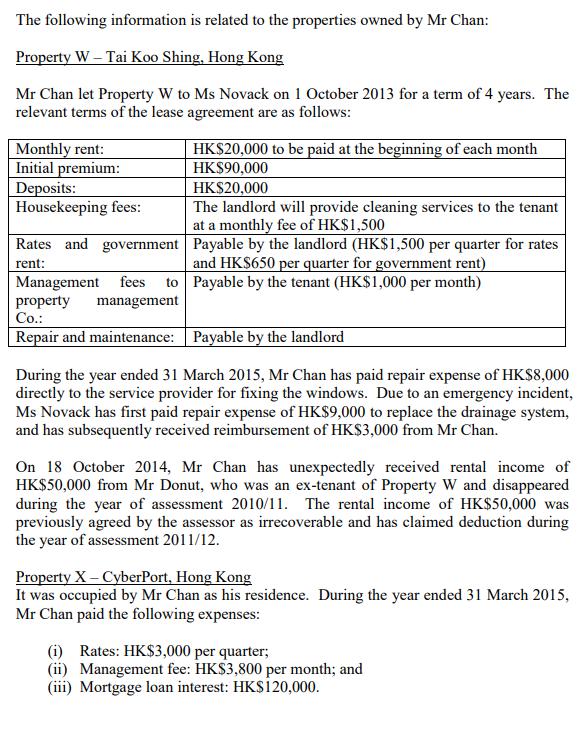

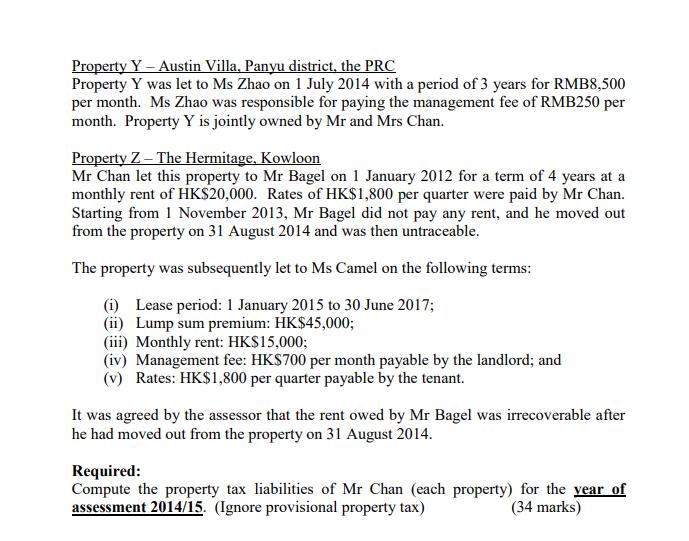

The following information is related to the properties owned by Mr Chan: Property W Tai...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

The following information is related to the properties owned by Mr Chan: Property W – Tai Koo Shing, Hong Kong Mr Chan let Property W to Ms Novack on 1 October 2013 for a term of 4 years. The relevant terms of the lease agreement are as follows: Monthly rent: Initial premium: Deposits: Housekeeping fees: HK$20,000 to be paid at the beginning of each month HKS90,000 HK$20,000 The landlord will provide cleaning services to the tenant at a monthly fee of HK$1,500 Rates and government Payable by the landlord (HK$1,500 per quarter for rates and HKS650 per quarter for government rent) to Payable by the tenant (HK$1,000 per month) rent: Management fees property Co.: management Repair and maintenance: Payable by the landlord During the year ended 31 March 2015, Mr Chan has paid repair expense of HKS8,000 directly to the service provider for fixing the windows. Due to an emergency incident, Ms Novack has first paid repair expense of HK$9,000 to replace the drainage system, and has subsequently received reimbursement of HK$3,000 from Mr Chan. On 18 October 2014, Mr Chan has unexpectedly received rental income of HK$50,000 from Mr Donut, who was an ex-tenant of Property W and disappeared during the year of assessment 2010/11. The rental income of HK$50,000 was previously agreed by the assessor as irrecoverable and has claimed deduction during the year of assessment 2011/12. Property X – CyberPort, Hong Kong It was occupied by Mr Chan as his residence. During the year ended 31 March 2015, Mr Chan paid the following expenses: (i) Rates: HK$3,000 per quarter; (ii) Management fee: HKS3,800 per month; and (iii) Mortgage loan interest: HKS120,000. Property Y – Austin Villa, Panyu district, the PRC Property Y was let to Ms Zhao on 1 July 2014 with a period of 3 years for RMB8,500 per month. Ms Zhao was responsible for paying the management fee of RMB250 per month. Property Y is jointly owned by Mr and Mrs Chan. Property Z – The Hermitage, Kowloon Mr Chan let this property to Mr Bagel on 1 January 2012 for a term of 4 years at a monthly rent of HK$20,000. Rates of HK$1,800 per quarter were paid by Mr Chan. Starting from 1 November 2013, Mr Bagel did not pay any rent, and he moved out from the property on 31 August 2014 and was then untraceable. The property was subsequently let to Ms Camel on the following terms: (i) Lease period: 1 January 2015 to 30 June 2017; (ii) Lump sum premium: HK$45,000; (iii) Monthly rent: HK$15,000; (iv) Management fee: HKS700 per month payable by the landlord; and (v) Rates: HK$1,800 per quarter payable by the tenant. It was agreed by the assessor that the rent owed by Mr Bagel was irrecoverable after he had moved out from the property on 31 August 2014. Required: Compute the property tax liabilities of Mr Chan (each property) for the year of assessment 2014/15. (Ignore provisional property tax) (34 marks) The following information is related to the properties owned by Mr Chan: Property W – Tai Koo Shing, Hong Kong Mr Chan let Property W to Ms Novack on 1 October 2013 for a term of 4 years. The relevant terms of the lease agreement are as follows: Monthly rent: Initial premium: Deposits: Housekeeping fees: HK$20,000 to be paid at the beginning of each month HKS90,000 HK$20,000 The landlord will provide cleaning services to the tenant at a monthly fee of HK$1,500 Rates and government Payable by the landlord (HK$1,500 per quarter for rates and HKS650 per quarter for government rent) to Payable by the tenant (HK$1,000 per month) rent: Management fees property Co.: management Repair and maintenance: Payable by the landlord During the year ended 31 March 2015, Mr Chan has paid repair expense of HKS8,000 directly to the service provider for fixing the windows. Due to an emergency incident, Ms Novack has first paid repair expense of HK$9,000 to replace the drainage system, and has subsequently received reimbursement of HK$3,000 from Mr Chan. On 18 October 2014, Mr Chan has unexpectedly received rental income of HK$50,000 from Mr Donut, who was an ex-tenant of Property W and disappeared during the year of assessment 2010/11. The rental income of HK$50,000 was previously agreed by the assessor as irrecoverable and has claimed deduction during the year of assessment 2011/12. Property X – CyberPort, Hong Kong It was occupied by Mr Chan as his residence. During the year ended 31 March 2015, Mr Chan paid the following expenses: (i) Rates: HK$3,000 per quarter; (ii) Management fee: HKS3,800 per month; and (iii) Mortgage loan interest: HKS120,000. Property Y – Austin Villa, Panyu district, the PRC Property Y was let to Ms Zhao on 1 July 2014 with a period of 3 years for RMB8,500 per month. Ms Zhao was responsible for paying the management fee of RMB250 per month. Property Y is jointly owned by Mr and Mrs Chan. Property Z – The Hermitage, Kowloon Mr Chan let this property to Mr Bagel on 1 January 2012 for a term of 4 years at a monthly rent of HK$20,000. Rates of HK$1,800 per quarter were paid by Mr Chan. Starting from 1 November 2013, Mr Bagel did not pay any rent, and he moved out from the property on 31 August 2014 and was then untraceable. The property was subsequently let to Ms Camel on the following terms: (i) Lease period: 1 January 2015 to 30 June 2017; (ii) Lump sum premium: HK$45,000; (iii) Monthly rent: HK$15,000; (iv) Management fee: HKS700 per month payable by the landlord; and (v) Rates: HK$1,800 per quarter payable by the tenant. It was agreed by the assessor that the rent owed by Mr Bagel was irrecoverable after he had moved out from the property on 31 August 2014. Required: Compute the property tax liabilities of Mr Chan (each property) for the year of assessment 2014/15. (Ignore provisional property tax) (34 marks) The following information is related to the properties owned by Mr Chan: Property W – Tai Koo Shing, Hong Kong Mr Chan let Property W to Ms Novack on 1 October 2013 for a term of 4 years. The relevant terms of the lease agreement are as follows: Monthly rent: Initial premium: Deposits: Housekeeping fees: HK$20,000 to be paid at the beginning of each month HKS90,000 HK$20,000 The landlord will provide cleaning services to the tenant at a monthly fee of HK$1,500 Rates and government Payable by the landlord (HK$1,500 per quarter for rates and HKS650 per quarter for government rent) to Payable by the tenant (HK$1,000 per month) rent: Management fees property Co.: management Repair and maintenance: Payable by the landlord During the year ended 31 March 2015, Mr Chan has paid repair expense of HKS8,000 directly to the service provider for fixing the windows. Due to an emergency incident, Ms Novack has first paid repair expense of HK$9,000 to replace the drainage system, and has subsequently received reimbursement of HK$3,000 from Mr Chan. On 18 October 2014, Mr Chan has unexpectedly received rental income of HK$50,000 from Mr Donut, who was an ex-tenant of Property W and disappeared during the year of assessment 2010/11. The rental income of HK$50,000 was previously agreed by the assessor as irrecoverable and has claimed deduction during the year of assessment 2011/12. Property X – CyberPort, Hong Kong It was occupied by Mr Chan as his residence. During the year ended 31 March 2015, Mr Chan paid the following expenses: (i) Rates: HK$3,000 per quarter; (ii) Management fee: HKS3,800 per month; and (iii) Mortgage loan interest: HKS120,000. Property Y – Austin Villa, Panyu district, the PRC Property Y was let to Ms Zhao on 1 July 2014 with a period of 3 years for RMB8,500 per month. Ms Zhao was responsible for paying the management fee of RMB250 per month. Property Y is jointly owned by Mr and Mrs Chan. Property Z – The Hermitage, Kowloon Mr Chan let this property to Mr Bagel on 1 January 2012 for a term of 4 years at a monthly rent of HK$20,000. Rates of HK$1,800 per quarter were paid by Mr Chan. Starting from 1 November 2013, Mr Bagel did not pay any rent, and he moved out from the property on 31 August 2014 and was then untraceable. The property was subsequently let to Ms Camel on the following terms: (i) Lease period: 1 January 2015 to 30 June 2017; (ii) Lump sum premium: HK$45,000; (iii) Monthly rent: HK$15,000; (iv) Management fee: HKS700 per month payable by the landlord; and (v) Rates: HK$1,800 per quarter payable by the tenant. It was agreed by the assessor that the rent owed by Mr Bagel was irrecoverable after he had moved out from the property on 31 August 2014. Required: Compute the property tax liabilities of Mr Chan (each property) for the year of assessment 2014/15. (Ignore provisional property tax) (34 marks) The following information is related to the properties owned by Mr Chan: Property W – Tai Koo Shing, Hong Kong Mr Chan let Property W to Ms Novack on 1 October 2013 for a term of 4 years. The relevant terms of the lease agreement are as follows: Monthly rent: Initial premium: Deposits: Housekeeping fees: HK$20,000 to be paid at the beginning of each month HKS90,000 HK$20,000 The landlord will provide cleaning services to the tenant at a monthly fee of HK$1,500 Rates and government Payable by the landlord (HK$1,500 per quarter for rates and HKS650 per quarter for government rent) to Payable by the tenant (HK$1,000 per month) rent: Management fees property Co.: management Repair and maintenance: Payable by the landlord During the year ended 31 March 2015, Mr Chan has paid repair expense of HKS8,000 directly to the service provider for fixing the windows. Due to an emergency incident, Ms Novack has first paid repair expense of HK$9,000 to replace the drainage system, and has subsequently received reimbursement of HK$3,000 from Mr Chan. On 18 October 2014, Mr Chan has unexpectedly received rental income of HK$50,000 from Mr Donut, who was an ex-tenant of Property W and disappeared during the year of assessment 2010/11. The rental income of HK$50,000 was previously agreed by the assessor as irrecoverable and has claimed deduction during the year of assessment 2011/12. Property X – CyberPort, Hong Kong It was occupied by Mr Chan as his residence. During the year ended 31 March 2015, Mr Chan paid the following expenses: (i) Rates: HK$3,000 per quarter; (ii) Management fee: HKS3,800 per month; and (iii) Mortgage loan interest: HKS120,000. Property Y – Austin Villa, Panyu district, the PRC Property Y was let to Ms Zhao on 1 July 2014 with a period of 3 years for RMB8,500 per month. Ms Zhao was responsible for paying the management fee of RMB250 per month. Property Y is jointly owned by Mr and Mrs Chan. Property Z – The Hermitage, Kowloon Mr Chan let this property to Mr Bagel on 1 January 2012 for a term of 4 years at a monthly rent of HK$20,000. Rates of HK$1,800 per quarter were paid by Mr Chan. Starting from 1 November 2013, Mr Bagel did not pay any rent, and he moved out from the property on 31 August 2014 and was then untraceable. The property was subsequently let to Ms Camel on the following terms: (i) Lease period: 1 January 2015 to 30 June 2017; (ii) Lump sum premium: HK$45,000; (iii) Monthly rent: HK$15,000; (iv) Management fee: HKS700 per month payable by the landlord; and (v) Rates: HK$1,800 per quarter payable by the tenant. It was agreed by the assessor that the rent owed by Mr Bagel was irrecoverable after he had moved out from the property on 31 August 2014. Required: Compute the property tax liabilities of Mr Chan (each property) for the year of assessment 2014/15. (Ignore provisional property tax) (34 marks) The following information is related to the properties owned by Mr Chan: Property W – Tai Koo Shing, Hong Kong Mr Chan let Property W to Ms Novack on 1 October 2013 for a term of 4 years. The relevant terms of the lease agreement are as follows: Monthly rent: Initial premium: Deposits: Housekeeping fees: HK$20,000 to be paid at the beginning of each month HKS90,000 HK$20,000 The landlord will provide cleaning services to the tenant at a monthly fee of HK$1,500 Rates and government Payable by the landlord (HK$1,500 per quarter for rates and HKS650 per quarter for government rent) to Payable by the tenant (HK$1,000 per month) rent: Management fees property Co.: management Repair and maintenance: Payable by the landlord During the year ended 31 March 2015, Mr Chan has paid repair expense of HKS8,000 directly to the service provider for fixing the windows. Due to an emergency incident, Ms Novack has first paid repair expense of HK$9,000 to replace the drainage system, and has subsequently received reimbursement of HK$3,000 from Mr Chan. On 18 October 2014, Mr Chan has unexpectedly received rental income of HK$50,000 from Mr Donut, who was an ex-tenant of Property W and disappeared during the year of assessment 2010/11. The rental income of HK$50,000 was previously agreed by the assessor as irrecoverable and has claimed deduction during the year of assessment 2011/12. Property X – CyberPort, Hong Kong It was occupied by Mr Chan as his residence. During the year ended 31 March 2015, Mr Chan paid the following expenses: (i) Rates: HK$3,000 per quarter; (ii) Management fee: HKS3,800 per month; and (iii) Mortgage loan interest: HKS120,000. Property Y – Austin Villa, Panyu district, the PRC Property Y was let to Ms Zhao on 1 July 2014 with a period of 3 years for RMB8,500 per month. Ms Zhao was responsible for paying the management fee of RMB250 per month. Property Y is jointly owned by Mr and Mrs Chan. Property Z – The Hermitage, Kowloon Mr Chan let this property to Mr Bagel on 1 January 2012 for a term of 4 years at a monthly rent of HK$20,000. Rates of HK$1,800 per quarter were paid by Mr Chan. Starting from 1 November 2013, Mr Bagel did not pay any rent, and he moved out from the property on 31 August 2014 and was then untraceable. The property was subsequently let to Ms Camel on the following terms: (i) Lease period: 1 January 2015 to 30 June 2017; (ii) Lump sum premium: HK$45,000; (iii) Monthly rent: HK$15,000; (iv) Management fee: HKS700 per month payable by the landlord; and (v) Rates: HK$1,800 per quarter payable by the tenant. It was agreed by the assessor that the rent owed by Mr Bagel was irrecoverable after he had moved out from the property on 31 August 2014. Required: Compute the property tax liabilities of Mr Chan (each property) for the year of assessment 2014/15. (Ignore provisional property tax) (34 marks) The following information is related to the properties owned by Mr Chan: Property W – Tai Koo Shing, Hong Kong Mr Chan let Property W to Ms Novack on 1 October 2013 for a term of 4 years. The relevant terms of the lease agreement are as follows: Monthly rent: Initial premium: Deposits: Housekeeping fees: HK$20,000 to be paid at the beginning of each month HKS90,000 HK$20,000 The landlord will provide cleaning services to the tenant at a monthly fee of HK$1,500 Rates and government Payable by the landlord (HK$1,500 per quarter for rates and HKS650 per quarter for government rent) to Payable by the tenant (HK$1,000 per month) rent: Management fees property Co.: management Repair and maintenance: Payable by the landlord During the year ended 31 March 2015, Mr Chan has paid repair expense of HKS8,000 directly to the service provider for fixing the windows. Due to an emergency incident, Ms Novack has first paid repair expense of HK$9,000 to replace the drainage system, and has subsequently received reimbursement of HK$3,000 from Mr Chan. On 18 October 2014, Mr Chan has unexpectedly received rental income of HK$50,000 from Mr Donut, who was an ex-tenant of Property W and disappeared during the year of assessment 2010/11. The rental income of HK$50,000 was previously agreed by the assessor as irrecoverable and has claimed deduction during the year of assessment 2011/12. Property X – CyberPort, Hong Kong It was occupied by Mr Chan as his residence. During the year ended 31 March 2015, Mr Chan paid the following expenses: (i) Rates: HK$3,000 per quarter; (ii) Management fee: HKS3,800 per month; and (iii) Mortgage loan interest: HKS120,000. Property Y – Austin Villa, Panyu district, the PRC Property Y was let to Ms Zhao on 1 July 2014 with a period of 3 years for RMB8,500 per month. Ms Zhao was responsible for paying the management fee of RMB250 per month. Property Y is jointly owned by Mr and Mrs Chan. Property Z – The Hermitage, Kowloon Mr Chan let this property to Mr Bagel on 1 January 2012 for a term of 4 years at a monthly rent of HK$20,000. Rates of HK$1,800 per quarter were paid by Mr Chan. Starting from 1 November 2013, Mr Bagel did not pay any rent, and he moved out from the property on 31 August 2014 and was then untraceable. The property was subsequently let to Ms Camel on the following terms: (i) Lease period: 1 January 2015 to 30 June 2017; (ii) Lump sum premium: HK$45,000; (iii) Monthly rent: HK$15,000; (iv) Management fee: HKS700 per month payable by the landlord; and (v) Rates: HK$1,800 per quarter payable by the tenant. It was agreed by the assessor that the rent owed by Mr Bagel was irrecoverable after he had moved out from the property on 31 August 2014. Required: Compute the property tax liabilities of Mr Chan (each property) for the year of assessment 2014/15. (Ignore provisional property tax) (34 marks)

Expert Answer:

Answer rating: 100% (QA)

Tax Liability Monthly rent 2000012 2400005 12000 Initial Premium 9000028 25200 d... View the full answer

Related Book For

Cost Accounting Foundations and Evolutions

ISBN: 978-1111626822

8th Edition

Authors: Michael R. Kinney, Cecily A. Raiborn

Posted Date:

Students also viewed these accounting questions

-

The following information is related to the Lilliput Veterinary Clinic for April 2010, the firms first month of operation: Veterinarian salaries for April ............... $16,200 Assistants salaries...

-

The following information is related to North Zulch Veterinary Clinic for April 2013, the firms first month of operation: Veterinarian salaries for April ............... $ 8,100 Assistants salaries...

-

The following information is related to the defined benefit pension plan of Simpson Company for the year: Service cost.......................................................$90,000 Contribution to...

-

A taxpayer had the following income: a.) Gain on sale of domestic stocks - P200,000............ b.) Gain on sale of foreign bonds - P100,000............ c.) Gain on sale of a commercial lot in...

-

What are the modules in the baseline accounting system model? Discuss the purposes and transactions associated with each module.

-

Classify each of the following materials as falling into one of the categories listed in Table 12.2. What particles make up these solids and what are the forces of attraction between particles? Give...

-

True or False: Welding on a fan blade requires the welding grounding clamp to be placed on the fan impeller itself.

-

Remnant Carpet Company sells and installs commercial carpeting for office buildings. Remnant Carpet Company uses a job order cost system. When a prospective customer asks for a price quote on a job,...

-

A community's social capital plays an important role in how effective local governments and community-based organizations work together toward common goals. In short, What are ways in which a local...

-

Trim the branches in the following game tree to solve the game depicted: High 10,5) Low (6,3) High (4,15) Top Andre Basie Up Bottom Andre Low (5,7) Andre High (13,3) Down TopAndre Low (22,5) High...

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

Bushmills Irish Whiskey, a world-renowned brand of Diageo plc, is distilled in County Antrim in Northern Ireland. The Old Bushmills distillery has been in operation since 1608 and currently markets...

-

Government crime-fighting targets are a shambles and should be scrapped, claims Chief Superintendent, Ian Johnston. Mr Johnston was speaking ahead of the Police Superintendents Associations annual...

-

Asda is staging a major push south opening 11 new stores in the greater London region over the next few months with plans for a further 150 by 2018.Two of the new stores will be a trial of a new...

-

The British government has pledged to spend 0.7 per cent of national aid resulting in 12 billion being allocated to the Department for International Developments (DfIDs) aid budget despite the fact...

-

The term TetraPak is one which is familiar to most consumers it is the name you will see on the card cartons in which milk, juice and other liquid products are frequently packaged. The Tetra group...

-

Given an array of integers that is of length n, and a positive integer x where x < n. Your job is to rotate the numbers in the array x index to the right. {1, 2, 3, 4, 5}, 3 public static void m

-

1. Advertising for eyeglasses _________ (increases/decreases) the price of eyeglasses because advertising promotes _________. 2. An advertisement that succeeds in getting consumers to try the product...

-

Svenson Technology considers direct labor cost too insignificant to separately account for, and, therefore, uses a $22.50 per machine hour predetermined conversion cost rate (of which $16 is related...

-

You are a partner in a local accounting firm that does financial planning and prepares tax returns, payroll, and financial reports for medium-size companies. Your monthly financial statements show...

-

The accounting system for Amaldi Co. reflected the following quality costs for 2009 and 2010: a. Which of these are costs of compliance, and which are costs of noncompliance? b. Calculate the...

-

A4-stroke, 4-cylinder, single acting spark ignition petrol engine develops \(20 \mathrm{~kW}\) brake power at \(3000 \mathrm{rpm}\). The following data are given : Bore \(=65 \mathrm{~mm}\), Stroke...

-

A six cylinder four stroke I.C. Engine is to develop \(100 \mathrm{~kW}\) i.p. at 800 RPM. The stroke to bare ratio is 1.25. Assuming Mechanical efficiency of \(80 \%\) and break mean effective...

-

The following data is available for a four stroke petrol engine stroke volume \(=6\) Litres. Mean effective pressure \(=6\) bar. Speed of engine \(=750\) RPM. Calculate i.p. of the engine.

Study smarter with the SolutionInn App