The International Financial Reporting Standard (IFRS)s Conceptual Framework and the Financial Accounting Standards Board (FASB)s Conceptual Framework

Question:

The International Financial Reporting Standard (IFRS)’s Conceptual Framework and the Financial Accounting Standards Board (FASB)’s Conceptual Framework state that future cash flows prediction is one of the key objectives of financial reporting. Atqa, Lee, and Mohd-Saleh (2019) investigated whether the adoption of IFRS (locally known as the Malaysian Financial Reporting Standard (MFRS)) in Malaysia since the year 2006 improves the predictability of future cash flows of Malaysian public listed firms from the institutional perspective. The results show that the cash flows under the IFRS regime significantly predict future operating cash flows (p.851).

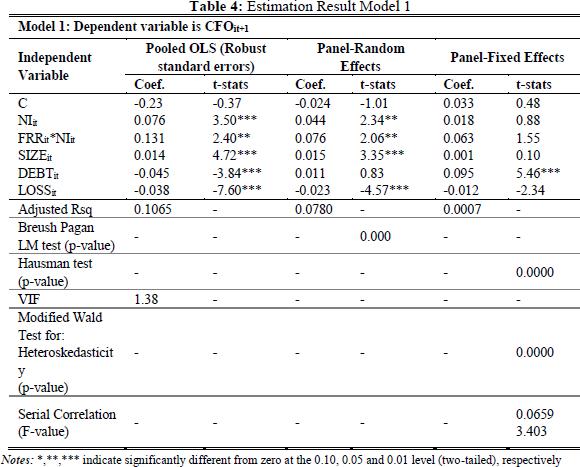

The following Table 4 (p. 863) is extracted from Atqa, Lee, and Mohd-Saleh (2019). Has IFRSs Improves Predictions of Future Cash Flows? Evidence from Malaysia. International Journal of Business and Society, 20(2), 851-869.

Adopted from Atqa, Lee, and Mohd-Saleh (2019) p.863.

- Interpret and justify with relevant citations for the results reported in Table 4 above.

Expert Answer:

The results in Table 4 show that the adoption of IFRS in Malaysia significantly improves the predict... View the full answer

Intermediate accounting

ISBN: 978-0077647094

7th edition

Authors: J. David Spiceland, James Sepe, Mark Nelson