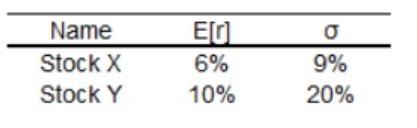

The returns on stocks X and Y have the following properties: where is the standard deviation

Question:

where σ is the standard deviation of the return. The correlation between X and Y returns is 0.2. The risk free rate is 2%.

a. What is the Sharpe ratio of stock X?

b.What is the Sharpe ratio of stock Y?

c.Imagine that a rational investor must construct a portfolio consisting of only one of these stocks and the risk free bond. In which stock should he invest?

A.Stock X

B.Stock Y

d.Now imagine the investor is able to invest in both stocks and builds a portfolio by investing 75% of her wealth in stock X, and 25% in stock

Y. Compute the expected return of this portfolio & the and standard deviation of the portfolio.

e. The investor can borrow and lend at the risk-free rate. She thus chooses to mix the portfolio found in the Question above, (i.e., keeping the allocation among risky assets equal to 75% in stock X and 25% in stock Y) with the risk-free asset. What is the highest return she can attain while keeping her portfolio standard deviation below 12%? (You can borrow at the risk-free rate if needed)

Expert Answer:

a The Sharpe ratio of stock X is calculated as ErX rf X where ErX is the expected return of stock X rf is the riskfree rate and X is the standard devi... View the full answer