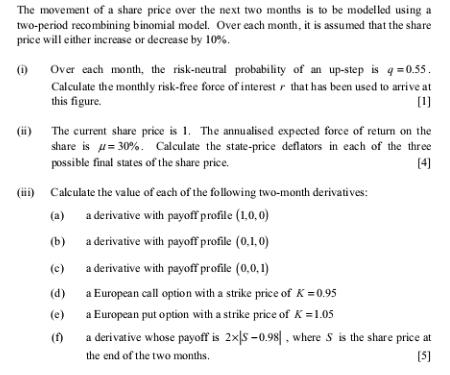

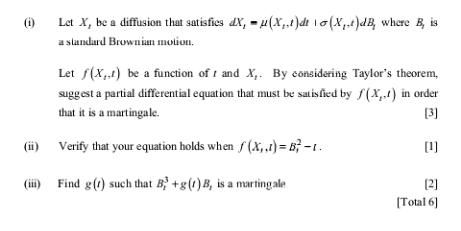

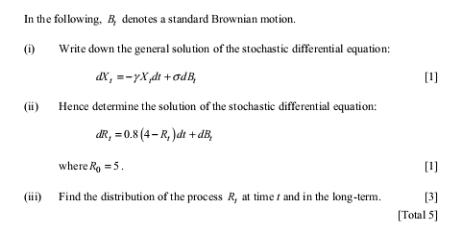

The movement of a share price over the next two months is to be modelled using...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Binomial Model and RiskNeutral Pricing Part 1 I RiskNeutral Probability and Force of Interest In a twoperiod binomial model with an upmovement probabi... View the full answer

Related Book For

Posted Date: