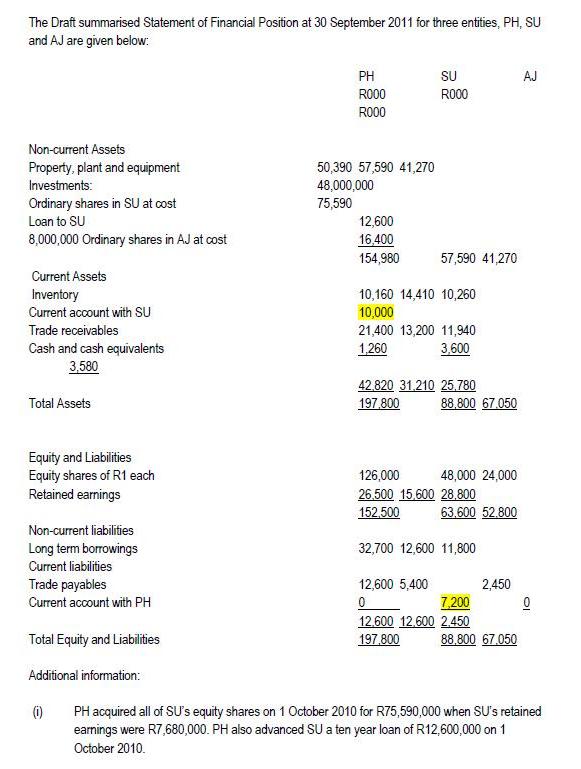

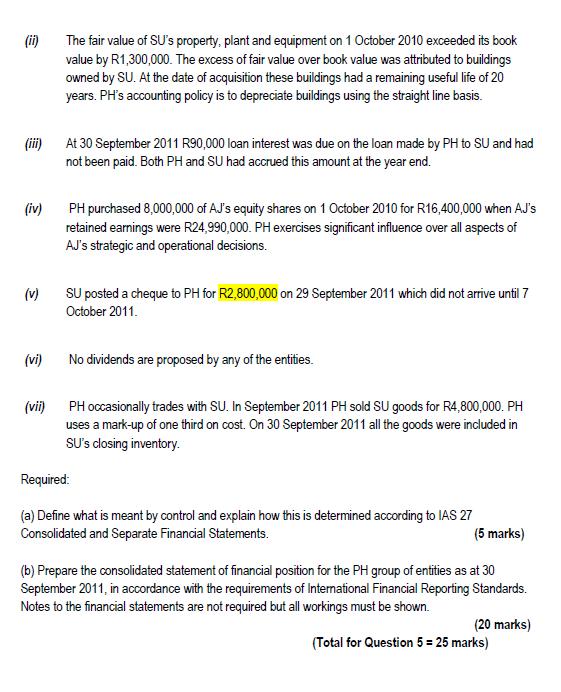

The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks)

Expert Answer:

Answer rating: 100% (QA)

AnsaControl is defined by IFRS 10 as follows An investor controls an investee when the investor is e... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

The comparative consolidated statement of financial position at December 31, Year 2, and the consolidated income statement for Year 2, of Parent Ltd. and its 70%-owned subsidiary are shown below....

-

Ayayai tnc. reported the following partial income statement data for the years ended December 31, 2018, and 2017: 2010 2017 Sales $267,000 $242,000 Cost of gonds sold 208,000 189,244 Gruss profit...

-

The comparative unclassified statement of financial position for Puffy Ltd. follows: Additional information: 1. Net income was $115,000. 2. Sales were $978,000. 3. Cost of goods sold was $751,000. 4....

-

Refer to the following lease amortization schedule. The 10 payments are made annually starting with the inception Of the lease. Title does not transfer to the lessee and there is no bargain purchase...

-

One of the ways to evaluate the ease of navigating a corporate website is to measure how long it takes to reach the link where you can view or download the companys most recent annual report. In...

-

For each of the two preliminary audit strategies, state the appropriate levels of (1) planned detection risk and (2) substantive tests.

-

Find the area to the right of 29.141 under the chi-square distribution with 14 degrees of freedom.

-

A single-pass, cross-flow heat exchanger with both fluids unmixed is being used to heat water (m c = 2 kg/s. c p = 4200 J/kg K) from 20C to 100C with hot exhaust gases (c p = 1200 J/kg K) entering...

-

Joan Hill, President of Hill & Hill Pens, was looking forward to receiving the company's second quarter income statement. She knew that the sales budget of 20,000 units sold had been met during the...

-

SAE specifications call for the low-side R-134a servicehose to be A) Solid blue with a black stripe B) Solid blue with no stripe C) Solid blue with a yellow stripe D) Solid black with a blue stripe...

-

John's friend Tim is injured in a car accident. John was not involved in the accident, but he wants to pursue a lawsuit on Tim's behalf to recover for Tim's injuries. Tim is not related to John, and...

-

What would be the result if a new state modified a decree where the decree state had continuing jurisdiction?

-

Do you think postmarital contracts avoid some of the problems associated with premarital contracts? Do they present other potential difficulties?

-

What are the four jurisdictional bases under the UCCJEA and PKPA? Why were these laws enacted?

-

Do you think premarital agreements denigrate the meaning of marriage by making it more like a commercial transaction?

-

Traditionally, what has been the basis for the exercise of jurisdiction over a child custody dispute? What problems did this create?

-

Whirly Corporation's contribution format income statement for the most recent month is shown below: Sales (7,400 units) Total Variable expenses $ 229,400 140,600 Contribution margin 88,800 Per Unit $...

-

A business had revenues of $280,000 and operating expenses of $315,000. Did the business (a) Incur a net loss (b) Realize net income?

-

Identify the phases in the joint conceptual framework project. What two phases are expect to be completed earliest?

-

What are the basic elements of the framework? Briefly describe the relationship between the moment in time and period of time elements?

-

Explain the role of the international financial Reporting Interpretations Committee.

-

Suppose the US investor in Question 8 were risk averse, instead of risk neutral, and wants a risk premium of \(1 \%\) (annual) for assuming the exchange-rate risk on the international investment. a....

-

When there is a concentration gradient in the system, show that the potential gradient is composed of two terms, (i) an Ohm's-law contribution and (ii) a diffusional contribution. State the equation...

-

Copper is deposited at a cathode from solution with a bulk concentration of \(0.5 \mathrm{M}\) at the rate of \(3.0 \mathrm{~g} / \mathrm{m}^{2} \cdot \mathrm{s}\). Find the surface concentration of...

Study smarter with the SolutionInn App