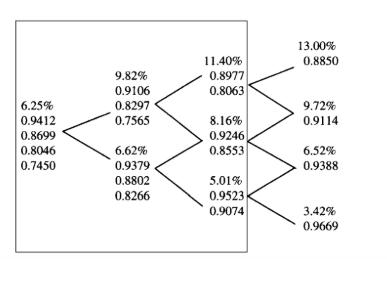

The three-period binomial interest rate tree provided below gives one-period interest rates and prices of zero-coupon bonds.

Question:

The three-period binomial interest rate tree provided below gives one-period interest rates and prices of zero-coupon bonds. Starting at t = 0, you are provided with the one-period interest rate and prices of zero-coupon bonds with maturities of one period, two periods, three periods, and four periods. At t=1, you are provided with the one-period interest rate and prices of zero-coupon bonds with maturities of one period, two periods, and three periods. At t=2, you are provided with the one-period interest rate and prices of zero-coupon bonds with maturities of one period and two periods. At t=3, you are provided with the one-period interest rate and prices of zero-coupon bonds with maturity of one period.

Calculate the price of a two-period floor (depicted below by a rectangle) with an exercise rate of 9 percent. The underlying is the one-period rate.

Expert Answer:

The price of a twoperiod floor with an exercise rate of 9 is the amount of money that the holder of ... View the full answer