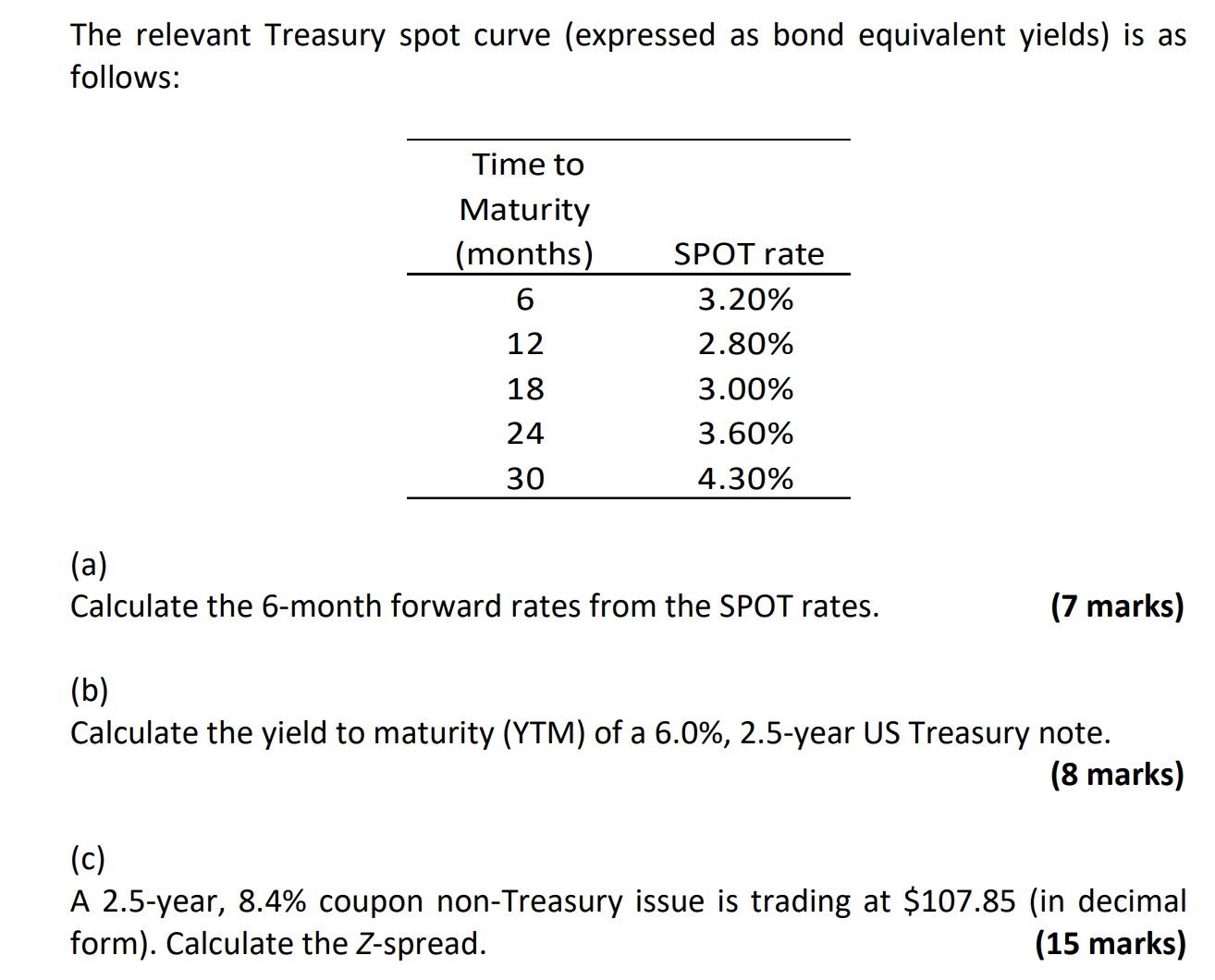

The relevant Treasury spot curve (expressed as bond equivalent yields) is as follows: Time to Maturity...

Fantastic news! We've Found the answer you've been seeking!

Question:

![Risk Premium E[R] (note R = r-r) Hints: 0.0026 0.0026 The alpha and beta come directly from the regression](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2023/04/6448bc52df573_1682488399936.jpg)

Transcribed Image Text:

The relevant Treasury spot curve (expressed as bond equivalent yields) is as follows: Time to Maturity (months) 6 12 18 24 30 SPOT rate 3.20% 2.80% 3.00% 3.60% 4.30% (a) Calculate the 6-month forward rates from the SPOT rates. (7 marks) (b) Calculate the yield to maturity (YTM) of a 6.0%, 2.5-year US Treasury note. (8 marks) (c) A 2.5-year, 8.4% coupon non-Treasury issue is trading at $107.85 (in decimal form). Calculate the Z-spread. (15 marks) Risk Premium E[R] (note R = r-r₁) Hints: ● ● 0.0026 0.0026 The alpha and beta come directly from the regression coefficient estimates. The weekly variance of returns can be calculated as the Total Sum of Squares (SS) divided by the total degrees of freedom (df). The residual standard deviation can be calculated from the Standard Error of the regression (in the regression statistics box). Calculate the variance of the residuals as the square of residual standard deviation. Finally, calculate the risk premium using the expected return equation: E[R] =B₁x(Market Risk Premium). b) Step 2: Calculate the covariance matrix of the excess returns. Complete the matrix below. Remember, the index model makes a simplifying assumption about the covariances, so we can use the formula: COV(ri, rj) = BiBjƠM² S&P500 AIG CITI S&P500 AIG CITI c) Now we have all the information we need to calculate the initial position in each security. Note: We will ignore systematic risk at first, to make things easier, and we'll account for it later in the process. Compute the initial position in each security, and scale them so that these weights sum to one. What are the weights? (Hint: Steps 1 and 2) d) Using the weights you calculated in step (c), calculate the weighted average alpha, the weighted average beta, and the weighted average residual variance. (Hints: Steps 3, 4, and 6) e) Now that you know the weights for the individual assets, calculate how much money you should put in the active portfolio. [Hint: see step 5 from Bodie, Kane, and Marcus, page 266] ● You are required to demonstrate trading strategies and instruments that would be appropriate to exploit price efficiency/inefficiency during the process of acquisition. Your analysis should forecast possible trading profit going forward until the appropriate cut-off date. (40%) 1) Drawing on the insights from previous section, describe the type of trading strategies and risk management tools intended for the event and your design principle for using these tools based on the result of event analysis 2) Demonstrate, using relevant trading instruments for the type of strategy used, e.g. long- short strategy and calculate total return from such strategy. 3) Calculate relevant statistics to demonstrate understanding on volatility and correlation amongst the trading pairs. 4) Illustrate how to avoid adverse price movement as a result of (a) unexpected down side movement for the long position; (b) unexpected up side movement for the short position; and the characteristics of the type of instrument used to hedge risks. 5) In retrospect, how to use (3) in combination with (2) to maximise profit The relevant Treasury spot curve (expressed as bond equivalent yields) is as follows: Time to Maturity (months) 6 12 18 24 30 SPOT rate 3.20% 2.80% 3.00% 3.60% 4.30% (a) Calculate the 6-month forward rates from the SPOT rates. (7 marks) (b) Calculate the yield to maturity (YTM) of a 6.0%, 2.5-year US Treasury note. (8 marks) (c) A 2.5-year, 8.4% coupon non-Treasury issue is trading at $107.85 (in decimal form). Calculate the Z-spread. (15 marks) Risk Premium E[R] (note R = r-r₁) Hints: ● ● 0.0026 0.0026 The alpha and beta come directly from the regression coefficient estimates. The weekly variance of returns can be calculated as the Total Sum of Squares (SS) divided by the total degrees of freedom (df). The residual standard deviation can be calculated from the Standard Error of the regression (in the regression statistics box). Calculate the variance of the residuals as the square of residual standard deviation. Finally, calculate the risk premium using the expected return equation: E[R] =B₁x(Market Risk Premium). b) Step 2: Calculate the covariance matrix of the excess returns. Complete the matrix below. Remember, the index model makes a simplifying assumption about the covariances, so we can use the formula: COV(ri, rj) = BiBjƠM² S&P500 AIG CITI S&P500 AIG CITI c) Now we have all the information we need to calculate the initial position in each security. Note: We will ignore systematic risk at first, to make things easier, and we'll account for it later in the process. Compute the initial position in each security, and scale them so that these weights sum to one. What are the weights? (Hint: Steps 1 and 2) d) Using the weights you calculated in step (c), calculate the weighted average alpha, the weighted average beta, and the weighted average residual variance. (Hints: Steps 3, 4, and 6) e) Now that you know the weights for the individual assets, calculate how much money you should put in the active portfolio. [Hint: see step 5 from Bodie, Kane, and Marcus, page 266] ● You are required to demonstrate trading strategies and instruments that would be appropriate to exploit price efficiency/inefficiency during the process of acquisition. Your analysis should forecast possible trading profit going forward until the appropriate cut-off date. (40%) 1) Drawing on the insights from previous section, describe the type of trading strategies and risk management tools intended for the event and your design principle for using these tools based on the result of event analysis 2) Demonstrate, using relevant trading instruments for the type of strategy used, e.g. long- short strategy and calculate total return from such strategy. 3) Calculate relevant statistics to demonstrate understanding on volatility and correlation amongst the trading pairs. 4) Illustrate how to avoid adverse price movement as a result of (a) unexpected down side movement for the long position; (b) unexpected up side movement for the short position; and the characteristics of the type of instrument used to hedge risks. 5) In retrospect, how to use (3) in combination with (2) to maximise profit

Expert Answer:

Answer rating: 100% (QA)

a To calculate the 6month forward rates from the spot rates we can use the following formula Forward ... View the full answer

Related Book For

Posted Date:

Students also viewed these finance questions

-

The following additional information is available for the Dr. Ivan and Irene Incisor family from Chapters 1-5. Ivan's grandfather died and left a portfolio of municipal bonds. In 2012, they pay Ivan...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

KYC's stock price can go up by 15 percent every year, or down by 10 percent. Both outcomes are equally likely. The risk free rate is 5 percent, and the current stock price of KYC is 100. (a) Price a...

-

A ping pong ball is drawn at random from an urn consisting of balls numbered 4 through 9. A player wins $1.5 if the number on the ball is odd and loses $1.5 if the number is even. Let x be the amount...

-

The eddy viscosity expression in the viscous sublayer, verify that Eq. 5.4-2 for the eddy viscosity comes directly from the Taylor series expression in Eq. 5.3-13.

-

Given \(\theta=\) angle through which the axis of the outer forward wheel turns \(\phi=\) angle through which the axis of the inner forward wheel turns \(a=\) distance between the pivots of front...

-

At the beginning of 2016, John Cornell decided to quit his job as a construction company ey supervisor and formed his own residential housing construction company. When he resigned, he had a contract...

-

The adjusted trial balance for Karr Farm Corporation at the end of the current year contained the following accounts. Interest Payable $ 9000 Lease Liability 89,500 Bonds Payable, due 2019 180,000...

-

Question 12 of 50 A customer has the following position: Short ABCD Jul 25 put @ 3. What do you know is true about the position? A It is bullish B It is bearish C It is in-the-money D It is...

-

An exercise advocate wants to determine the effect that walking rigorously has on weight loss. The researcher recruits participants to engage in a weeklong study. The researcher instructs...

-

Five individuals have provided their name and the day of the year they were born in a partially completed table directly below. Given (known) info Please use the lookup functions to identify the...

-

Use the Shapiro Library and web resources to conduct research on the process of repatriation. Write a short paper explaining your findings. In your paper, describe the specific roles that HR,...

-

Solve for x 2sin(x) -3 = 0 , for 0 x 2 Feel free to use these questions for practice or in your assignments. Good luck!

-

Four identical charged particles (g = +10.9 C) are located on the corners of a rectangle as shown in the figure below. The dimensions of the rectangle are L = 57.0 cm and W = 13.5 cm. 1.E W (a)...

-

Determine the elongation (in meters) of the whole rod in the figure below if it is under a tension of 4.5x10 N. The radius is 0.22 cm, while the lengths are Lal = 1.5 m and Lco = 2.8 m. Copper Lco...

-

We have the following loading with F = 77 N, FB = 194 N, and Fc = 191 N. FB Fc Efx=0 - FA+ FB + Fc + Fo=0 What is the internal force Fcp between C and D in units of Newtons? FA +x

-

Discuss the issues of jurisdiction (geographic, subject matter, etc.) that were brought up in the story. Is it fair that some people face charges for crimes on Indian reservations, while others do...

-

Suppose that A is an m n matrix with linearly independent columns and the linear system LS(A, b) is consistent. Show that this system has a unique solution.

-

The New York Times reported on January 18, 2012, in an article titled What the Top 1% of Earners Majored In that 8.2% of Americans who majored in economics for their undergraduate degree are in the...

-

What does GDP per capita measure? Why is it not a precise measure of a typical persons standard of living in a country?

-

Why have pensions become a less common form of retirement benefit offered by companies?

-

The following data (and annotations) are related to the June 2019 charges appearing in the work-in-process account for Sutter Company's first processing department: Sutter uses the FIFO method....

-

Terrace Corporation makes an industrial cleaner in two sequential departments, Compounding and Drying. All materials are added at the beginning of the process in the Compounding Department....

-

The following are selected operating data for Jackson Company's Blending Department for November 2019. Painting and packaging operations are carried out subsequently in other departments. Calculate...

Study smarter with the SolutionInn App