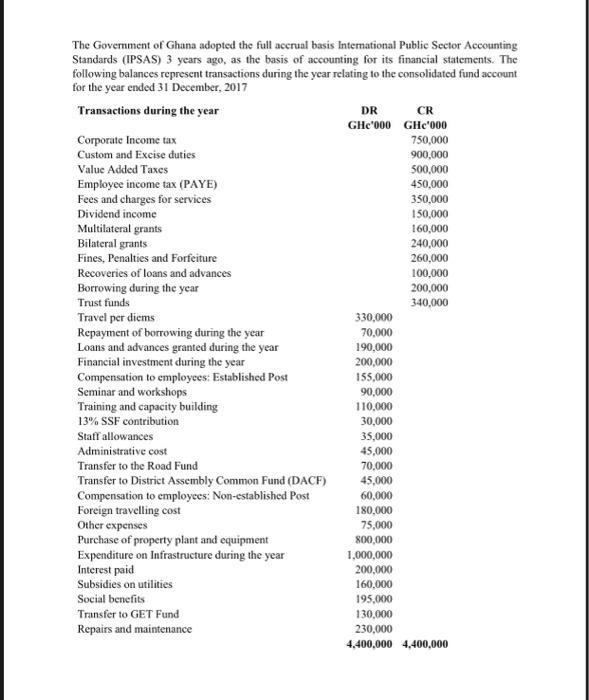

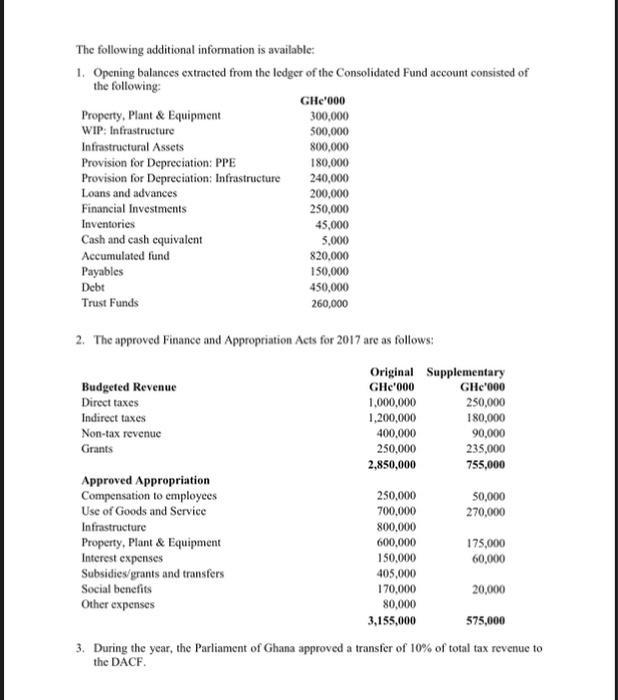

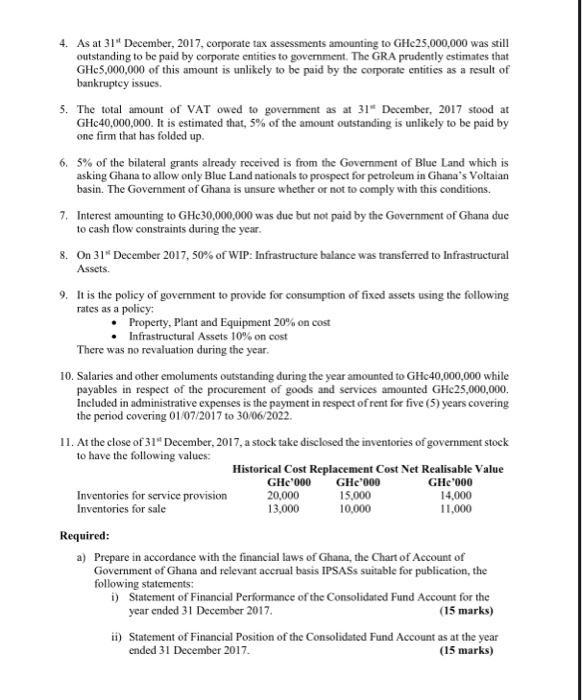

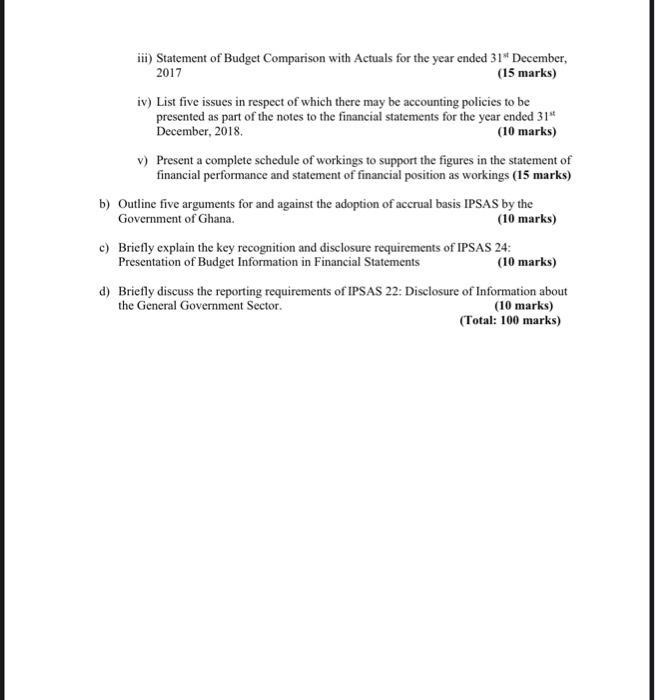

The Government of Ghana adopted the full accrual basis International Public Sector Accounting Standards (IPSAS) 3...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

The Government of Ghana adopted the full accrual basis International Public Sector Accounting Standards (IPSAS) 3 years ago, as the basis of accounting for its financial statements. The following balances represent transactions during the year relating to the consolidated fund account for the year ended 31 December, 2017 Transactions during the year Corporate Income tax Custom and Excise duties Value Added Taxes Employee income tax (PAYE) Fees and charges for services Dividend income Multilateral grants Bilateral grants Fines, Penalties and Forfeiture Recoveries of loans and advances Borrowing during the year Trust funds Travel per diems Repayment of borrowing during the year Loans and advances granted during the year Financial investment during the year Compensation to employees: Established Post Seminar and workshops Training and capacity building 13% SSF contribution Staff allowances Administrative cost Transfer to the Road Fund Transfer to District Assembly Common Fund (DACF) Compensation to employees: Non-established Post Foreign travelling cost Other expenses Purchase of property plant and equipment Expenditure on Infrastructure during the year Interest paid Subsidies on utilities Social benefits Transfer to GET Fund Repairs and maintenance DR GHe'000 330,000 70,000 190,000 200,000 155,000 90,000 110,000 30,000 35,000 45,000 70,000 45,000 60,000 180,000 75,000 800,000 1,000,000 200,000 160,000 195,000 CR GHe'000 750,000 900,000 500,000 450,000 350,000 150,000 160,000 240,000 260,000 100,000 200,000 340,000 130,000 230,000 4,400,000 4,400,000 The following additional information is available: 1. Opening balances extracted from the ledger of the Consolidated Fund account consisted of the following: Property, Plant & Equipment WIP: Infrastructure Infrastructural Assets Provision for Depreciation: PPE Provision for Depreciation: Infrastructure Loans and advances Financial Investments Inventories Cash and cash equivalent Accumulated fund Payables Debt Trust Funds Budgeted Revenue Direct taxes Indirect taxes 2. The approved Finance and Appropriation Acts for 2017 are as follows: Non-tax revenue Grants Approved Appropriation Compensation to employees Use of Goods and Service Infrastructure Property, Plant & Equipment Interest expenses GHe'000 300,000 500,000 800,000 180,000 240,000 200,000 250,000 Subsidies/grants and transfers Social benefits Other expenses 45,000 5,000 820,000 150,000 450,000 260,000 Original Supplementary GHe'000 1,000,000 1,200,000 400,000 250,000 2,850,000 250,000 700,000 800,000 600,000 150,000 405,000 170,000 80,000 3,155,000 GHC000 250,000 180,000 90,000 235,000 755,000 50,000 270,000 175,000 60,000 20,000 575,000 3. During the year, the Parliament of Ghana approved a transfer of 10% of total tax revenue to the DACF. 4. As at 31" December, 2017, corporate tax assessments amounting to GHc25,000,000 was still outstanding to be paid by corporate entities to government. The GRA prudently estimates that GHc5,000,000 of this amount is unlikely to be paid by the corporate entities as a result of bankruptcy issues. 5. The total amount of VAT owed to government as at 31 December, 2017 stood at GHc40,000,000. It is estimated that, 5% of the amount outstanding is unlikely to be paid by one firm that has folded up. 6. 5% of the bilateral grants already received is from the Government of Blue Land which is asking Ghana to allow only Blue Land nationals to prospect for petroleum in Ghana's Voltaian basin. The Government of Ghana is unsure whether or not to comply with this conditions. 7. Interest amounting to GHc30,000,000 was due but not paid by the Government of Ghana due to cash flow constraints during the year. 8. On 31* December 2017, 50% of WIP: Infrastructure balance was transferred to Infrastructural Assets. 9. It is the policy of government to provide for consumption of fixed assets using the following rates as a policy: Property, Plant and Equipment 20% on cost Infrastructural Assets 10% on cost There was no revaluation during the year. 10. Salaries and other emoluments outstanding during the year amounted to GHc40,000,000 while payables in respect of the procurement of goods and services amounted GHc25,000,000. Included in administrative expenses is the payment in respect of rent for five (5) years covering the period covering 01/07/2017 to 30/06/2022. 11. At the close of 31 December, 2017, a stock take disclosed the inventories of government stock to have the following values: Inventories for service provision Inventories for sale Historical Cost Replacement Cost Net Realisable Value GHe'000 GHe'000 20,000 13,000 GHe'000 15,000 10,000 14,000 11,000 Required: a) Prepare in accordance with the financial laws of Ghana, the Chart of Account of Government of Ghana and relevant accrual basis IPSASS suitable for publication, the following statements: i) Statement of Financial Performance of the Consolidated Fund Account for the year ended 31 December 2017. (15 marks) ii) Statement of Financial Position of the Consolidated Fund Account as at the year ended 31 December 2017. (15 marks) iii) Statement of Budget Comparison with Actuals for the year ended 31* December, 2017 (15 marks) iv) List five issues in respect of which there may be accounting policies to be presented as part of the notes to the financial statements for the year ended 31st December, 2018. (10 marks) v) Present a complete schedule of workings to support the figures in the statement of financial performance and statement of financial position as workings (15 marks) b) Outline five arguments for and against the adoption of accrual basis IPSAS by the Government of Ghana. (10 marks) c) Briefly explain the key recognition and disclosure requirements of IPSAS 24: Presentation of Budget Information in Financial Statements (10 marks) d) Briefly discuss the reporting requirements of IPSAS 22: Disclosure of Information about the General Government Sector. (10 marks) (Total: 100 marks) The Government of Ghana adopted the full accrual basis International Public Sector Accounting Standards (IPSAS) 3 years ago, as the basis of accounting for its financial statements. The following balances represent transactions during the year relating to the consolidated fund account for the year ended 31 December, 2017 Transactions during the year Corporate Income tax Custom and Excise duties Value Added Taxes Employee income tax (PAYE) Fees and charges for services Dividend income Multilateral grants Bilateral grants Fines, Penalties and Forfeiture Recoveries of loans and advances Borrowing during the year Trust funds Travel per diems Repayment of borrowing during the year Loans and advances granted during the year Financial investment during the year Compensation to employees: Established Post Seminar and workshops Training and capacity building 13% SSF contribution Staff allowances Administrative cost Transfer to the Road Fund Transfer to District Assembly Common Fund (DACF) Compensation to employees: Non-established Post Foreign travelling cost Other expenses Purchase of property plant and equipment Expenditure on Infrastructure during the year Interest paid Subsidies on utilities Social benefits Transfer to GET Fund Repairs and maintenance DR GHe'000 330,000 70,000 190,000 200,000 155,000 90,000 110,000 30,000 35,000 45,000 70,000 45,000 60,000 180,000 75,000 800,000 1,000,000 200,000 160,000 195,000 CR GHe'000 750,000 900,000 500,000 450,000 350,000 150,000 160,000 240,000 260,000 100,000 200,000 340,000 130,000 230,000 4,400,000 4,400,000 The following additional information is available: 1. Opening balances extracted from the ledger of the Consolidated Fund account consisted of the following: Property, Plant & Equipment WIP: Infrastructure Infrastructural Assets Provision for Depreciation: PPE Provision for Depreciation: Infrastructure Loans and advances Financial Investments Inventories Cash and cash equivalent Accumulated fund Payables Debt Trust Funds Budgeted Revenue Direct taxes Indirect taxes 2. The approved Finance and Appropriation Acts for 2017 are as follows: Non-tax revenue Grants Approved Appropriation Compensation to employees Use of Goods and Service Infrastructure Property, Plant & Equipment Interest expenses GHe'000 300,000 500,000 800,000 180,000 240,000 200,000 250,000 Subsidies/grants and transfers Social benefits Other expenses 45,000 5,000 820,000 150,000 450,000 260,000 Original Supplementary GHe'000 1,000,000 1,200,000 400,000 250,000 2,850,000 250,000 700,000 800,000 600,000 150,000 405,000 170,000 80,000 3,155,000 GHC000 250,000 180,000 90,000 235,000 755,000 50,000 270,000 175,000 60,000 20,000 575,000 3. During the year, the Parliament of Ghana approved a transfer of 10% of total tax revenue to the DACF. 4. As at 31" December, 2017, corporate tax assessments amounting to GHc25,000,000 was still outstanding to be paid by corporate entities to government. The GRA prudently estimates that GHc5,000,000 of this amount is unlikely to be paid by the corporate entities as a result of bankruptcy issues. 5. The total amount of VAT owed to government as at 31 December, 2017 stood at GHc40,000,000. It is estimated that, 5% of the amount outstanding is unlikely to be paid by one firm that has folded up. 6. 5% of the bilateral grants already received is from the Government of Blue Land which is asking Ghana to allow only Blue Land nationals to prospect for petroleum in Ghana's Voltaian basin. The Government of Ghana is unsure whether or not to comply with this conditions. 7. Interest amounting to GHc30,000,000 was due but not paid by the Government of Ghana due to cash flow constraints during the year. 8. On 31* December 2017, 50% of WIP: Infrastructure balance was transferred to Infrastructural Assets. 9. It is the policy of government to provide for consumption of fixed assets using the following rates as a policy: Property, Plant and Equipment 20% on cost Infrastructural Assets 10% on cost There was no revaluation during the year. 10. Salaries and other emoluments outstanding during the year amounted to GHc40,000,000 while payables in respect of the procurement of goods and services amounted GHc25,000,000. Included in administrative expenses is the payment in respect of rent for five (5) years covering the period covering 01/07/2017 to 30/06/2022. 11. At the close of 31 December, 2017, a stock take disclosed the inventories of government stock to have the following values: Inventories for service provision Inventories for sale Historical Cost Replacement Cost Net Realisable Value GHe'000 GHe'000 20,000 13,000 GHe'000 15,000 10,000 14,000 11,000 Required: a) Prepare in accordance with the financial laws of Ghana, the Chart of Account of Government of Ghana and relevant accrual basis IPSASS suitable for publication, the following statements: i) Statement of Financial Performance of the Consolidated Fund Account for the year ended 31 December 2017. (15 marks) ii) Statement of Financial Position of the Consolidated Fund Account as at the year ended 31 December 2017. (15 marks) iii) Statement of Budget Comparison with Actuals for the year ended 31* December, 2017 (15 marks) iv) List five issues in respect of which there may be accounting policies to be presented as part of the notes to the financial statements for the year ended 31st December, 2018. (10 marks) v) Present a complete schedule of workings to support the figures in the statement of financial performance and statement of financial position as workings (15 marks) b) Outline five arguments for and against the adoption of accrual basis IPSAS by the Government of Ghana. (10 marks) c) Briefly explain the key recognition and disclosure requirements of IPSAS 24: Presentation of Budget Information in Financial Statements (10 marks) d) Briefly discuss the reporting requirements of IPSAS 22: Disclosure of Information about the General Government Sector. (10 marks) (Total: 100 marks)

Expert Answer:

Answer rating: 100% (QA)

Ghana Government Consolidated Fund Account Financial Statements for the Year Ended 31 December 2017 Statement of Financial Performance Description Amount GHC000 Revenue Corporate income tax 750000 Cus... View the full answer

Related Book For

Government and Not for Profit Accounting Concepts and Practices

ISBN: 978-1118155974

6th edition

Authors: Michael H. Granof, Saleha B. Khumawala

Posted Date:

Students also viewed these accounting questions

-

Many advocates of the International Public Sector Accounting Standards (IPSAS) have argued that it can enhance public sector accountability and governance quality. Some studies particularly...

-

Explain the three significant expenditure items the government of Ghana uses and suggest how those with unfavourable variance can be controlled.

-

International Public Sector Accounting Standards Board (IPSASB) develops accrual IPASS that are converged with International Financial Reporting Standards (IFRSS) issued by the IASB by adapting them...

-

The portfolio of stock that comprises the ASX200 index is currently worth $5000. The continuously compounded interest rates on Australian government bonds is 1.5% per annum for each of the next five...

-

From the following selected data, compute: 1. Net cash flow provided (used) by operating activities. 2. Net cash flow provided (used) by investing activities. 3. Net cash flow provided (used) by...

-

Logistics Solutions provides order fulfillment services for dot.com merchants. The company maintains warehouses that stock items carried by its dot.com clients. When a client receives an order from a...

-

Match each of the following items with its location in the accounting equation. Use the most detailed category appropriate: a. Assets b. Liabilities c. Stockholders' Equity d. Revenues e. Expenses -...

-

Tiffany Goren started her own consulting firm, Goren Consulting, on May 1, 2010. The trial balance at May 31 is as shown below. In addition to those accounts listed on the trial balance, the chart of...

-

3. The S&P 500 stock index option is currently trading at 1,200. The strike price is 1,200. You believe the stock market is going to decline. You decide to buy 20 stock index put option contracts for...

-

Comparative income statements and balance sheets for Merck ($millions) follow: Required a. Use the following ratios to prepare a projected income statement, balance sheet, and statement of cash flows...

-

An 1100-0 Aluminum strip 8 inches wide is cold rolled in one pass from 0.075 inch to 0.005 inch in thickness with 6 inch diameter rolls rotating at 0.5 rps. The material is characterized by 26000 0.2...

-

Discuss the scope and objectives of internal audits, and how they assist management in identifying operational inefficiencies, detecting fraud, and enhancing overall governance processes. Provide...

-

Write a free verse poem Free verse is non-rhyming andnon-metered, meaning youre free from the rules of a metered formlike a haiku or sonnet. Instead of making your lines fit a rhymescheme or metered...

-

Umar wants to buy Derek's house. The purchase price is $900,000 and there is an outstanding mortgage in favour of Scotiabank in the amount of $400,000. Umar has $600,000 in savings to put towards the...

-

An MRI technician moves her hand from a region of very low magnetic field strength into an MRI scanner's 2.00 T field with her fingers pointing in the direction of the field.

-

What is wrong with the statements being made in relation toNorse mythology? 7) With Selvig\'s help, he is freed and resigns himself to exileon Earth as he develops a romance with Jane. Loki discovers...

-

A company is using Supply Chain Management. You need to configure inbound operations for a warehouse worker using a warehousing mobile device. Which process should you configure?

-

Why is inventory management important for merchandising and manufacturing firms and what are the main tradeoffs for firms in managing their inventory?

-

A city established a public housing authority to fund the construction of low-income residential homes within city limits. The authority is governed by a nine-person board of trustees. New trustees...

-

The following totals were drawn from Independence Citys Schedule of Changes in Capital Assets by Function and Activity, included in the citys ï¬nancial statements for the year ending June...

-

What is an agency fund? Why is it the easiest fund for which to account?

-

Restore the file Wild Water Sports Ch 06A (Backup) you downloaded from the student companion site and then save it as Wild Water Sports Ch 06A. If you are asked to setup an external accountant user,...

-

You must have completed Exercise 1 in this chapter to complete this exercise. Restore the backup file you created in Exercise 1. Change the company name to Boston Catering Ch 6 Ex 2. Add the...

-

You must have completed Exercise 1 in this chapter to complete this exercise. Restore the backup file you created in Exercise 1. Change the company name to Boston Catering Ch 6 Ex 3. Add the...

Study smarter with the SolutionInn App