The Fosters definitely want to plan for retirement. They would love to retire at 63, with 80%

Fantastic news! We've Found the answer you've been seeking!

Question:

The Fosters definitely want to plan for retirement. They would love to retire at 63, with 80% replacement of preretirement income. But they understand that they may have to wait longer if that is not a possibility.

Assumptions:

In your conversations with the Fosters and from your research you have discovered:

- Inflation (CPI) is expected to be 3%

- The rate of return on their investments and any additional retirement savings is expected to be 8%

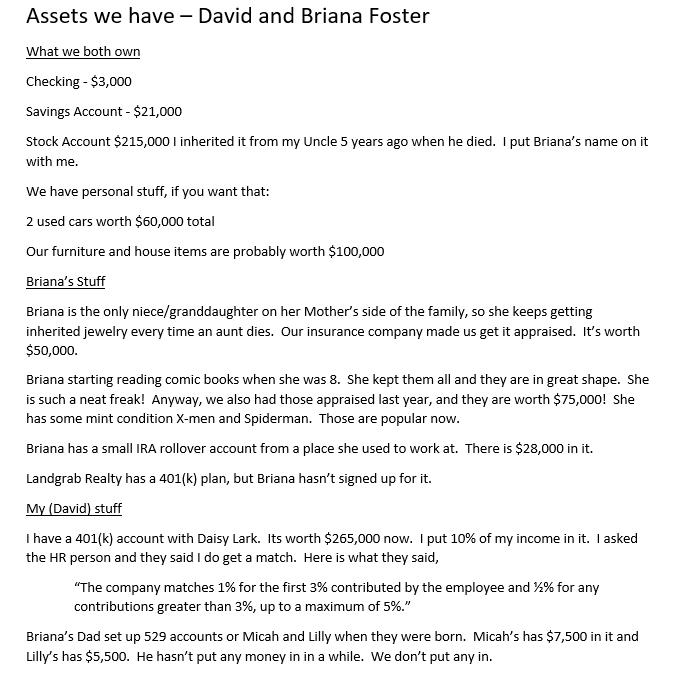

- Both have similar 401(k) plans at their respective employers. Both plans have an employer match of 100% for the first 3% of salary David contributes, and 50% for any contributions greater than 3% up to 5%. Briana would like to start contributing but hasn't gotten around to it. David contributes 10%.

- Based on their family history, they both expect to live to age 95

- Their combined Social Security Benefits are expected to be (in today's dollars):

- Age 63 - $36,450

- Age 65 - $42,120

- Age 67 - $48,600

- You should be able to perform all calculations using the methods found in your textbook.

- Calculate the amount they would have to invest today in a lump sum to fully fund retirement at Age 63. Show the steps performed to get your answer. In your paper, discuss with them whether they have assets to complete this.

- Calculate the annual savings amount required for the Fosters to retire at Ages 63, 65 and 67. Show the steps performed to get your answers.

- Provide a written explanation of the results, including your assumptions, explained as if you were explaining it to the client. Charts/Tables may help the Fosters understand better.

- Discuss in your paper a couple of options of what types of accounts they might use and how much they could save in each.

Expert Answer:

Here is my analysis for the Fosters retirement planning based on the information provided 1 Calculat... View the full answer

Related Book For

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

Posted Date: