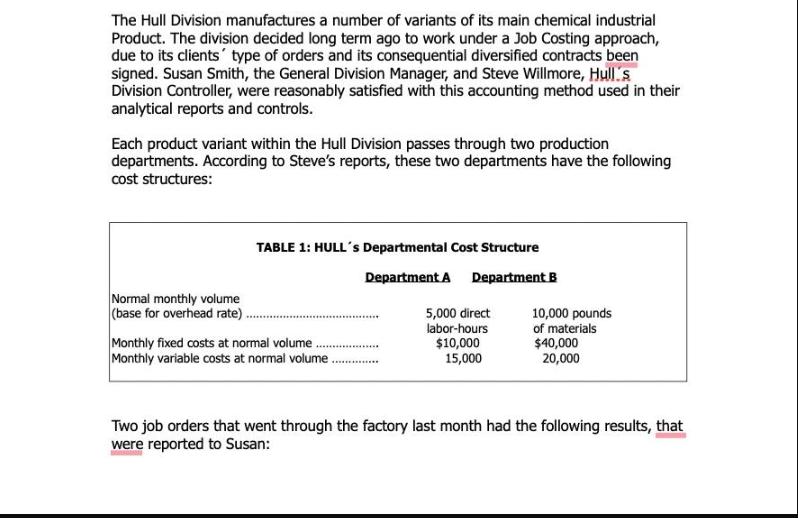

The Hull Division manufactures a number of variants of its main chemical industrial Product. The division...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

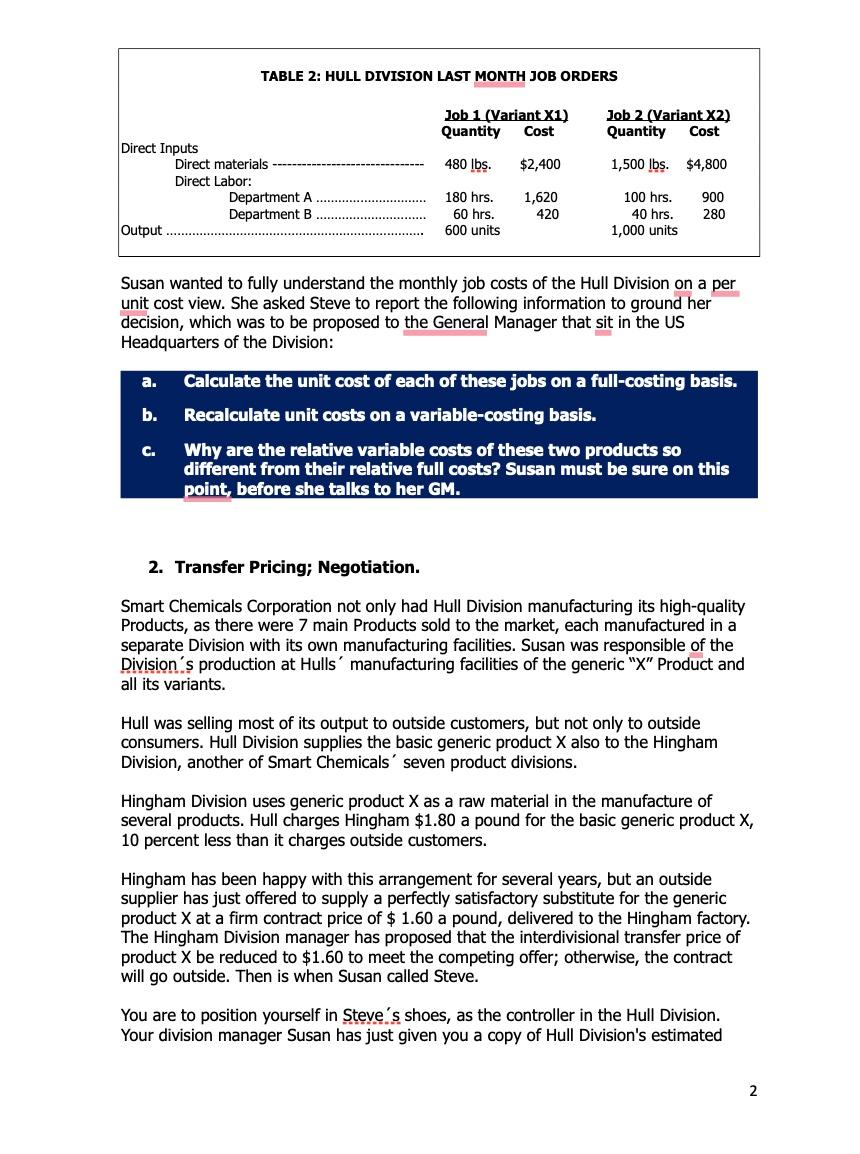

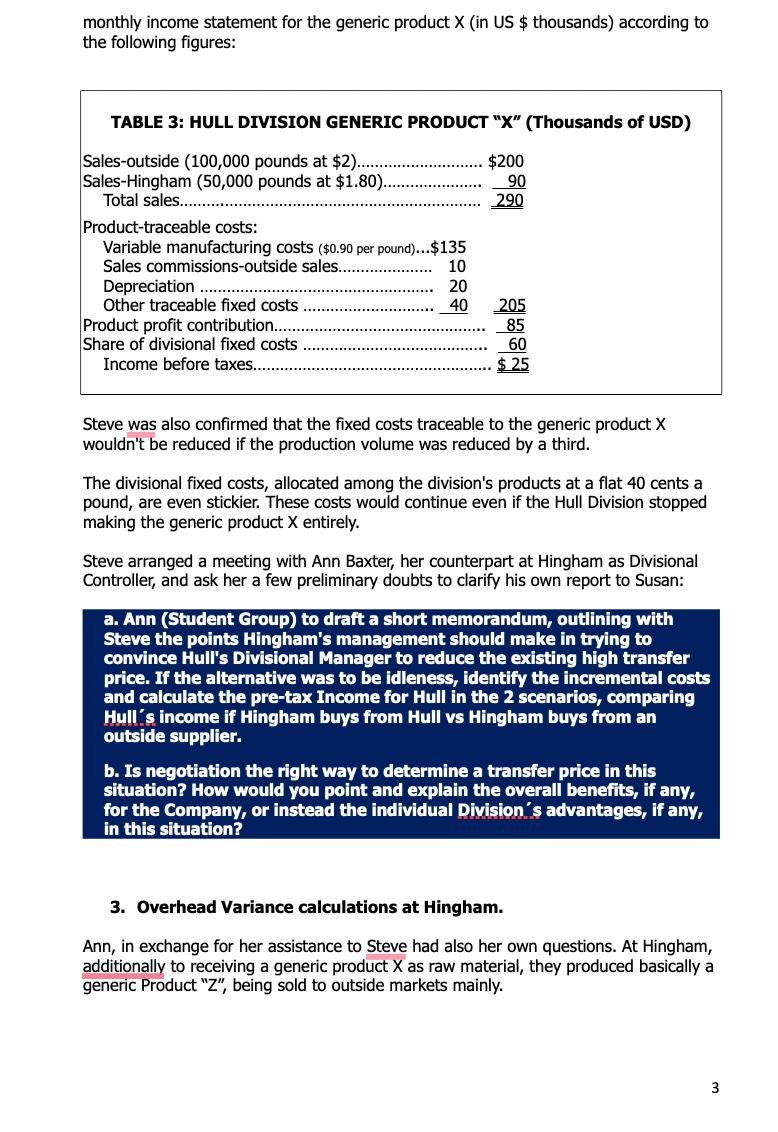

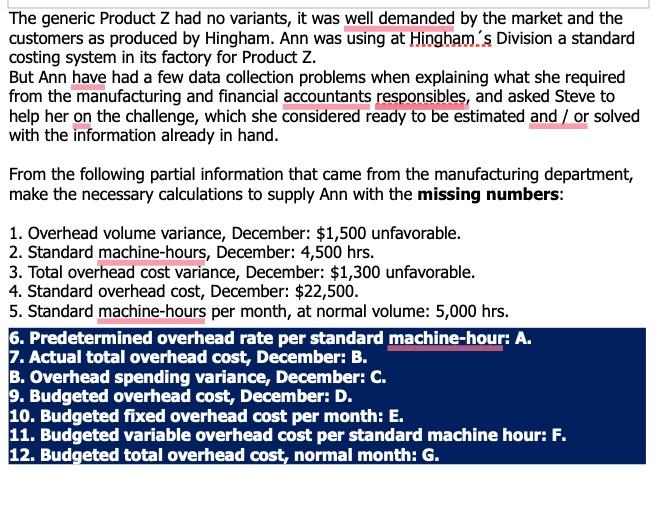

The Hull Division manufactures a number of variants of its main chemical industrial Product. The division decided long term ago to work under a Job Costing approach, due to its clients' type of orders and its consequential diversified contracts been signed. Susan Smith, the General Division Manager, and Steve Willmore, Hull's Division Controller, were reasonably satisfied with this accounting method used in their analytical reports and controls. Each product variant within the Hull Division passes through two production departments. According to Steve's reports, these two departments have the following cost structures: Normal monthly volume (base for overhead rate) TABLE 1: HULL's Departmental Cost Structure Department A Department B Monthly fixed costs at normal volume Monthly variable costs at normal volume. 5,000 direct labor-hours $10,000 15,000 10,000 pounds of materials $40,000 20,000 Two job orders that went through the factory last month had the following results, that were reported to Susan: Direct Inputs Output a. b. TABLE 2: HULL DIVISION LAST MONTH JOB ORDERS C. Direct materials Direct Labor: Department A Department B Job 1 (Variant X1) Quantity Cost $2,400 1,620 420 480 lbs. 180 hrs. 60 hrs. 600 units Job 2 (Variant X2) Quantity Cost 1,500 lbs. $4,800 Susan wanted to fully understand the monthly job costs of the Hull Division on a per unit cost view. She asked Steve to report the following information to ground her decision, which was to be proposed to the General Manager that sit in the US Headquarters of the Division: 100 hrs. 40 hrs. 1,000 units 900 280 Calculate the unit cost of each of these jobs on a full-costing basis. Recalculate unit costs on a variable-costing basis. Why are the relative variable costs of these two products so different from their relative full costs? Susan must be sure on this point, before she talks to her GM. 2. Transfer Pricing; Negotiation. Smart Chemicals Corporation not only had Hull Division manufacturing its high-quality Products, as there were 7 main Products sold to the market, each manufactured in a separate Division with its own manufacturing facilities. Susan was responsible of the Division's production at Hulls manufacturing facilities of the generic "X" Product and all its variants. Hull was selling most of its output to outside customers, but not only to outside consumers. Hull Division supplies the basic generic product X also to the Hingham Division, another of Smart Chemicals' seven product divisions. Hingham Division uses generic product X as a raw material in the manufacture of several products. Hull charges Hingham $1.80 a pound for the basic generic product X, 10 percent less than it charges outside customers. Hingham has been happy with this arrangement for several years, but an outside supplier has just offered to supply a perfectly satisfactory substitute for the generic product X at a firm contract price of $ 1.60 a pound, delivered to the Hingham factory. The Hingham Division manager has proposed that the interdivisional transfer price of product X be reduced to $1.60 to meet the competing offer; otherwise, the contract will go outside. Then is when Susan called Steve. You are to position yourself in Steve's shoes, as the controller in the Hull Division. Your division manager Susan has just given you a copy of Hull Division's estimated 2 monthly income statement for the generic product X (in US $ thousands) according to the following figures: TABLE 3: HULL DIVISION GENERIC PRODUCT "X" (Thousands of USD) Sales-outside (100,000 pounds at $2)... $200 Sales-Hingham (50,000 pounds at $1.80).. 90 Total sales. 290 Product-traceable costs: Variable manufacturing costs ($0.90 per pound)... $135 Sales commissions-outside sales. 10 Depreciation Other traceable fixed costs Product profit contribution.. Share of divisional fixed costs Income before taxes... 20 40 205 85 60 $25 Steve was also confirmed that the fixed costs traceable to the generic product X wouldn't be reduced if the production volume was reduced by a third. The divisional fixed costs, allocated among the division's products at a flat 40 cents a pound, are even stickier. These costs would continue even if the Hull Division stopped making the generic product X entirely. Steve arranged a meeting with Ann Baxter, her counterpart at Hingham as Divisional Controller, and ask her a few preliminary doubts to clarify his own report to Susan: a. Ann (Student Group) to draft a short memorandum, outlining with Steve the points Hingham's management should make in trying to convince Hull's Divisional Manager to reduce the existing high transfer price. If the alternative was to be idleness, identify the incremental costs and calculate the pre-tax Income for Hull in the 2 scenarios, comparing Hull's income if Hingham buys from Hull vs Hingham buys from an outside supplier. b. Is negotiation the right way to determine a transfer price in this situation? How would you point and explain the overall benefits, if any, for the Company, or instead the individual Division's advantages, if any, in this situation? 3. Overhead Variance calculations at Hingham. Ann, in exchange for her assistance to Steve had also her own questions. At Hingham, additionally to receiving a generic product X as raw material, they produced basically a generic Product "Z", being sold to outside markets mainly. 3 The generic Product Z had no variants, it was well demanded by the market and the customers as produced by Hingham. Ann was using at Hingham's Division a standard costing system in its factory for Product Z. But Ann have had a few data collection problems when explaining what she required from the manufacturing and financial accountants responsibles, and asked Steve to help her on the challenge, which she considered ready to be estimated and / or solved with the information already in hand. From the following partial information that came from the manufacturing department, make the necessary calculations to supply Ann with the missing numbers: 1. Overhead volume variance, December: $1,500 unfavorable. 2. Standard machine-hours, December: 4,500 hrs. 3. Total overhead cost variance, December: $1,300 unfavorable. 4. Standard overhead cost, December: $22,500. 5. Standard machine-hours per month, at normal volume: 5,000 hrs. 6. Predetermined overhead rate per standard machine-hour: A. 7. Actual total overhead cost, December: B. B. Overhead spending variance, December: C. 9. Budgeted overhead cost, December: D. 10. Budgeted fixed overhead cost per month: E. 11. Budgeted variable overhead cost per standard machine hour: F. 12. Budgeted total overhead cost, normal month: G. The Hull Division manufactures a number of variants of its main chemical industrial Product. The division decided long term ago to work under a Job Costing approach, due to its clients' type of orders and its consequential diversified contracts been signed. Susan Smith, the General Division Manager, and Steve Willmore, Hull's Division Controller, were reasonably satisfied with this accounting method used in their analytical reports and controls. Each product variant within the Hull Division passes through two production departments. According to Steve's reports, these two departments have the following cost structures: Normal monthly volume (base for overhead rate) TABLE 1: HULL's Departmental Cost Structure Department A Department B Monthly fixed costs at normal volume Monthly variable costs at normal volume. 5,000 direct labor-hours $10,000 15,000 10,000 pounds of materials $40,000 20,000 Two job orders that went through the factory last month had the following results, that were reported to Susan: Direct Inputs Output a. b. TABLE 2: HULL DIVISION LAST MONTH JOB ORDERS C. Direct materials Direct Labor: Department A Department B Job 1 (Variant X1) Quantity Cost $2,400 1,620 420 480 lbs. 180 hrs. 60 hrs. 600 units Job 2 (Variant X2) Quantity Cost 1,500 lbs. $4,800 Susan wanted to fully understand the monthly job costs of the Hull Division on a per unit cost view. She asked Steve to report the following information to ground her decision, which was to be proposed to the General Manager that sit in the US Headquarters of the Division: 100 hrs. 40 hrs. 1,000 units 900 280 Calculate the unit cost of each of these jobs on a full-costing basis. Recalculate unit costs on a variable-costing basis. Why are the relative variable costs of these two products so different from their relative full costs? Susan must be sure on this point, before she talks to her GM. 2. Transfer Pricing; Negotiation. Smart Chemicals Corporation not only had Hull Division manufacturing its high-quality Products, as there were 7 main Products sold to the market, each manufactured in a separate Division with its own manufacturing facilities. Susan was responsible of the Division's production at Hulls manufacturing facilities of the generic "X" Product and all its variants. Hull was selling most of its output to outside customers, but not only to outside consumers. Hull Division supplies the basic generic product X also to the Hingham Division, another of Smart Chemicals' seven product divisions. Hingham Division uses generic product X as a raw material in the manufacture of several products. Hull charges Hingham $1.80 a pound for the basic generic product X, 10 percent less than it charges outside customers. Hingham has been happy with this arrangement for several years, but an outside supplier has just offered to supply a perfectly satisfactory substitute for the generic product X at a firm contract price of $ 1.60 a pound, delivered to the Hingham factory. The Hingham Division manager has proposed that the interdivisional transfer price of product X be reduced to $1.60 to meet the competing offer; otherwise, the contract will go outside. Then is when Susan called Steve. You are to position yourself in Steve's shoes, as the controller in the Hull Division. Your division manager Susan has just given you a copy of Hull Division's estimated 2 monthly income statement for the generic product X (in US $ thousands) according to the following figures: TABLE 3: HULL DIVISION GENERIC PRODUCT "X" (Thousands of USD) Sales-outside (100,000 pounds at $2)... $200 Sales-Hingham (50,000 pounds at $1.80).. 90 Total sales. 290 Product-traceable costs: Variable manufacturing costs ($0.90 per pound)... $135 Sales commissions-outside sales. 10 Depreciation Other traceable fixed costs Product profit contribution.. Share of divisional fixed costs Income before taxes... 20 40 205 85 60 $25 Steve was also confirmed that the fixed costs traceable to the generic product X wouldn't be reduced if the production volume was reduced by a third. The divisional fixed costs, allocated among the division's products at a flat 40 cents a pound, are even stickier. These costs would continue even if the Hull Division stopped making the generic product X entirely. Steve arranged a meeting with Ann Baxter, her counterpart at Hingham as Divisional Controller, and ask her a few preliminary doubts to clarify his own report to Susan: a. Ann (Student Group) to draft a short memorandum, outlining with Steve the points Hingham's management should make in trying to convince Hull's Divisional Manager to reduce the existing high transfer price. If the alternative was to be idleness, identify the incremental costs and calculate the pre-tax Income for Hull in the 2 scenarios, comparing Hull's income if Hingham buys from Hull vs Hingham buys from an outside supplier. b. Is negotiation the right way to determine a transfer price in this situation? How would you point and explain the overall benefits, if any, for the Company, or instead the individual Division's advantages, if any, in this situation? 3. Overhead Variance calculations at Hingham. Ann, in exchange for her assistance to Steve had also her own questions. At Hingham, additionally to receiving a generic product X as raw material, they produced basically a generic Product "Z", being sold to outside markets mainly. 3 The generic Product Z had no variants, it was well demanded by the market and the customers as produced by Hingham. Ann was using at Hingham's Division a standard costing system in its factory for Product Z. But Ann have had a few data collection problems when explaining what she required from the manufacturing and financial accountants responsibles, and asked Steve to help her on the challenge, which she considered ready to be estimated and / or solved with the information already in hand. From the following partial information that came from the manufacturing department, make the necessary calculations to supply Ann with the missing numbers: 1. Overhead volume variance, December: $1,500 unfavorable. 2. Standard machine-hours, December: 4,500 hrs. 3. Total overhead cost variance, December: $1,300 unfavorable. 4. Standard overhead cost, December: $22,500. 5. Standard machine-hours per month, at normal volume: 5,000 hrs. 6. Predetermined overhead rate per standard machine-hour: A. 7. Actual total overhead cost, December: B. B. Overhead spending variance, December: C. 9. Budgeted overhead cost, December: D. 10. Budgeted fixed overhead cost per month: E. 11. Budgeted variable overhead cost per standard machine hour: F. 12. Budgeted total overhead cost, normal month: G.

Expert Answer:

Answer rating: 100% (QA)

Answer Question 1 c Explanation for the Difference in Relative Variable Costs The relative variable costs of the two products are different from their relative full costs due to the allocation of fixe... View the full answer

Related Book For

Managerial accounting

ISBN: 978-0471467854

1st edition

Authors: ramji balakrishnan, k. s i varamakrishnan, Geoffrey b. sprin

Posted Date:

Students also viewed these finance questions

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

Planning is one of the most important management functions in any business. A front office managers first step in planning should involve determine the departments goals. Planning also includes...

-

Read the case study "Southwest Airlines," found in Part 2 of your textbook. Review the "Guide to Case Analysis" found on pp. CA1 - CA11 of your textbook. (This guide follows the last case in the...

-

The statements of financial position of Parkway plc for 20X7 and 20X8 are given below, together with the income statement for the year ended 30 June 20X8. Statement of comprehensive income of Parkway...

-

Suppose a new and more liberal Congress and administration are elected. Their first order of business is to take away the independence of the Federal Reserve System and to force the Fed to greatly...

-

Describe various defenses and remedies available for nonperformance of a contract.

-

Brooke Young runs Young Yachting Pty Ltd. Brooke is a graduate of a tourism and hospitality degree and offers a luxury fully catered yachting holiday experience that includes scuba diving, swimming...

-

The email server at Rockbottom University has been experiencing downtime. Let us assume that the trials of an associated Markov process are defined as one-hour periods and that the probability of the...

-

Demonstrate your understanding of both classical and operant conditioning. Think about your current behaviors such as, studying, driving, playing sports, exercise, or eating patterns. Then, select...

-

Start with the partial model in the file Ch21 P08 Build a Model.xlsx on the textbook's Web site. Kasperov Corporation has an unlevered cost of equity of 12% and is taxed at a 40% rate. The 4-year...

-

anceLab Assignment Question 3, P9-4 (similar to) Part 1 of 2 > a. The value of this bond if it paid interest annually would be $ K (Related to Checkpoint 9.4) (Bond valuation) A bond that matures in...

-

Read the poem by Sherman Alexie entitled, The Powwow at the End of the World (1996). The Powwow at the End of the World and answers the questions. 1. who is speaking 2. what is the speaker speaking...

-

A topic that has a local focus, such as a change that needs to happen in your community. Please include three things: what the need for change is, what your planned solution is, and who the audience...

-

Suggest which solution to a gender-neutral pronoun you think would be the best option and why. What do you think is the best approach to appeal to the Real Academia Espaola to make them official...

-

Please take a look at the Checklist below and talk about your thoughts on what it recommends compared to your usual habits when it comes to drafting and revising your writing. Feel free to address...

-

Important considerations pertaining to the amount of inventory a business has available to sell, allows for discovering what items are hot sells for a business. Knowing this you will know how much...

-

Assume a USD is worth CAD 0.97, (St=0.97 CAD/USD). Also, a GBP is worth USD 2.05 (St=2.05 USD/GBP). What is the cross rate CAD/GBP? Suppose Kwiki Bank quotes St= 2.15 CAD/GBP. Is arbitrage possible?...

-

Show that, given a maximum flow in a network with m edges, a minimum cut of N can be computed in O(m) time.

-

What are some special items that might affect a firms cash budget?

-

Bosworth Boxes makes cardboard boxes. For March and April, Bosworth expects to produce 12,000 and 15,800 boxes, respectively. The main material input for Bosworths boxes is cardboard. To make one...

-

Select Auto Imports is a regional auto dealership that specializes in selling high-end imported luxury automobiles. Select Auto Imports sells both new and pre-owned (used) cars. Financial data for...

-

What is a P-value for a hypothesis test?

-

You plan a survey to estimate the proportion of students on your campus who carry an iPad regularly. How many students should be in the sample if you want (with 95% confidence) a margin of error of...

-

What is a hypothesis test?

Study smarter with the SolutionInn App