The following Trial Balance was extracted from the books of Hillside Plc at 31st March 2006:...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

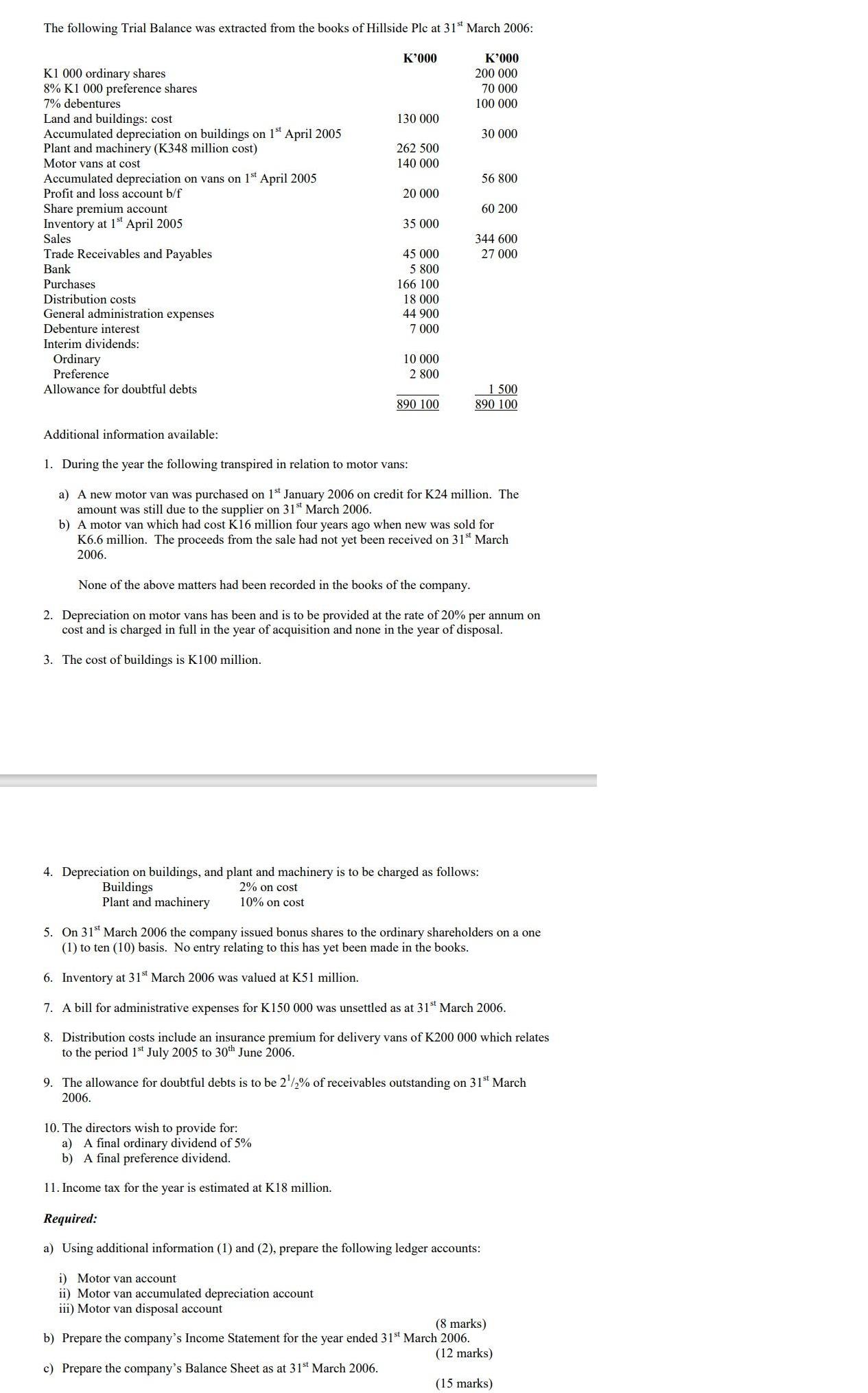

The following Trial Balance was extracted from the books of Hillside Plc at 31st March 2006: K1 000 ordinary shares 8% K1 000 preference shares 7% debentures Land and buildings: cost Accumulated depreciation on buildings on 1st April 2005 Plant and machinery (K348 million cost) Motor vans at cost Accumulated depreciation on vans on 1st April 2005 Profit and loss account b/f Share premium account Inventory at 1st April 2005 Sales Trade Receivables and Payables Bank Purchases Distribution costs General administration expenses Debenture interest Interim dividends: Ordinary Preference Allowance for doubtful debts Additional information available: K'000 130 000 Buildings Plant and machinery 262 500 140 000 20 000 35 000 10. The directors wish to provide for: a) A final ordinary dividend of 5% b) A final preference dividend. 11. Income tax for the year is estimated at K18 million. 45 000 5 800 166 100 18 000 44 900 7 000 10 000 2 800 890 100 K'000 200 000 70 000 100 000 30 000 56 800 4. Depreciation on buildings, and plant and machinery is to be charged as follows: 2% on cost 10% on cost 60 200 344 600 27 000 1. During the year the following transpired in relation to motor vans: a) A new motor van was purchased on 1st January 2006 on credit for K24 million. The amount was still due to the supplier on 31st March 2006. 1 500 890 100 b) A motor van which had cost K16 million four years ago when new was sold for K6.6 million. The proceeds from the sale had not yet been received on 31st March 2006. None of the above matters had been recorded in the books of the company. 2. Depreciation on motor vans has been and is to be provided at the rate of 20% per annum on cost and is charged in full in the year of acquisition and none in the year of disposal. 3. The cost of buildings is K100 million. 5. On 31st March 2006 the company issued bonus shares to the ordinary shareholders on a one (1) to ten (10) basis. No entry relating to this has yet been made in the books. 6. Inventory at 31st March 2006 was valued at K51 million. 7. A bill for administrative expenses for K150 000 was unsettled as at 31st March 2006. 8. Distribution costs include an insurance premium for delivery vans of K200 000 which relates to the period 1st July 2005 to 30th June 2006. 9. The allowance for doubtful debts is to be 2¹2% of receivables outstanding on 31st March 2006. Required: a) Using additional information (1) and (2), prepare the following ledger accounts: i) Motor van account ii) Motor van accumulated depreciation account iii) Motor van disposal account (8 marks) b) Prepare the company's Income Statement for the year ended 31st March 2006. c) Prepare the company's Balance Sheet as at 31st March 2006. (12 marks) (15 marks) The following Trial Balance was extracted from the books of Hillside Plc at 31st March 2006: K1 000 ordinary shares 8% K1 000 preference shares 7% debentures Land and buildings: cost Accumulated depreciation on buildings on 1st April 2005 Plant and machinery (K348 million cost) Motor vans at cost Accumulated depreciation on vans on 1st April 2005 Profit and loss account b/f Share premium account Inventory at 1st April 2005 Sales Trade Receivables and Payables Bank Purchases Distribution costs General administration expenses Debenture interest Interim dividends: Ordinary Preference Allowance for doubtful debts Additional information available: K'000 130 000 Buildings Plant and machinery 262 500 140 000 20 000 35 000 10. The directors wish to provide for: a) A final ordinary dividend of 5% b) A final preference dividend. 11. Income tax for the year is estimated at K18 million. 45 000 5 800 166 100 18 000 44 900 7 000 10 000 2 800 890 100 K'000 200 000 70 000 100 000 30 000 56 800 4. Depreciation on buildings, and plant and machinery is to be charged as follows: 2% on cost 10% on cost 60 200 344 600 27 000 1. During the year the following transpired in relation to motor vans: a) A new motor van was purchased on 1st January 2006 on credit for K24 million. The amount was still due to the supplier on 31st March 2006. 1 500 890 100 b) A motor van which had cost K16 million four years ago when new was sold for K6.6 million. The proceeds from the sale had not yet been received on 31st March 2006. None of the above matters had been recorded in the books of the company. 2. Depreciation on motor vans has been and is to be provided at the rate of 20% per annum on cost and is charged in full in the year of acquisition and none in the year of disposal. 3. The cost of buildings is K100 million. 5. On 31st March 2006 the company issued bonus shares to the ordinary shareholders on a one (1) to ten (10) basis. No entry relating to this has yet been made in the books. 6. Inventory at 31st March 2006 was valued at K51 million. 7. A bill for administrative expenses for K150 000 was unsettled as at 31st March 2006. 8. Distribution costs include an insurance premium for delivery vans of K200 000 which relates to the period 1st July 2005 to 30th June 2006. 9. The allowance for doubtful debts is to be 2¹2% of receivables outstanding on 31st March 2006. Required: a) Using additional information (1) and (2), prepare the following ledger accounts: i) Motor van account ii) Motor van accumulated depreciation account iii) Motor van disposal account (8 marks) b) Prepare the company's Income Statement for the year ended 31st March 2006. c) Prepare the company's Balance Sheet as at 31st March 2006. (12 marks) (15 marks) The following Trial Balance was extracted from the books of Hillside Plc at 31st March 2006: K1 000 ordinary shares 8% K1 000 preference shares 7% debentures Land and buildings: cost Accumulated depreciation on buildings on 1st April 2005 Plant and machinery (K348 million cost) Motor vans at cost Accumulated depreciation on vans on 1st April 2005 Profit and loss account b/f Share premium account Inventory at 1st April 2005 Sales Trade Receivables and Payables Bank Purchases Distribution costs General administration expenses Debenture interest Interim dividends: Ordinary Preference Allowance for doubtful debts Additional information available: K'000 130 000 Buildings Plant and machinery 262 500 140 000 20 000 35 000 10. The directors wish to provide for: a) A final ordinary dividend of 5% b) A final preference dividend. 11. Income tax for the year is estimated at K18 million. 45 000 5 800 166 100 18 000 44 900 7 000 10 000 2 800 890 100 K'000 200 000 70 000 100 000 30 000 56 800 4. Depreciation on buildings, and plant and machinery is to be charged as follows: 2% on cost 10% on cost 60 200 344 600 27 000 1. During the year the following transpired in relation to motor vans: a) A new motor van was purchased on 1st January 2006 on credit for K24 million. The amount was still due to the supplier on 31st March 2006. 1 500 890 100 b) A motor van which had cost K16 million four years ago when new was sold for K6.6 million. The proceeds from the sale had not yet been received on 31st March 2006. None of the above matters had been recorded in the books of the company. 2. Depreciation on motor vans has been and is to be provided at the rate of 20% per annum on cost and is charged in full in the year of acquisition and none in the year of disposal. 3. The cost of buildings is K100 million. 5. On 31st March 2006 the company issued bonus shares to the ordinary shareholders on a one (1) to ten (10) basis. No entry relating to this has yet been made in the books. 6. Inventory at 31st March 2006 was valued at K51 million. 7. A bill for administrative expenses for K150 000 was unsettled as at 31st March 2006. 8. Distribution costs include an insurance premium for delivery vans of K200 000 which relates to the period 1st July 2005 to 30th June 2006. 9. The allowance for doubtful debts is to be 2¹2% of receivables outstanding on 31st March 2006. Required: a) Using additional information (1) and (2), prepare the following ledger accounts: i) Motor van account ii) Motor van accumulated depreciation account iii) Motor van disposal account (8 marks) b) Prepare the company's Income Statement for the year ended 31st March 2006. c) Prepare the company's Balance Sheet as at 31st March 2006. (12 marks) (15 marks) The following Trial Balance was extracted from the books of Hillside Plc at 31st March 2006: K1 000 ordinary shares 8% K1 000 preference shares 7% debentures Land and buildings: cost Accumulated depreciation on buildings on 1st April 2005 Plant and machinery (K348 million cost) Motor vans at cost Accumulated depreciation on vans on 1st April 2005 Profit and loss account b/f Share premium account Inventory at 1st April 2005 Sales Trade Receivables and Payables Bank Purchases Distribution costs General administration expenses Debenture interest Interim dividends: Ordinary Preference Allowance for doubtful debts Additional information available: K'000 130 000 Buildings Plant and machinery 262 500 140 000 20 000 35 000 10. The directors wish to provide for: a) A final ordinary dividend of 5% b) A final preference dividend. 11. Income tax for the year is estimated at K18 million. 45 000 5 800 166 100 18 000 44 900 7 000 10 000 2 800 890 100 K'000 200 000 70 000 100 000 30 000 56 800 4. Depreciation on buildings, and plant and machinery is to be charged as follows: 2% on cost 10% on cost 60 200 344 600 27 000 1. During the year the following transpired in relation to motor vans: a) A new motor van was purchased on 1st January 2006 on credit for K24 million. The amount was still due to the supplier on 31st March 2006. 1 500 890 100 b) A motor van which had cost K16 million four years ago when new was sold for K6.6 million. The proceeds from the sale had not yet been received on 31st March 2006. None of the above matters had been recorded in the books of the company. 2. Depreciation on motor vans has been and is to be provided at the rate of 20% per annum on cost and is charged in full in the year of acquisition and none in the year of disposal. 3. The cost of buildings is K100 million. 5. On 31st March 2006 the company issued bonus shares to the ordinary shareholders on a one (1) to ten (10) basis. No entry relating to this has yet been made in the books. 6. Inventory at 31st March 2006 was valued at K51 million. 7. A bill for administrative expenses for K150 000 was unsettled as at 31st March 2006. 8. Distribution costs include an insurance premium for delivery vans of K200 000 which relates to the period 1st July 2005 to 30th June 2006. 9. The allowance for doubtful debts is to be 2¹2% of receivables outstanding on 31st March 2006. Required: a) Using additional information (1) and (2), prepare the following ledger accounts: i) Motor van account ii) Motor van accumulated depreciation account iii) Motor van disposal account (8 marks) b) Prepare the company's Income Statement for the year ended 31st March 2006. c) Prepare the company's Balance Sheet as at 31st March 2006. (12 marks) (15 marks)

Expert Answer:

Answer rating: 100% (QA)

a Motor Van Account Purchase of New Motor Van Debit Motor Van New Purchase K24000 Credit Bank Due to Supplier K24000 Sale Proceeds of Motor Van Debit Bank Due from Buyer K6600 Credit Motor Van Sale Pr... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

Refer to the pig farmer survey of Problem 11.7 (Table 11.1 1). Analyze these data using marginal models with all the variables. Data from Problem 11.7: Table 11.11 is from a Kansas State University...

-

The following trial balance was extracted from the books of Marric Ltd. as at 31.05.03 The following information has not been accounted for: 1. Closing inventory as at 31.05.03 is £497,000 2....

-

The following trial balance was extracted from the books of Jaya Enterprise at 31 December 2020. RM RM Bank 135,000 Drawings 10,000 Inventory as at 1 January 2020 800,000 Sales 2,100,000 Purchases...

-

How are Bit coins different from VCU1, VCU2, and VCU3 currencies? How are they similar? What is the primary economic threat of Bit coins?

-

Elizabeth Belt is not completely certain that the loss per lamp is $10 if sales are below the breakeven point (refer to Problem). The loss per lamp could be as low as $8 or as high as $15. What...

-

Mendel conducted some his famous experiments with peas that were either smooth yellow plants or wrinkly green plants. If four peas are randomly selected from a batch consisting of four smooth yellow...

-

The following are six journal entries Keene Engineering, Inc., made during the month of April. Requirement 1. For each transaction shown, determine the accounts affected, the type of account, whether...

-

Photo Tonight, a film-developing and camera-repair franchise, began business on January 1, 20X1. In the process of beginning operations, it incurred the following capital expenditures: Developing...

-

Greenmount Ltd, an ASX listed consumer goods corporation aims to acquire a fashion business to generate new growth opportunities. Following a formal search process, external advisors have identified...

-

The table shown below presents data regarding womens singles Grand Slam tournaments tennis champions. Since 1968 (the start of the Open era), 45 different women have won one or more major tennis...

-

What is the current International Funds Transfer threshold amount that should be reported on?

-

Compare and contrast five types of terrorism.

-

Identify the three main reasons for excuse defenses.

-

Should prostitution be illegal? Why or why not?

-

Explain the difference between a justification defense and an excuse defense.

-

Compare and contrast at least three offenses against public order.

-

ONE require an adjustment (Adjusting Entry AJE) a) Prepaid Insurance b) Salary Expense - c) Interest Payable - d) Service Fees Earned - e) Unearned Revenue - f) Depreciation Expense - 4. Emery...

-

Information graphics, also called infographics, are wildly popular, especially in online environments. Why do you think infographics continue to receive so much attention? How could infographics be...

-

Ephraim Electronics has the following information in respect of the accounting year ended 31 March 20X4. Administration...

-

Trade payables balances at 1st June, per control account and per list of individual purchase ledger balances 306,895 Purchases for the month, per list of purchase invoices 1,206,790 Payments to...

-

It has been suggested that a statement of financial position based on historical cost valuations can be so out of date, and so undervalued in times of significantly rising prices, that it becomes of...

-

The regression shown in column (2) was estimated again, this time using data from 1992 (4000 observations selected at random from the March 1993 Current Population Survey, converted into 2015 dollars...

-

Evaluate the following statement: "In all of the regressions, the coefficient on Female is negative, large, and statistically significant. This provides strong statistical evidence of sex...

-

Referring to Table 7.1 in the text: a. Calculate the \(R^{2}\) for each of the regressions. b. Calculate the homoskedasticity-only \(F\)-statistic for testing \(\beta_{3}=\beta_{4}=0\) in the...

Study smarter with the SolutionInn App