When a firm decides that a plant wide overhead rate is not sufficient (perhaps it makes...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

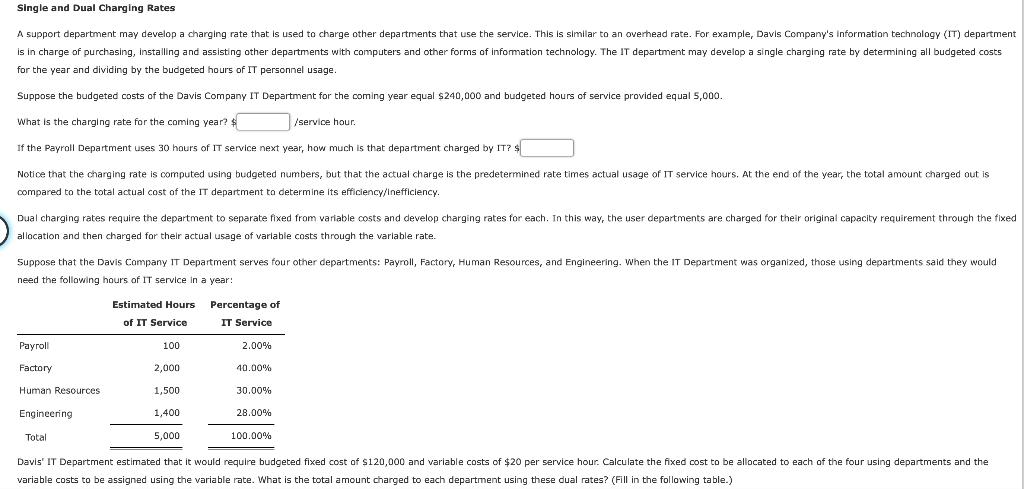

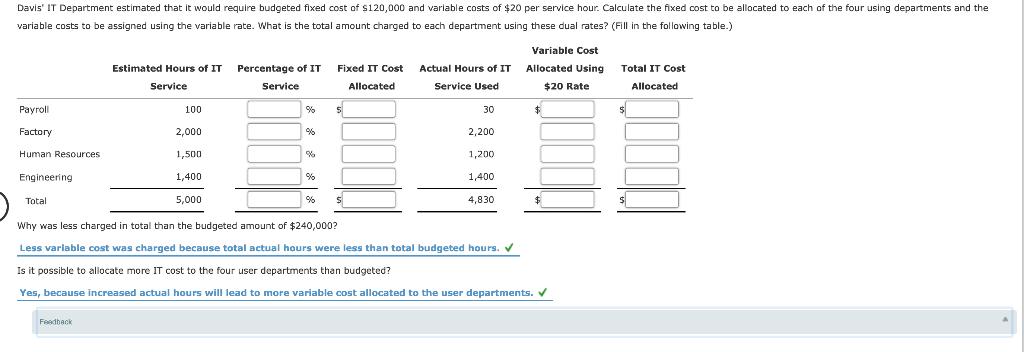

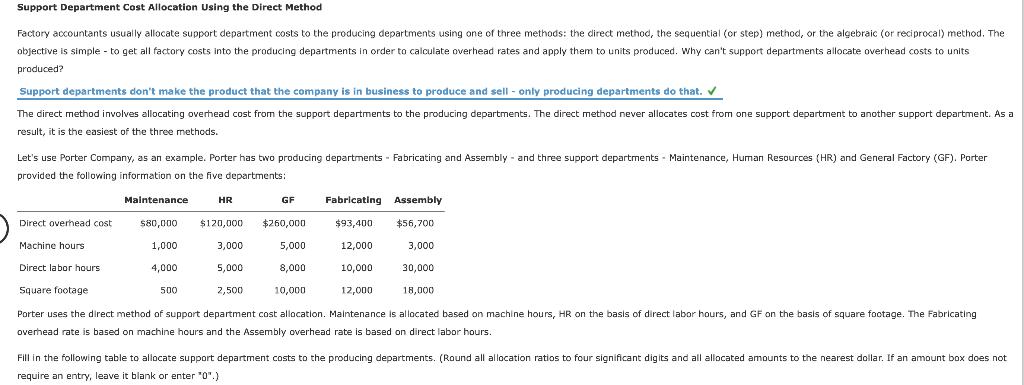

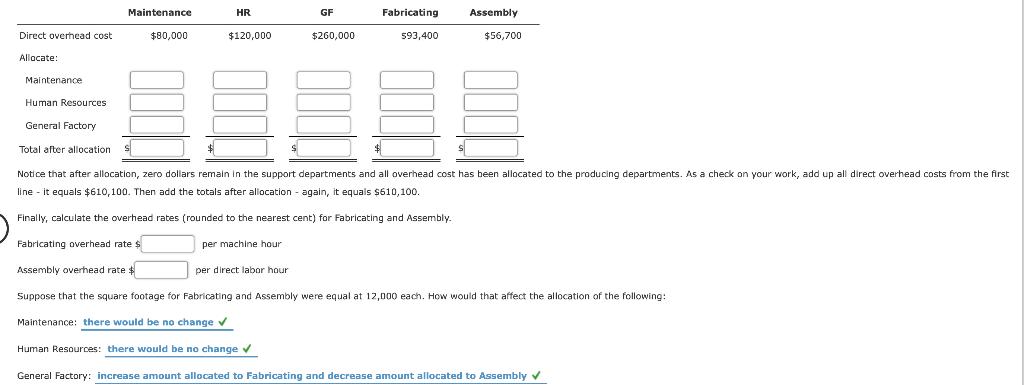

When a firm decides that a plant wide overhead rate is not sufficient (perhaps it makes multiple products and the various products go through some processes but not all), it may decide to departmentalise. The factory is divided into departments and costs are accumulated within the departments. When that is done, there are basically two types of departments: producing departments that actually make units of product, and support departments that do not make the product but assist or support the producing departments. Costs of support departments are allocated to producing departments for the following reasons: inventory valuation, product- line profitability, pricing, and planning and control.. From the list below, determine which of the following are producing departments: Departments Is it a producing department? Yes ✔ Assembly Human Resources Industrial engineering (in a bread factory) Baking (in a bread factory) Packaging Accounting (in a paint factory) Welding (in a auto manufacture) No ✓ No ✓ Yes ✓ Yes ✔ No ✓ Yes ✔ No ✓ Yes ✔ Maintenance Mixing (in a food factory) Some costs are hard to associate with a single department, so a final catch-all department may be created called General Factory. This department includes all overhead costs that could not be traced to the other departments. For example, the salary of the plant superintendent and the cost of landscaping and grounds keeping may be included in General Factory. Once the factory is departmentalized, the costs of each department are traced to that department. All costs in the support departments are overhead costs. Costs in the producing departments can include direct overhead. For example, overhead cost directly traced to a producing department may include depreciation on machinery and the salary of the departmental supervisor. Single and Dual Charging Rates A support department may develop a charging rate that is used to charge other departments that use the service. This is similar to an overhead rate. For example, Davis Company's Information technology (IT) department is in charge of purchasing, installing and assisting other departments with computers and other forms of information technology. The IT department may develop a single charging rate by determining all budgeted costs for the year and dividing by the budgeted hours of IT personnel usage. Suppose the budgeted costs of the Davis Company IT Department for the coming year equal $240,000 and budgeted hours of service provided equal 5,000. What is the charging rate for the coming year? $ /service hour. If the Payroll Department uses 30 hours of IT service next year, how much is that department charged by IT? $ Notice that the charging rate is computed using budgeted numbers, but that the actual charge is the predetermined rate times actual usage of IT service hours. At the end of the year, the total amount charged out is compared to the total actual cost of the IT department to determine its efficiency/Inefficiency. Dual charging rates require the department to separate fixed from variable costs and develop charging rates for each. In this way, the user departments are charged for their original capacity requirement through the fixed. allocation and then charged for their actual usage of variable costs through the variable rate. Suppose that the Davis Company IT Department serves four other departments: Payroll, Factory, Human Resources, and Engineering. When the IT Department was organized, those using departments said they would need the following hours of IT service in a year: Payroll Factory Human Resources. Engineering. Estimated Hours of IT Service 100 2,000 1,500 1,400 Total Percentage of IT Service 2.00% 40.00% 30.00% 28.00% 5,000 Davis' IT Department estimated that it would require budgeted fixed cost of $120,000 and variable costs of $20 per service hour. Calculate the fixed cost to be allocated to each of the four using departments and the variable costs to be assigned using the variable rate. What is the total amount charged to each department using these dual rates? (Fill in the following table.) 100.00% Davis' IT Department estimated that it would require budgeted fixed cost of $120,000 and variable costs of $20 per service hour. Calculate the fixed cost to be allocated to each of the four using departments and the variable costs to be assigned using the variable rate. What is the total amount charged to each department using these dual rates? (Fill in the following table.) Payroll Factory Human Resources Engineering Total Estimated Hours of IT Service Feedback 100 2,000 1,500 1,400 5,000 Percentage of IT Service % % % % % Fixed IT Cost Allocated 5 Actual Hours of IT Service Used 30 2,200 1,200 1,400 4,830 Variable Cost Allocated Using $20 Rate $ Why was less charged in total than the budgeted amount of $240,000? Less variable cost was charged because total actual hours were less than total budgeted hours. ✓ Is it possible to allocate more IT cost to the four user departments than budgeted? Yes, because increased actual hours will lead to more variable cost allocated to the user departments. ✓ Total IT Cost Allocated Support Department Cost Allocation Using the Direct Method Factory accountants usually allocate support department costs to the producing departments using one of three methods: the direct method, the sequential (or step) method, or the algebraic (or reciprocal) method. The objective is simple to get all factory costs into the producing departments in order to calculate overhead rates and apply them to units produced. Why can't support departments allocate overhead costs to units produced? Support departments don't make the product that the company is in business to produce and sell only producing departments do that. ✔ The direct method involves allocating overhead cost from the support departments to the producing departments. The direct method never allocates cost from one support department another support department. As a result, it is the easiest of the three methods. Let's use Porter Company, as an example. Porter has two producing departments Fabricating and Assembly and three support departments Maintenance, Human Resources (HR) and General Factory (GF). Porter provided the following information on the five departments: Direct overhead cost. Machine hours Maintenance $80,000 1,000 4,000 500 HR GF $120,000 $260,000 3,000 5,000 2,500 5,000 8,000 Fabricating Assembly $93,400. $56,700 12,000 10,000 10,000 3,000 Direct labor hours Square footage 18,000 Porter uses the direct method of support department cost allocation. Maintenance is allocated based on machine hours, HR on the basis of direct labor hours, and GF on the basis of square footage. The Fabricating overhead rate is based on machine hours and the Assembly overhead rate is based on direct labor hours. 12,000 - 30,000 Fill in the following table to allocate support department costs to the producing departments. (Round all allocation ratios to four significant digits and all allocated amounts to the nearest dollar. If an amount box does not require an entry, leave it blank or enter "0".) Direct overhead cost Allocate: Maintenance Human Resources General Factory Maintenance $80,000 $ HR $120,000 GF per machine hour $260,000 $ Fabricating $93,400 Assembly $56,700 Total after allocation Notice that after allocation, zero dollars remain in the support departments and all overhead cost has been allocated to the producing departments. As a check on your work, add up all direct overhead costs from the first line - it equals $610,100. Then add the totals after allocation - again, it equals $610,100. Finally, calculate the overhead rates (rounded to the nearest cent) for Fabricating and Assembly. Fabricating overhead rate $ Assembly overhead rate $ per direct labor hour Suppose that the square footage for Fabricating and Assembly were equal at 12,000 each. How would that affect the allocation of the following: Maintenance: there would be no change ✓ Human Resources: there would be no change ✔ General Factory: increase amount allocated to Fabricating and decrease amount allocated to Assembly ✓ When a firm decides that a plant wide overhead rate is not sufficient (perhaps it makes multiple products and the various products go through some processes but not all), it may decide to departmentalise. The factory is divided into departments and costs are accumulated within the departments. When that is done, there are basically two types of departments: producing departments that actually make units of product, and support departments that do not make the product but assist or support the producing departments. Costs of support departments are allocated to producing departments for the following reasons: inventory valuation, product- line profitability, pricing, and planning and control.. From the list below, determine which of the following are producing departments: Departments Is it a producing department? Yes ✔ Assembly Human Resources Industrial engineering (in a bread factory) Baking (in a bread factory) Packaging Accounting (in a paint factory) Welding (in a auto manufacture) No ✓ No ✓ Yes ✓ Yes ✔ No ✓ Yes ✔ No ✓ Yes ✔ Maintenance Mixing (in a food factory) Some costs are hard to associate with a single department, so a final catch-all department may be created called General Factory. This department includes all overhead costs that could not be traced to the other departments. For example, the salary of the plant superintendent and the cost of landscaping and grounds keeping may be included in General Factory. Once the factory is departmentalized, the costs of each department are traced to that department. All costs in the support departments are overhead costs. Costs in the producing departments can include direct overhead. For example, overhead cost directly traced to a producing department may include depreciation on machinery and the salary of the departmental supervisor. Single and Dual Charging Rates A support department may develop a charging rate that is used to charge other departments that use the service. This is similar to an overhead rate. For example, Davis Company's Information technology (IT) department is in charge of purchasing, installing and assisting other departments with computers and other forms of information technology. The IT department may develop a single charging rate by determining all budgeted costs for the year and dividing by the budgeted hours of IT personnel usage. Suppose the budgeted costs of the Davis Company IT Department for the coming year equal $240,000 and budgeted hours of service provided equal 5,000. What is the charging rate for the coming year? $ /service hour. If the Payroll Department uses 30 hours of IT service next year, how much is that department charged by IT? $ Notice that the charging rate is computed using budgeted numbers, but that the actual charge is the predetermined rate times actual usage of IT service hours. At the end of the year, the total amount charged out is compared to the total actual cost of the IT department to determine its efficiency/Inefficiency. Dual charging rates require the department to separate fixed from variable costs and develop charging rates for each. In this way, the user departments are charged for their original capacity requirement through the fixed. allocation and then charged for their actual usage of variable costs through the variable rate. Suppose that the Davis Company IT Department serves four other departments: Payroll, Factory, Human Resources, and Engineering. When the IT Department was organized, those using departments said they would need the following hours of IT service in a year: Payroll Factory Human Resources. Engineering. Estimated Hours of IT Service 100 2,000 1,500 1,400 Total Percentage of IT Service 2.00% 40.00% 30.00% 28.00% 5,000 Davis' IT Department estimated that it would require budgeted fixed cost of $120,000 and variable costs of $20 per service hour. Calculate the fixed cost to be allocated to each of the four using departments and the variable costs to be assigned using the variable rate. What is the total amount charged to each department using these dual rates? (Fill in the following table.) 100.00% Davis' IT Department estimated that it would require budgeted fixed cost of $120,000 and variable costs of $20 per service hour. Calculate the fixed cost to be allocated to each of the four using departments and the variable costs to be assigned using the variable rate. What is the total amount charged to each department using these dual rates? (Fill in the following table.) Payroll Factory Human Resources Engineering Total Estimated Hours of IT Service Feedback 100 2,000 1,500 1,400 5,000 Percentage of IT Service % % % % % Fixed IT Cost Allocated 5 Actual Hours of IT Service Used 30 2,200 1,200 1,400 4,830 Variable Cost Allocated Using $20 Rate $ Why was less charged in total than the budgeted amount of $240,000? Less variable cost was charged because total actual hours were less than total budgeted hours. ✓ Is it possible to allocate more IT cost to the four user departments than budgeted? Yes, because increased actual hours will lead to more variable cost allocated to the user departments. ✓ Total IT Cost Allocated Support Department Cost Allocation Using the Direct Method Factory accountants usually allocate support department costs to the producing departments using one of three methods: the direct method, the sequential (or step) method, or the algebraic (or reciprocal) method. The objective is simple to get all factory costs into the producing departments in order to calculate overhead rates and apply them to units produced. Why can't support departments allocate overhead costs to units produced? Support departments don't make the product that the company is in business to produce and sell only producing departments do that. ✔ The direct method involves allocating overhead cost from the support departments to the producing departments. The direct method never allocates cost from one support department another support department. As a result, it is the easiest of the three methods. Let's use Porter Company, as an example. Porter has two producing departments Fabricating and Assembly and three support departments Maintenance, Human Resources (HR) and General Factory (GF). Porter provided the following information on the five departments: Direct overhead cost. Machine hours Maintenance $80,000 1,000 4,000 500 HR GF $120,000 $260,000 3,000 5,000 2,500 5,000 8,000 Fabricating Assembly $93,400. $56,700 12,000 10,000 10,000 3,000 Direct labor hours Square footage 18,000 Porter uses the direct method of support department cost allocation. Maintenance is allocated based on machine hours, HR on the basis of direct labor hours, and GF on the basis of square footage. The Fabricating overhead rate is based on machine hours and the Assembly overhead rate is based on direct labor hours. 12,000 - 30,000 Fill in the following table to allocate support department costs to the producing departments. (Round all allocation ratios to four significant digits and all allocated amounts to the nearest dollar. If an amount box does not require an entry, leave it blank or enter "0".) Direct overhead cost Allocate: Maintenance Human Resources General Factory Maintenance $80,000 $ HR $120,000 GF per machine hour $260,000 $ Fabricating $93,400 Assembly $56,700 Total after allocation Notice that after allocation, zero dollars remain in the support departments and all overhead cost has been allocated to the producing departments. As a check on your work, add up all direct overhead costs from the first line - it equals $610,100. Then add the totals after allocation - again, it equals $610,100. Finally, calculate the overhead rates (rounded to the nearest cent) for Fabricating and Assembly. Fabricating overhead rate $ Assembly overhead rate $ per direct labor hour Suppose that the square footage for Fabricating and Assembly were equal at 12,000 each. How would that affect the allocation of the following: Maintenance: there would be no change ✓ Human Resources: there would be no change ✔ General Factory: increase amount allocated to Fabricating and decrease amount allocated to Assembly ✓

Expert Answer:

Related Book For

Posted Date:

Students also viewed these accounting questions

-

The estimated departmental overhead for producing departments S and T and the estimated costs of service departments E, F, and G (before any service department distributions) are: The interdependence...

-

The product costs reported using either plant wide or department allocation are the same. The only difference is in the number of cost drivers used. True or false? Explain.

-

A manufacturing firm produces two products. Each product must go through an assembly process and a finishing process. The product is then transferred to the warehouse, which has space for only a...

-

1. The Jarmon Company manufactures and sells a line of exclusive sportswear. Prepare a financial position as at 31st December 2022 from the following information. Account Receivable Long term loan...

-

What would a person who wishes to sell goods to an individual in Lebanon have to do before shipping goods to that person?

-

What is cultural relativism, and is it the same as moral relativism?

-

Lockridge-Priest, Inc., was organized in 2008. At December 31, 2008, the Lockridge-Priest balance sheet reported the following stockholders' equity: Requirements 1. During 2009 , the company...

-

Capacitance of an Oscilloscope Oscilloscopes has parallel metal plates inside them to deflect the electron beam. These plates are called the deflecting plates. Typically, they are squares 3.0 cm on a...

-

12.1 Cutler Limited had two shareholders, Arthur and Barry, who owned the company in equal proportions. Arthur bought all of Barry's shares and became the sole owner of the company. As part of the...

-

Solve the following modifications of the capital budgeting model in Figure 6.5. (Solve each part independently of the others.) a. Suppose that at most two of projects 3, 5, and 6 can be selected. b....

-

Target Corporation believed it could increase the companys profits by closing its stores in Canada. Other companies have also tried to improve their financial performance by downsizing. In November...

-

Use what you have learned in the module to analyze the quote below. Make sure to address each point in complete sentences. "In this world, nothing is certain but death and taxes." -Benjamin Franklin...

-

Tina Catchings has just started her study of accounting. She is finding that the hardest part of understanding accounting is learning what all of the terms mean. For example, Tina is interested in...

-

Divide and simplify. x-18x+81 x2-81 x-x-72 + 3

-

There is a mound of g pounds of gravel in a quarry. Throughout the day,2 75 pounds of gravel are added to the mound. Two orders of 720 pounds are sold and the gravel is removed from the mound. At the...

-

Factor out the GCF. 10a5b5+2ab3-16ab5 10a5b5+2ab3-16ab5 -16ab5 = (Factor completely.)

-

Define the manufacturers role in the fashion industry. In your definition, include a comparison of limited-function wholesalers and full-function wholesalers. Define licensing and discuss how it has...

-

In Problems, solve each system of equations. x + 2y + 3z = 5 y + 11z = 21 5y + 9z = 13

-

What is a capital gain? When are capital gains taxes levied? May capital losses be used to offset capital gains and income from other sources?

-

1. The differences between collecting and investing in baseball cards and investing in commodities. 2. The tax implications (if any) of redeeming the mutual fund shares, closing the bank account, or...

-

What is a nations cash inflow (outflow) on its current account and its capital account, given the following information? Was there a net currency inflow or outflow? Imports ............... $245...

-

Review the sample scope statement in this chapter. Assume you are responsible for planning and then managing the deliverable called survey development. What additional information would you want to...

-

You are part of a team in charge of a project to help people in your company (500 people) lose weight. This project is part of a competition, and the top losers will be featured in a popular...

-

Your organization initiated a project to raise money for an important charity. Assume that there are 1,000 people in your organization. Also assume that you have six months to raise as much money as...

Study smarter with the SolutionInn App