The objective of the Continuing Case is to help you synthesize and integrate the various financial...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

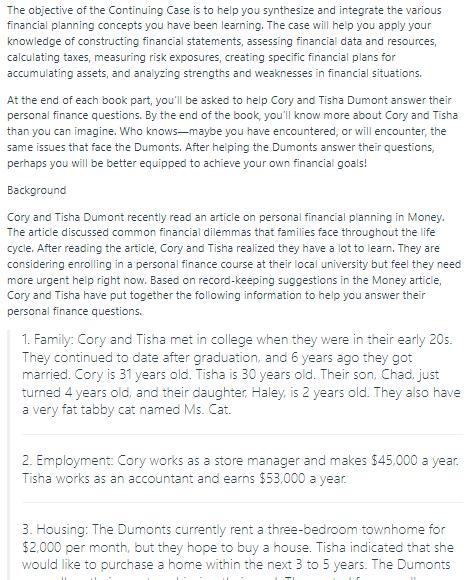

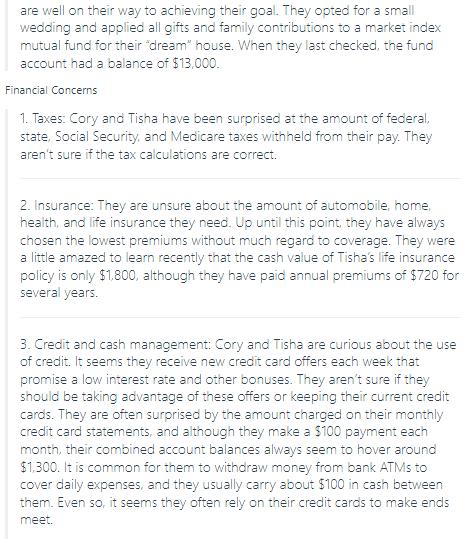

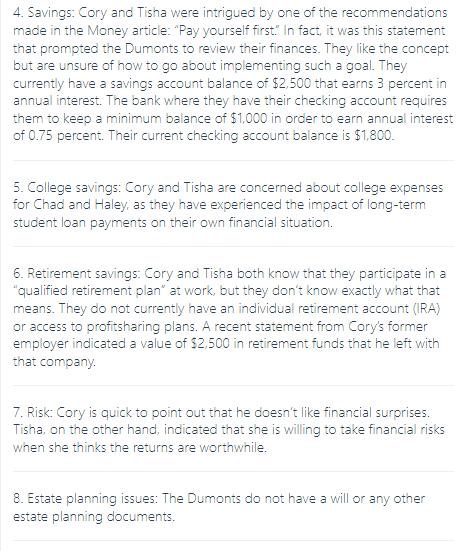

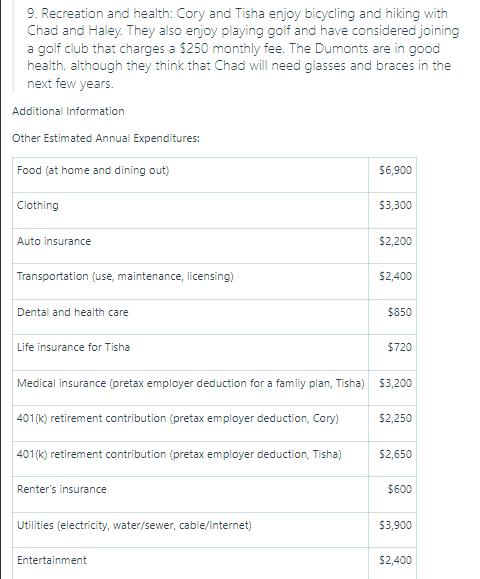

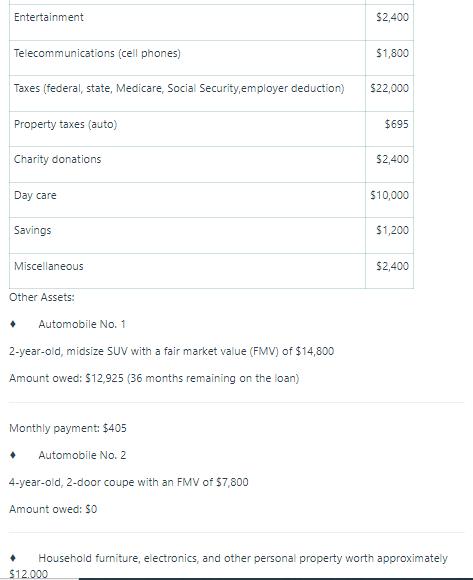

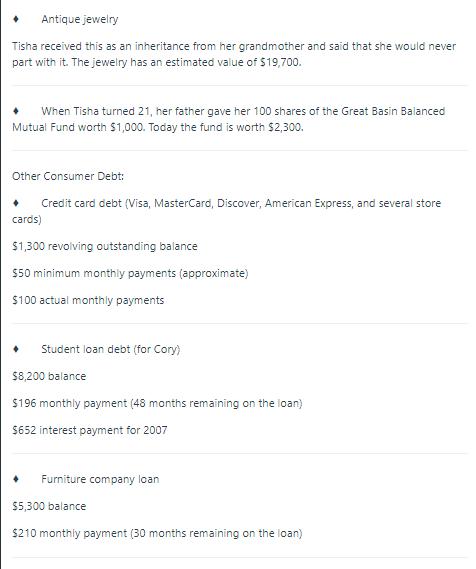

The objective of the Continuing Case is to help you synthesize and integrate the various financial planning concepts you have been learning. The case will help you apply your knowledge of constructing financial statements, assessing financial data and resources, calculating taxes, measuring risk exposures, creating specific financial plans for accumulating assets, and analyzing strengths and weaknesses in financial situations. At the end of each book part, you'll be asked to help Cory and Tisha Dumont answer their personal finance questions. By the end of the book, you'll know more about Cory and Tisha than you can imagine. Who knows-maybe you have encountered, or will encounter, the same issues that face the Dumonts. After helping the Dumonts answer their questions, perhaps you will be better equipped to achieve your own financial goals! Background Cory and Tisha Dumont recently read an article on personal financial planning in Money. The article discussed common financial dilemmas that families face throughout the life cycle. After reading the article, Cory and Tisha realized they have a lot to learn. They are considering enrolling in a personal finance course at their local university but feel they need more urgent help right now. Based on record-keeping suggestions in the Money article, Cory and Tisha have put together the following information to help you answer their personal finance questions. 1. Family: Cory and Tisha met in college when they were in their early 20s. They continued to date after graduation, and 6 years ago they got married. Cory is 31 years old. Tisha is 30 years old. Their son, Chad, just turned 4 years old, and their daughter, Haley, is 2 years old. They also have a very fat tabby cat named Ms. Cat. 2. Employment: Cory works as a store manager and makes $45,000 a year. Tisha works as an accountant and earns $53,000 a year. 3. Housing: The Dumonts currently rent a three-bedroom townhome for $2,000 per month, but they hope to buy a house. Tisha indicated that she would like to purchase a home within the next 3 to 5 years. The Dumonts are well on their way to achieving their goal. They opted for a small wedding and applied all gifts and family contributions to a market index mutual fund for their dream" house. When they last checked, the fund account had a balance of $13,000. Financial Concerns 1. Taxes: Cory and Tisha have been surprised at the amount of federal, state, Social Security, and Medicare taxes withheld from their pay. They aren't sure if the tax calculations are correct. 2. Insurance: They are unsure about the amount of automobile, home, health, and life insurance they need. Up until this point, they have always chosen the lowest premiums without much regard to coverage. They were a little amazed to learn recently that the cash value of Tisha's life insurance policy is only $1,800, although they have paid annual premiums of $720 for several years. 3. Credit and cash management: Cory and Tisha are curious about the use of credit. It seems they receive new credit card offers each week that promise a low interest rate and other bonuses. They aren't sure if they should be taking advantage of these offers or keeping their current credit cards. They are often surprised by the amount charged on their monthly credit card statements, and although they make a $100 payment each month, their combined account balances always seem to hover around $1,300. It is common for them to withdraw money from bank ATMs to cover daily expenses, and they usually carry about $100 in cash between them. Even so, it seems they often rely on their credit cards to make ends meet. 4. Savings: Cory and Tisha were intrigued by one of the recommendations made in the Money article: "Pay yourself first." In fact, it was this statement that prompted the Dumonts to review their finances. They like the concept but are unsure of how to go about implementing such a goal. They currently have a savings account balance of $2,500 that earns 3 percent in annual interest. The bank where they have their checking account requires them to keep a minimum balance of $1,000 in order to earn annual interest of 0.75 percent. Their current checking account balance is $1,800. 5. College savings: Cory and Tisha are concerned about college expenses for Chad and Haley, as they have experienced the impact of long-term student loan payments on their own financial situation. 6. Retirement savings: Cory and Tisha both know that they participate in a "qualified retirement plan" at work, but they don't know exactly what that means. They do not currently have an individual retirement account (IRA) or access to profitsharing plans. A recent statement from Cory's former employer indicated a value of $2,500 in retirement funds that he left with that company. 7. Risk: Cory is quick to point out that he doesn't like financial surprises. Tisha, on the other hand, indicated that she is willing to take financial risks when she thinks the returns are worthwhile. 8. Estate planning issues: The Dumonts do not have a will or any other estate planning documents. 9. Recreation and health: Cory and Tisha enjoy bicycling and hiking with Chad and Haley. They also enjoy playing golf and have considered joining a golf club that charges a $250 monthly fee. The Dumonts are in good health, although they think that Chad will need glasses and braces in the next few years. Additional Information Other Estimated Annual Expenditures: Food (at home and dining out) Clothing Auto insurance Transportation (use, maintenance, licensing) Dental and health care Life insurance for Tisha 401(k) retirement contribution (pretax employer deduction, Tisha) Renter's insurance Utilities (electricity, water/sewer, cable/Internet) $6,900 Entertainment $3,300 $2,200 Medical insurance (pretax employer deduction for a family plan, Tisha) $3,200 401(k) retirement contribution (pretax employer deduction, Cory) $2,400 $850 $720 $2,250 $2,650 $600 $3,900 $2,400 Entertainment Telecommunications (cell phones) Taxes (federal, state, Medicare, Social Security,employer deduction) Property taxes (auto) Charity donations Day care Savings Miscellaneous Other Assets: Automobile No. 1 2-year-old, midsize SUV with a fair market value (FMV) of $14,800 Amount owed: $12,925 (36 months remaining on the loan) ♦ Monthly payment: $405 Automobile No. 2 ♦ 4-year-old, 2-door coupe with an FMV of $7,800 Amount owed: $0 $2,400 $12.000 $1,800 $22,000 $695 $2,400 $10,000 $1,200 $2,400 Household furniture, electronics, and other personal property worth approximately Antique jewelry Tisha received this as an inheritance from her grandmother and said that she would never part with it. The jewelry has an estimated value of $19,700. When Tisha turned 21, her father gave her 100 shares of the Great Basin Balanced Mutual Fund worth $1,000. Today the fund is worth $2,300. Other Consumer Debt: Credit card debt (Visa, MasterCard, Discover, American Express, and several store cards) $1,300 revolving outstanding balance $50 minimum monthly payments (approximate) $100 actual monthly payments. Student loan debt (for Cory) $8,200 balance $196 monthly payment (48 months remaining on the loan) $652 interest payment for 2007 Furniture company loan $5,300 balance $210 monthly payment (30 months remaining on the loan) $5,300 balance $210 monthly payment (30 months remaining on the loan) Part I: Financial Planning Using information from the income and expense statements and the balance sheet, calculate the following ratios: a. Current ratio b. Month's living expenses covered ratio c. Debt ratio d. Long-term debt coverage ratio e. Savings ratio The objective of the Continuing Case is to help you synthesize and integrate the various financial planning concepts you have been learning. The case will help you apply your knowledge of constructing financial statements, assessing financial data and resources, calculating taxes, measuring risk exposures, creating specific financial plans for accumulating assets, and analyzing strengths and weaknesses in financial situations. At the end of each book part, you'll be asked to help Cory and Tisha Dumont answer their personal finance questions. By the end of the book, you'll know more about Cory and Tisha than you can imagine. Who knows-maybe you have encountered, or will encounter, the same issues that face the Dumonts. After helping the Dumonts answer their questions, perhaps you will be better equipped to achieve your own financial goals! Background Cory and Tisha Dumont recently read an article on personal financial planning in Money. The article discussed common financial dilemmas that families face throughout the life cycle. After reading the article, Cory and Tisha realized they have a lot to learn. They are considering enrolling in a personal finance course at their local university but feel they need more urgent help right now. Based on record-keeping suggestions in the Money article, Cory and Tisha have put together the following information to help you answer their personal finance questions. 1. Family: Cory and Tisha met in college when they were in their early 20s. They continued to date after graduation, and 6 years ago they got married. Cory is 31 years old. Tisha is 30 years old. Their son, Chad, just turned 4 years old, and their daughter, Haley, is 2 years old. They also have a very fat tabby cat named Ms. Cat. 2. Employment: Cory works as a store manager and makes $45,000 a year. Tisha works as an accountant and earns $53,000 a year. 3. Housing: The Dumonts currently rent a three-bedroom townhome for $2,000 per month, but they hope to buy a house. Tisha indicated that she would like to purchase a home within the next 3 to 5 years. The Dumonts are well on their way to achieving their goal. They opted for a small wedding and applied all gifts and family contributions to a market index mutual fund for their dream" house. When they last checked, the fund account had a balance of $13,000. Financial Concerns 1. Taxes: Cory and Tisha have been surprised at the amount of federal, state, Social Security, and Medicare taxes withheld from their pay. They aren't sure if the tax calculations are correct. 2. Insurance: They are unsure about the amount of automobile, home, health, and life insurance they need. Up until this point, they have always chosen the lowest premiums without much regard to coverage. They were a little amazed to learn recently that the cash value of Tisha's life insurance policy is only $1,800, although they have paid annual premiums of $720 for several years. 3. Credit and cash management: Cory and Tisha are curious about the use of credit. It seems they receive new credit card offers each week that promise a low interest rate and other bonuses. They aren't sure if they should be taking advantage of these offers or keeping their current credit cards. They are often surprised by the amount charged on their monthly credit card statements, and although they make a $100 payment each month, their combined account balances always seem to hover around $1,300. It is common for them to withdraw money from bank ATMs to cover daily expenses, and they usually carry about $100 in cash between them. Even so, it seems they often rely on their credit cards to make ends meet. 4. Savings: Cory and Tisha were intrigued by one of the recommendations made in the Money article: "Pay yourself first." In fact, it was this statement that prompted the Dumonts to review their finances. They like the concept but are unsure of how to go about implementing such a goal. They currently have a savings account balance of $2,500 that earns 3 percent in annual interest. The bank where they have their checking account requires them to keep a minimum balance of $1,000 in order to earn annual interest of 0.75 percent. Their current checking account balance is $1,800. 5. College savings: Cory and Tisha are concerned about college expenses for Chad and Haley, as they have experienced the impact of long-term student loan payments on their own financial situation. 6. Retirement savings: Cory and Tisha both know that they participate in a "qualified retirement plan" at work, but they don't know exactly what that means. They do not currently have an individual retirement account (IRA) or access to profitsharing plans. A recent statement from Cory's former employer indicated a value of $2,500 in retirement funds that he left with that company. 7. Risk: Cory is quick to point out that he doesn't like financial surprises. Tisha, on the other hand, indicated that she is willing to take financial risks when she thinks the returns are worthwhile. 8. Estate planning issues: The Dumonts do not have a will or any other estate planning documents. 9. Recreation and health: Cory and Tisha enjoy bicycling and hiking with Chad and Haley. They also enjoy playing golf and have considered joining a golf club that charges a $250 monthly fee. The Dumonts are in good health, although they think that Chad will need glasses and braces in the next few years. Additional Information Other Estimated Annual Expenditures: Food (at home and dining out) Clothing Auto insurance Transportation (use, maintenance, licensing) Dental and health care Life insurance for Tisha 401(k) retirement contribution (pretax employer deduction, Tisha) Renter's insurance Utilities (electricity, water/sewer, cable/Internet) $6,900 Entertainment $3,300 $2,200 Medical insurance (pretax employer deduction for a family plan, Tisha) $3,200 401(k) retirement contribution (pretax employer deduction, Cory) $2,400 $850 $720 $2,250 $2,650 $600 $3,900 $2,400 Entertainment Telecommunications (cell phones) Taxes (federal, state, Medicare, Social Security,employer deduction) Property taxes (auto) Charity donations Day care Savings Miscellaneous Other Assets: Automobile No. 1 2-year-old, midsize SUV with a fair market value (FMV) of $14,800 Amount owed: $12,925 (36 months remaining on the loan) ♦ Monthly payment: $405 Automobile No. 2 ♦ 4-year-old, 2-door coupe with an FMV of $7,800 Amount owed: $0 $2,400 $12.000 $1,800 $22,000 $695 $2,400 $10,000 $1,200 $2,400 Household furniture, electronics, and other personal property worth approximately Antique jewelry Tisha received this as an inheritance from her grandmother and said that she would never part with it. The jewelry has an estimated value of $19,700. When Tisha turned 21, her father gave her 100 shares of the Great Basin Balanced Mutual Fund worth $1,000. Today the fund is worth $2,300. Other Consumer Debt: Credit card debt (Visa, MasterCard, Discover, American Express, and several store cards) $1,300 revolving outstanding balance $50 minimum monthly payments (approximate) $100 actual monthly payments. Student loan debt (for Cory) $8,200 balance $196 monthly payment (48 months remaining on the loan) $652 interest payment for 2007 Furniture company loan $5,300 balance $210 monthly payment (30 months remaining on the loan) $5,300 balance $210 monthly payment (30 months remaining on the loan) Part I: Financial Planning Using information from the income and expense statements and the balance sheet, calculate the following ratios: a. Current ratio b. Month's living expenses covered ratio c. Debt ratio d. Long-term debt coverage ratio e. Savings ratio

Expert Answer:

Answer rating: 100% (QA)

To calculate the requested ratios for Cory and Tisha Dumont well use the provided income and expense statements and balance sheet Lets compute each ra... View the full answer

Related Book For

Posted Date:

Students also viewed these finance questions

-

The goal of this final case is to help you practice creating and understanding the accounting cycle, income statement, and balance sheet, along with providing practice on current liabilities (the one...

-

The goal of this mini-project is to help you verify the Rule for Sample Proportions firsthand, using a physical simulation. You will use the population represented in Figure 19.1 to do so. It...

-

The purpose of this mini-project is to help you verify the Rule for Sample Means, using a physical simulation. Suppose you are interested in measuring the average amount of blood contained in the...

-

If the appropriate discount rate for the following cash flows is 7.13 percent per year, what is the present value of the cash flows? Year Cash Flow 1 ......................$1,400 2...

-

You are a senior member of the financial reporting team reporting to the Commissioner of Finance of the Town of Greenville. The following is a list of units and their relationship with the town...

-

Waterman's 14% coupon rate, semiannual payment, $1,000 par value bonds that mature in 22 years are callable 4 years from now at a price of $1,090. The bonds sell at a price of $1,410 and the yield...

-

For the similarity solution, what are the boundary conditions for the constant-wall-flux case? Show that a complete similarity does not exist for this case. Also show the condition for the case where...

-

Use the information presented in BE5-14 for Martinez Corporation to compute the net cash used (provided) by financing activities.

-

Merchants remit $800,000 to a county government in calendar year 2022 for sales taxes collected in 2022. In January, 2023, they send the county an additional $25,000 applicable to the year 2022....

-

An army division in Iraq has five troop encampments in the desert, and the division leaders want to determine the best location for a supply depot to serve the camps. The (x, y) coordinates (in...

-

State by using the words: increase, decrease and/or no-change, the effect that each scenario will have on a company's WACC? (No computation required) (3 marks) Increase in tax rate Increase in weight...

-

In Florida, and was reported in the Wall Street Journal in 2002. First, get out a piece of paper and draw a circle in the middle of it about the size of an apple, draw a second circle just slightly...

-

Lockheed Martin's accounts receivable in the 2023 financial statement include billed and unbilled costs and accrued profit primarily related to sales and long-term contracts recognized in financial...

-

A stripped bond Question 9Select one: a. is a bearer bond and pays coupons at regular intervals until maturity. a. is a bearer bond and pays coupons at regular intervals until maturity. b. is a...

-

is to crystallize the asset positions into GBP to retain parity.

-

At a recent stockholder meeting for Ignate Inc., a group of stockholders expressed disagreement with the way that the managers were using free cash flow. Because they wanted to be able to control how...

-

How much is 51% of Team System's common equity worth? Use both a discounted cash flow and a multiple-based valuation, for multiple method, use at least Sales/EV(enterprise value) ?and EBIT/EV...

-

Given that all the choices are true, which one concludes the paragraph with a precise and detailed description that relates to the main topic of the essay? A. NO CHANGE B. Decades, X-ray C. Decades...

-

Refer to each of these news stories printed or summarized in the Appendix, and consult the original source article on the companion website if necessary. In each case, explain whether or not a...

-

The Roper Organization (1992) conducted a study as part of a larger survey to ascertain the number of American adults who had experienced phenomena such as seeing a ghost, feeling as if you left your...

-

An airline serves lunch in the first- class cabin. Customers are given a choice of either a sandwich or chicken salad. There are 12 customers in first-class, and the airline loads seven of each meal...

-

In testing a claim about a population mean, a larger z test statistic always results in a larger P-value. Decide whether the statement makes sense (or is clearly true) or does not make sense (or is...

-

In testing the claim that the mean IQ score of statistics students is greater than 100, the alternative hypothesis is expressed as > 100. Decide whether the statement makes sense (or is clearly...

-

A handy mnemonic for interpreting the P-value in a hypothesis test is this: If the P (value) is low, then the null must go.

Study smarter with the SolutionInn App