela Jach, MD, on August 1, 2017. On August 31, the balance sheet showed Cash $3,000; Accounts Receivable $1,500; Supplies $600; Equipment...

-

(a) Describe the curse of dimensionality. Why does it make learning hard in high dimensional space (b) Summarize main idea(s)in PCA and what is it used for? Is PCA a supervised or an unsupervised...

-

The extent of federal government power has been an issue throughout most of US history. Competing interpretations of the 10th Amendment on one hand, and the "commerce clause" on the other, are at the...

-

Discuss the tax implications for the Rollins family if they cease to be residents of Canada.

-

What are the meaning of lodgement and signing of Tax returns ~ briefly discuss in your own way.

-

X and her sister Y, were the registered owners of a parcel of land. They executed a special power of attorney in favor of their brother, B, authorizing him to sell the property for and in their...

-

On April 1, 2025, Acme Corporation paid $48,000 cash for equipment that will be used in business operations. The equipment will be used for four years. Acme records a depreciation expense of $48,000...

-

Z Lemon Inc. is a women's shoe retailer. On February 1, 2022, the company purchased 500 pairs of "Angel" model shoes for $20 per pair. On March 3, the company purchased 700 pairs of the newly...

-

Read the case study Coca-Cola in India, and answer the following: What aspects of U.S. culture and of Indian culture may have been causes of Coke's difficulties in India?

-

On 1 July 2021, Croydon Ltd leased ten excavators for five years from Machines4U Ltd. The excavators are expected to have an economic life of 6 years, after which time they will have an expected...

-

A probability experiment consists of rolling a single fair die. (a) Identify the outcomes of the probability experiment. (b) Determine the sample space. (c) Define the event E = roll an even number....

-

Suppose that a survey asked 500 families with three children to disclose the gender of their children and found that 180 of the families had two boys and one girl. (a) Estimate the probability of...

-

Our number system consists of the digits 0, 1, 2, 3, 4, 5, 6, 7, 8, and 9. Because we do not write numbers such as 12 as 012, the first significant digit in any number must be 1, 2, 3, 4, 5, 6, 7, 8,...

Study smarter with the SolutionInn App